- Weak Indian demand, soft Pacific rates slow down shipments

- Indonesia witnesses rebound in exports after 2 muted weeks

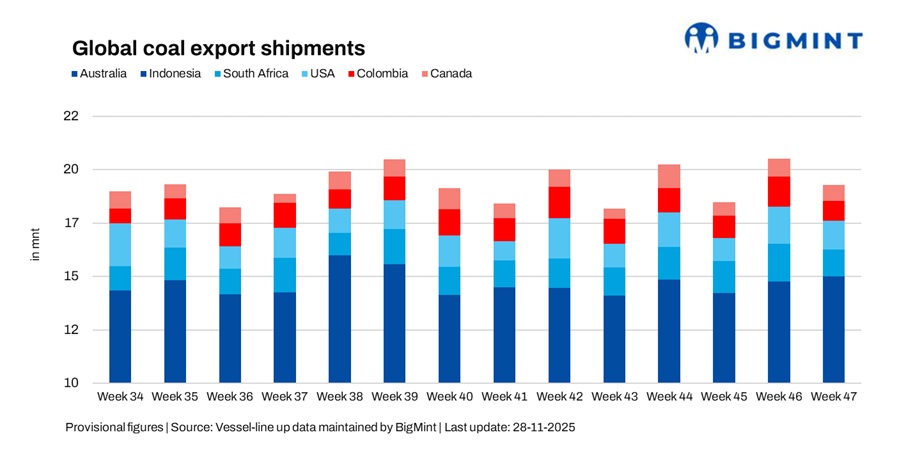

Global seaborne coal exports fell 5.7% w-o-w to 18.96 million tonnes (mnt) in week 47 (15-21 November 2025) from 20.09 mnt in week 46 (8-14 November), according to BigMint’s vessel line-up data. The pullback was led by a steep drop in shipments from South Africa and Colombia, while declines in Australia, the US and Canada further contributed to the softness. Indonesia acted as the only major support to total volumes, recording a strong rebound after two muted weeks.

The fall in shipments reflected weaker buying interest from India and muted procurement from select Northeast Asian utilities, alongside easing Pacific freight rates that reduced fixing momentum for some exporters. Although Atlantic sentiment stayed firm, a limited number of spot fixtures kept the improvement from translating into a broader rebound. Improving vessel availability across the Pacific also influenced owners to accept more competitive levels, moderating export flow into India and Southeast Asia.

Country-wise trends

Australian exports ease after multi-week peak

Australia’s coal exports fell 3% w-o-w to 7.46 mnt in week 47 from 7.69 mnt in week 46, easing after touching a five-week high BigMint says. Loadings at Newcastle (3.14 mnt), DBCT (1.60 mnt) and Gladstone (1.48 mnt) were largely stable, but a slight decline in cargo nominations and softer spot demand from India and Japan slowed shipment momentum. Weather remained favourable, supporting port operations throughout the week.

However, lower Pacific freight rates played a key role in limiting export growth as owners were less inclined to aggressively position vessels on the Australia-India route, keeping fixtures contained despite strong operational fundamentals. Japan (2.11 mnt) and China (1.78 mnt) led import demand, while Glencore (1.20 mnt) and BHP Shipping (0.67 mnt) emerged as the major shippers.

Indonesia rebounds sharply on stronger cargo flow

Indonesia’s coal exports surged 6.4% w-o-w to 7.33 mnt in week 47 from 6.89 mnt the week prior. Higher cargo nominations from East and South Kalimantan drove the increase, supported by improved logistics that facilitated faster vessel turnaround. Loadings were led by Taboneo (1.53 mnt) and Bunati (1.33 mnt), reflecting strong operational momentum during the week.

Rising demand from China (3 mnt) and steady interest from India (1.25 mnt) helped offset subdued Indian spot buying, sustaining overall shipment levels. However, competition from Australian cargoes kept pricing pressure intact, preventing a stronger rebound despite the improved trade flow and steady vessel activity.

South African exports drop sharply amid logistical disruptions

South Africa’s iron ore exports dropped sharply by 26.1% w-o-w to 1.25 mnt in week 47 from 1.69 mnt in week 46 – the biggest fall among major exporters. The decline was mainly due to rail-to-port delays and cargo allocation issues, which slowed operations and limited shipments through Richards Bay.

Even though Atlantic freight sentiment remained strong, exporters couldn’t increase volumes because most cargo was tied to long-term contracts, leaving little room for spot sales. Weak sponge iron demand in India further reduced spot fixtures, although India still emerged as the top importer with 0.48 mnt.

Colombia sees major slowdown as loadings dip

Colombia’s coal exports fell 33.4% w-o-w to 0.88 mnt in week 47 from 1.33 mnt in week 46, marking a sharp reversal after last week’s rebound. Lower cargo availability at Puerto Nuevo (0.36 mnt) and Puerto Bolivar (0.30 mnt), along with fewer working stems, significantly reduced weekly shipment momentum despite stable terminal operations.

Even though Atlantic freight sentiment remained firm, exporters avoided over-nominating vessels due to weaker short-haul buying interest from European markets. Shipments were primarily headed to Brazil (0.23 mnt) and South Korea (0.17 mnt), while Prodeco Group (0.45 mnt) and Cerrejon Mines (0.30 mnt) emerged as the major shippers during the week.

US exports ease after previous week’s spike

US coal exports dipped 22.1% w-o-w to 1.31 mnt in week 47 from 1.68 mnt in week 46, reversing the strong momentum seen earlier. Reduced loading activity at Norfolk (0.64 mnt) and Baltimore (0.31 mnt) slowed overall turnover and weighed on weekly volumes.

On the demand side, India (0.30 mnt) and Turkey (0.23 mnt) provided steady support, but a quieter European market held back fresh fixtures. With limited buying interest from Europe, exporters struggled to maintain last week’s pace despite stable demand from select markets.

Canada records mild decline as weather support stabilises

Canada exported 0.73 mnt in week 47, down 10.5% w-o-w from 0.82 mnt in week 46. Shipments were handled mainly through Roberts Bank (0.30 mnt), Vancouver (0.27 mnt) and Prince Rupert (0.17 mnt). Despite stable weather, early-week rail congestion restricted port throughput and capped overall volumes.

Northeast Asian demand continued to lend support, but fewer fresh spot cargoes kept exports from rising further. South Korea (0.25 mnt) and Japan (0.22 mnt) remained the top importers, while Elk Valley Resources led shipments with 0.27 mnt.

Coal freight rates see mixed signals

Coal freight sentiment to India remained mixed during the week, with rates in the Pacific basin softening while the Atlantic basin held firm. Improving vessel availability and subdued buying from Indian importers weighed on freight levels for Australia-India and Indonesia-India routes, slowing fixture momentum and capping shipments from these regions BigMint reported.

Meanwhile, the Atlantic market found support from tighter tonnage lists and stronger export offers, though limited fresh fixtures kept the gains from converting into higher volumes. Lower bunker prices eased operating costs for vessel owners, but abundant vessel supply continued to restrain freight upside, allowing only selective cargoes to command premium rates.

Outlook

In the near term, global seaborne coal exports are expected to remain steady to slightly soft in the near term, as mixed freight trends and inconsistent procurement from Indian importers continue to shape market movement. Pacific freight weakness may limit upside in Australian and Indonesian shipments, while firm Atlantic sentiment could support stabilisation in US and South African exports if logistical flow improves.

Buyers across India and Northeast Asia are likely to stay cautious given adequate stock levels, and any shift in demand or tightening of tonnage supply will be critical in determining freight-led support for cargo movement going forward.

Leave a Reply