- Softer China, India demand slows cargo nominations

- South Africa stands firm as other suppliers decline

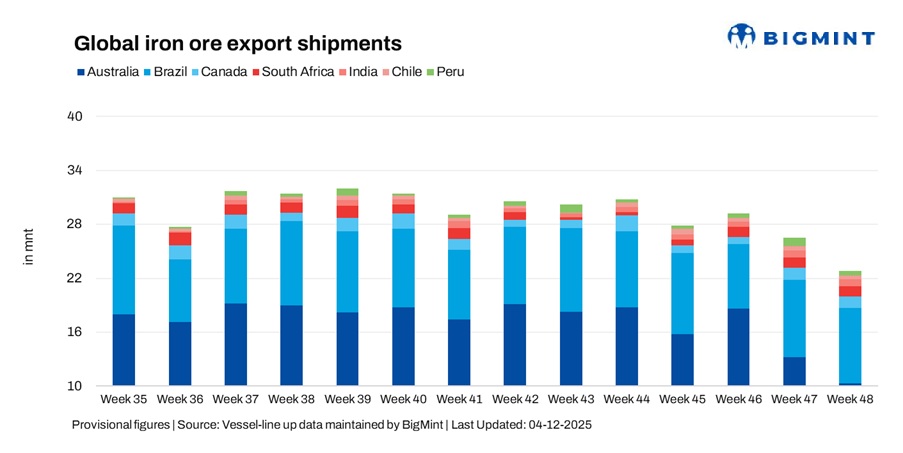

Global seaborne iron ore exports fell 14.2% w-o-w to 22.69 million tonnes (mnt) in the week ended 28 Nov’25) from 26.45 mnt in the previous week, based on BigMint’s vessel line-up data. The pullback was led by a steep drop in shipments from Australia and Peru, while declines in Brazil, Canada, India and Chile further dampened trade momentum. South Africa acted as the only major support to volumes, reporting a modest rise amid firm demand from Northeast Asian buyers.

The slowdown in shipments reflected softer procurement from Chinese and Indian mills, who moderated short-term spot buying despite healthy forward demand. While freight sentiment strengthened across major Capesize and Supramax routes, higher bunker costs and selective fixture appetite kept vessel operators cautious, preventing sharper export acceleration. Despite improving chartering confidence, the rise in freight economics offered limited support to cargo flow and could not offset muted spot enquiries across the Pacific.

Country-wise trends

Australia witnesses steep downturn as spot demand eases

Australia’s iron ore exports dropped 21.9% w-o-w to 10.29 mnt in week 48 from 13.18 mnt in week 47, the steepest decline among major suppliers. Port Hedland (5.17 mnt), Walcott (2.79 mnt) and Dampier (2.05 mnt) led shipments, but reduced cargo nominations to China weighed on volumes despite smooth port operations. China imported 8.73 mnt, followed by Japan at 0.92 mnt, as mills slowed spot enquiries after front-loading deliveries earlier in the month. Rio Tinto (4.84 mnt), BHP (3.28 mnt) and FMG (1.46 mnt) led supply, though rising bunker costs and firm Pacific freight limited vessel positioning and fixtures to India and Northeast Asia, further dragging weekly volumes.

Meanwhile, the first commercial iron ore shipment from Guinea’s $23-billion Simandou mine has set sail for China, signalling a major shift in future supply. The development has already lifted Capesize demand and pushed earnings to two-year highs, as China prepares to absorb more high-grade ore beyond traditional shipments from Australia and Brazil.

Brazil moderates amid softer long-haul enquiries

Brazil’s iron ore exports dipped 2.7% w-o-w to 8.36 mnt in week 48, reflecting a quieter week for long-haul fixtures to China. Shipments were led by Ponta da Madeira (2.72 mnt), Tubarão (2.05 mnt), and Itaguaí (1.31 mnt), indicating steady port operations despite the slowdown in fresh stems. China imported 4.30 mnt, with winter restocking continuing at a measured pace but without translating into incremental weekly volumes. Export activity remained supported by major shippers Vale (4.01 mnt) and CSN (3.36 mnt), although cautious procurement trends and costlier freight for the Brazil-China route affected the scheduling of spot shipments.

While supply availability and operational fundamentals stayed stable, the firmer freight environment and conservative buying from key steel mills capped shipment momentum and prevented a week-on-week rebound. Meanwhile, Mubadala and Trafigura are selling their major iron ore and port assets in Brazil, signaling a strategic shift in global commodities. The move reflects reduced focus on traditional mining and growing investment toward renewable energy and green fuels.

