- US scrap sentiment turns cautious as winter tightness eases

- Tight supply, low mill inventories support European prices

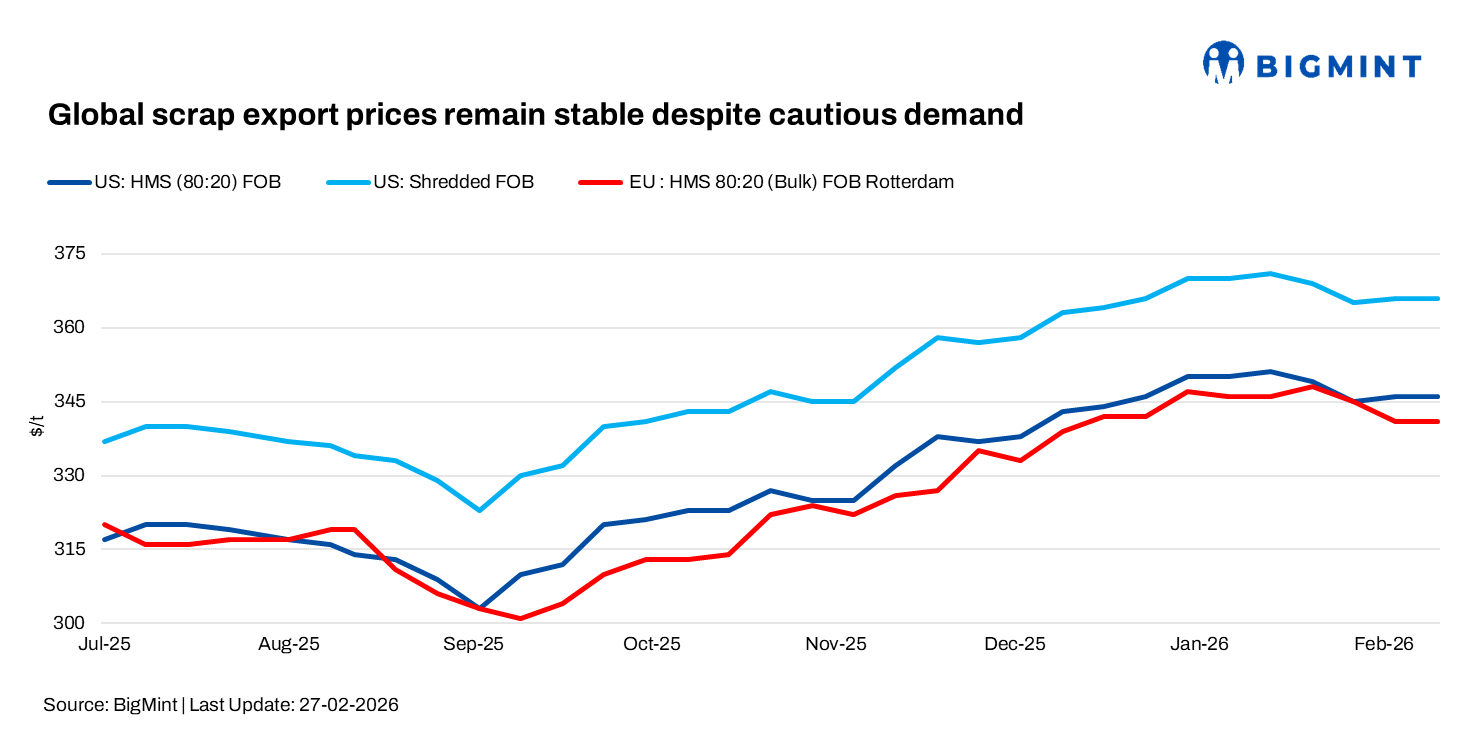

Global ferrous scrap export markets showed mixed trends during the week ended 27 February 2026. In the US, prices remained firm even as winter-related supply disruptions faded, while export demand stayed cautious. Europe remained supported by tight scrap availability and low mill inventories despite weak steel markets. Brazil was largely stable, and Ramadan-related slowdowns muted activity in the UK and UAE.

US

US scrap sentiment turned more guarded, with market participants suggesting the recent rally may be nearing its peak. Improving weather is expected to normalise yard inflows in March, easing supply tightness and shifting some leverage back to mills.

In February, Midwest prices rose by $28-30/t m-o-m amid tight winter supply. Busheling held at $450-455/t delivered Midwest and Southeast, respectively, while shredded remained at $445-450/t in both regions. Mill utilisation improved to 78%, indicating stable but not aggressive consumption.

Export prices were broadly steady. Fresh sales to Turkiye were heard last week at $375/t CFR for HMS 80:20 and $395/t CFR for shredded. Bangladesh bookings were reported at $375/t CFR Chattogram for HMS 80:20, though overall overseas demand remained subdued. With seasonal tightness gradually easing and export buying still cautious, further upside appears limited in the near weeks.

FOB – US East Coast (bulk)

CFR – US-origin HMS 80:20 (bulk)

Europe

The UK and Europe scrap market remained broadly stable but subdued. Yard inflows were modest, while demand from Turkiye and South Asia stayed cautious. Export activity was limited, with UK-origin containerised shredded sold at $370-374/t CFR Chennai. Offers to Pakistan were heard at $380/t against bids near $374-375/t, with a deal concluded at $377/t CFR Qasim.

Dockside UK origin HMS 80:20 was heard at GBP 215-225/t ($290-303/t) delivered and OA-grade at GBP 240-250/t ($323-337/t) delivered.

FOB assessments (Rotterdam, Europe)

- HMS 80:20 (Bulk): $341/t, stable w-o-w

Germany: German scrap prices rose in February as harsh weather restricted collections. E3 traded at EUR 310-315/t ($366-372/t) delivered, E40 at EUR 315-320/t ($372-378/t), and E8 at EUR 320-330/t ($378-389/t), up EUR 5-10/t ($6-12/t) m-o-m. However, weak steel demand may keep March prices stable.

Italy: In Italy, scrap prices increased by EUR 10-15/t ($12-18/t) m-o-m, with E3 at EUR 330-340/t ($389-401/t), E8 at EUR 345-355/t ($407-419/t), and E40 at EUR 345-350/t ($407-413/t) delivered. Strong domestic demand and poor inflows supported prices, though further gains may be difficult without export backing.

Brazil

Export prices were unchanged, with HMS at $285/t FOB and shredded at $305/t FOB. Both grades have gained $10/t since early February, supported mainly by improved buying sentiment from India. Market participants expect largely stable conditions in the near term.

Brazilian domestic scrap prices stabilised following moderate gains earlier in February. Domestic HMS 80:20 was assessed at BRL 810-820/t ($158-160/t) FOT, and turnings at BRL 730-740/t ($142-144/t), with limited fresh transactions reported.

Outlook

Global scrap export markets are expected to move sideways. Improved scrap availability in the US may limit further price increases, while tight supply in Europe could offer some support despite weak steel demand. Brazil is likely to remain stable, and Middle East buying may gradually improve after Ramadan.

Following the US Supreme Court’s 20 February ruling removing country-specific tariffs, more competitively priced European scrap may flow into the US. However, higher overall supply and the new 10% global tariff could keep US domestic scrap prices under pressure in the coming weeks.

Leave a Reply