- Turkish imports witness uptick, India records sharp decline

- Marginal drop in steel production, high Chinese exports weigh on market

- Scrap quality issues, protectionist trade policies remain pressing concerns

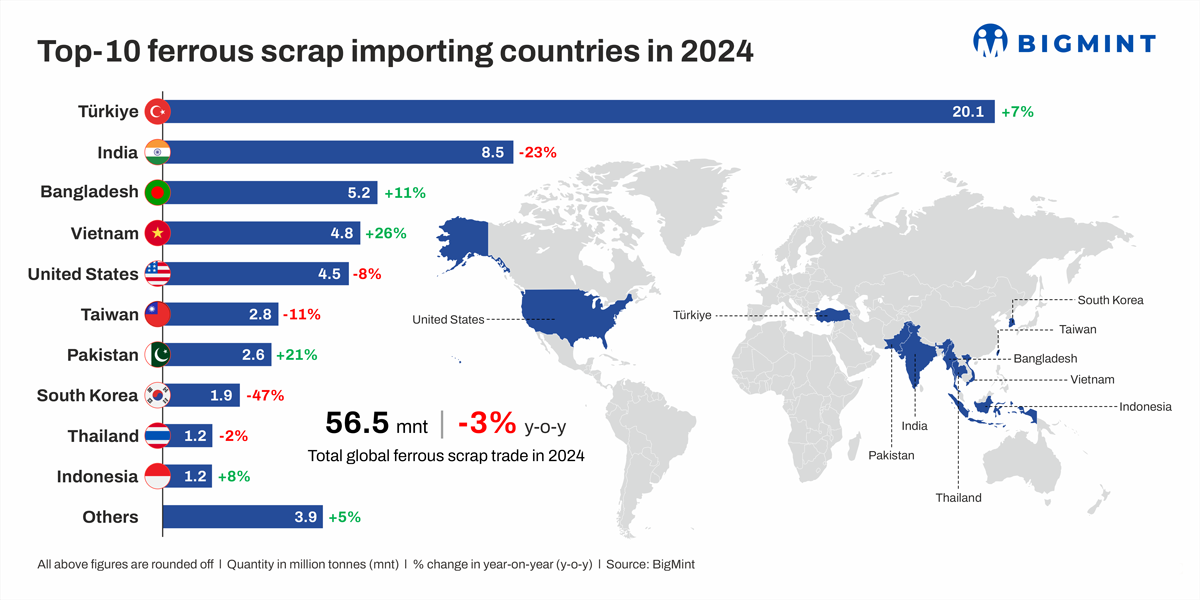

Morning Brief: Global seaborne ferrous scrap trade volumes dropped 3% y-o-y to 56.5 millon tonnes (mnt) in CY’24 compared to 58.08 mnt in the preceding year, as per BigMint data.

This was largely in consonance with the marginal de-growth in global crude steel production, which fell by 0.48% y-o-y to 1,882 mnt in the year gone by from 1,891 mnt in CY’23, as per World Steel Association data.

Amid subdued steel demand in key geographies, scrap imports by major countries edged down in CY’24, while a glut of Chinese steel in the global market impacted scrap demand dynamics. Coupled with this, a rapid surge in freight rates triggered by geopolitical disruptions also impacted the seaborne scrap market.

Top scrap-importing countries

Turkiye, the largest importer of ferrous scrap, saw imports rising by 6.6% y-o-y to 20.07 mnt in CY’24 from 18.82 mnt in CY’23. This was due to a 10% growth in crude steel production, which reached 37 mnt in CY’24.

The United Kingdom recorded the highest growth of 73% in exports to Turkiye, the United States remained the largest supplier, with a slight 0.8% rise in shipments.

Despite strong growth in steel production, scrap imports by Turkiye were impacted by high Chinese steel exports and a lacklustre rebar export market.