Canada edges lower after prior week’s surge

Canada’s iron ore exports recorded a 3.6% w-o-w decline to 1.31 mnt in week 48, easing slightly after the previous week’s uplift. Shipments were led by Sept-Îles (0.74 mnt) and Port-Cartier (0.57 mnt), reflecting steady operational performance. However, spot fixing slowed as key importers held back short-haul purchases in anticipation of stable supply, resulting in softer weekly shipment momentum despite sufficient cargo availability.

Export activity continued to be driven primarily by AMNS (0.57 mnt) and IOC (0.56 mnt), but incremental stems failed to materialise amid conservative procurement behaviour. Although improving freight sentiment in the Pacific supported baseline demand, it was not strong enough to trigger a meaningful rise in fixtures, keeping Canada’s volumes stable but slightly lower compared with the previous week.

South Africa holds firm with incremental gains

South Africa emerged as the only major iron ore exporter to report growth in week 48, with shipments up 2.7% w-o-w to 1.13 mnt. All loadings were handled through Saldanha Bay, where improved port coordination supported a steady flow of vessels. Buying interest remained firm, led by South Korea (0.35 mnt) and The Netherlands (0.20 mnt), helping maintain export momentum even as other markets turned cautious.

Stable demand from Northeast Asian buyers, coupled with better logistics and timely vessel availability, ensured uninterrupted scheduling. Firmer freight fundamentals provided additional support by encouraging sellers to sustain shipments rather than hold cargoes back, allowing South Africa to record volume growth at a time when most major exporters experienced w-o-w declines.

India sees mild correction but overall demand stays healthy

India’s outbound iron ore shipments eased 3.4% w-o-w to 0.75 mnt in week 48, moderating after a strong performance in week 47. Exports were led by Dhamra (0.23 mnt) and Paradip (0.17 mnt), although limited fresh stems from eastern ports and softer procurement from Southeast Asian buyers weighed on weekly totals. China emerged as the largest importer with 0.12 mnt, reflecting steady but measured buying interest.

Despite reduced spot enquiries, export flow remained supported by favourable pricing signals and ongoing winter restocking interest from key markets, which helped maintain baseline volumes. However, the lack of incremental demand and subdued forward bookings restricted shipments from gaining further traction, keeping India’s weekly exports slightly below the previous week.

Chile and Peru shipments slide sharply

Exports from Chile fell 21.7% w-o-w to 0.39 mnt due to reduced availability of spot stems and quieter demand from key East Asian buyers. Huasco and Totoralillo shipped 0.18 mnt each, while tightening vessel availability and higher fuel costs weakened cargo turnover and discouraged opportunistic fixtures. China remained the major buyer, importing 0.36 mnt.

Peru posted the sharpest downturn, with exports dropping 51.3% w-o-w to 0.45 mnt, reversing last week’s exceptional surge. San Nicolas exported 0.34 mnt and Matarani 0.11 mnt. The decline was led by weaker spot pull from China and fewer working stems, while rising freight and bunker costs made long-haul voyages less attractive to both charterers and exporters. China imported 0.45 mnt, including 0.34 mnt from Shougang Hierro.

Freight sentiment and impact on iron ore shipments

Freight momentum strengthened in week 48 on the back of winter-driven demand and firmer chartering activity across both the Atlantic and Pacific. Capesize and Supramax availability tightened steadily, while forward freight expectations turned increasingly bullish, lending support to sentiment and stimulating competitive fixing interest across major trade lanes.

However, elevated bunker costs and uneven rate performance across long-haul routes curbed aggressive fixture appetite. Vessel operators adopted a cautious approach to positioning, which moderated spot shipment growth from key exporters including Australia, Brazil, Peru and Chile. This restraint persisted despite stable export fundamentals and an overall improvement in freight market sentiment.

Outlook

Global iron ore exports are expected to stabilise with a slight upward bias in December, supported by improving winter restocking demand and firm sentiment in the Capesize and Supramax markets. Vessel supply remains broadly balanced, but sustained firmness in freight and bunker costs could limit short-term upside for long-haul shipments. South Africa is likely to maintain steady flows, while a rebound from Australia and Brazil will depend on whether Chinese and Indian buyers accelerate spot procurement heading into December.

Leave a Reply