India’s scrap imports dropped nearly 25% y-o-y in CY’24 to 8.44 mnt compared with over 11 mnt in CY’23. Apart from higher usage of domestic scrap, geopolitical conflicts and their impact on maritime trade and freight rates, declining shipments from key geographies, and higher use of sponge iron in domestic steelmaking were some of the major factors weighing on scrap imports.

Bangladesh’s scrap imports rose by 11% y-o-y to 5.18 mnt, primarily driven by bulk purchases by the major buyers who managed to secure LCs despite weak domestic steel demand. Short-sea shipments from Australia and Japan played a key role in supporting the overall increase. However, the slowdown in the domestic steel industry and aborted expansions, following domestic political disturbances, coupled with a sluggish economy, kept overall steel demand unstable, limiting further import growth.

The US imported 4.49 mnt of ferrous scrap in CY’24, down 8.2% from 4.89 mnt in CY’23 due mainly to a 15% drop in shipments from Canada to 3.18 mnt. US scrap exports slipped 7.9% y-o-y to 14.51 mnt, down from 15.75 mnt in 2023, marking the lowest export volume since 2020.

The decline in exports and steady import volumes reflect stronger domestic demand. According to the US Geological Survey (USGS), domestic ferrous scrap consumption rose by 1.6% y-o-y to 63 mnt, while direct reduced iron (DRI) usage surged 7.1% to 7.5 mnt.

Pakistan’s scrap imports increased 21% y-o-y to 2.62 mnt on higher shipments by the UK and the US due to competitive pricing and stable supplies. The UAE remained a key supplier, benefiting from shorter shipping times and prompt deliveries. However, political and economic uncertainty in Pakistan has slowed down industrial expansion.

Vietnam’s scrap imports rose by 26% y-o-y to 4.77 mnt in CY’24 on the back of a nearly 17% growth in crude steel production. Despite weak steel demand, Vietnamese mills maintained stable production levels to support ongoing infrastructure projects. The rise was also driven by competitive scrap pricing, making imports more viable compared to alternative raw materials.

In contrast, South Korea’s imports plunged 47.4% y-o-y to 1.86 mnt as sluggish construction activity and steel production cut limited scrap purchases.

Global scrap outlook

The transition to electric arc furnace (EAF) steelmaking is accelerating, driven by the need to cut emissions, yet challenges persist–scrap availability remains tight, and quality issues continue to impact production efficiency. While high-quality scrap is essential for greener steelmaking, its global supply remains constrained, making the shift away from traditional blast furnaces more complex than anticipated.

Demand outlook: no sign of recovery

Steel demand remains weak across major economies. China’s struggling construction sector, historically the backbone of its steel demand, shows no signs of recovery. Chinese EAFs are running at low capacity, keeping scrap demand subdued.

Globally, economic growth remains sluggish outside of India, with high interest rates and inflation suppressing consumer spending in developed markets.

In Turkiye, expectations of a construction sector revival remain low, particularly as post-earthquake reconstruction efforts have been slower than anticipated.

Moreover, the threat of high Chinese steel exports still lingers. US tariffs are unlikely to have a lasting impact on scrap prices or trade flows. Turkish mills, for instance, are expected to continue offsetting high scrap costs by increasing semi-finished steel imports rather than paying premiums for expensive scrap.

Price stability amid supply shifts

Turkish imported bulk HMS scrap prices are projected to hold steady in the $350-370/t CFR Turkiye range till the end of Q1 2025. While US tariffs may initially push up domestic scrap prices, buyers will resist excessive hikes. The UK, EU, and the US remain key suppliers, but regional shifts in supply and demand could reshape trade flows, not to forget protectionist trade policies regarding scrap.

The EU, facing industrial decline, may see lower scrap generation, reducing export volumes.

India’s approach to scrap imports remains opportunistic, largely driven by price competitiveness. However, anticipated safeguards against low-cost Chinese steel could alter the dynamics of scrap trade. Meanwhile, US scrap exporters, particularly on the West Coast, will continue targeting Indian buyers, as inland transportation costs remain prohibitively high for domestic distribution.

Leave a Reply