- Africa, South America output falls on operational issues

- LME aluminium remains above $3,000 amid tight supply

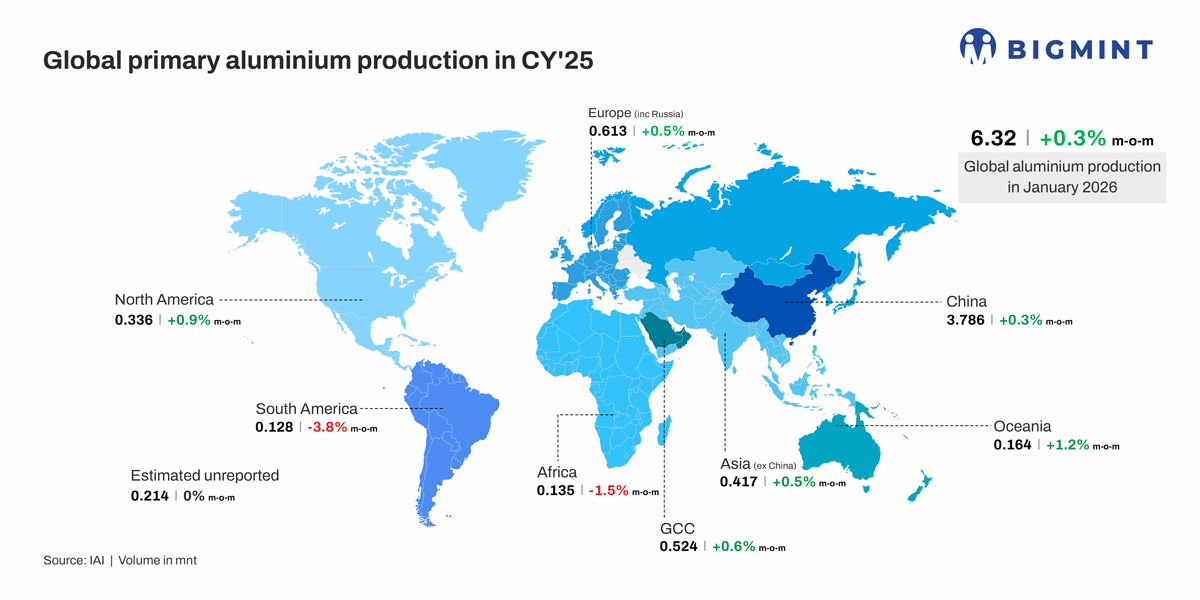

Global primary aluminium production stood at 6.32 million tonnes in January 2026, marking a 0.3% m-o-m increase from 6.30 million tonnes in December 2025. The marginal rise reflects steady smelter operations across key regions amid firm market fundamentals. Supportive price trends and relatively tight supply conditions continue to underpin overall production sentiment.

Country-wise breakdown

China, the world’s largest aluminium producer, reported output of 3.786 mnt in January 2026, up 0.3% m-o-m from 3.775 mnt in December 2025, further consolidating its dominant position in global supply. In contrast, Africa’s production declined 1.5% m-o-m to 0.135 mnt, while South America recorded a 3.8% m-o-m decrease to 0.128 mnt, reflecting ongoing operational and cost-side pressures in parts of the region.

North American output increased 0.9% m-o-m to 0.336 mnt. Asia (excluding China) saw a 0.5% m-o-m rise to 0.417 mnt, while Europe (including Russia) posted a 0.5% m-o-m uptick to 0.613 mnt. Oceania’s production grew 1.2% m-o-m to 0.164 mnt, and the GCC region recorded a 0.6% m-o-m increase to 0.524 mnt. Estimated unreported production remained unchanged at 0.214 mnt.

Overall, global aluminium output in January 2026 reflected broadly firm m-o-m trends, supported by gains in China, North America and the GCC, which offset declines in parts of Africa and South America, highlighting continued regional disparities in smelter performance and cost competitiveness.

Global aluminium output steady amid tight supply conditions

Global primary aluminium production reached 6.32 million tonnes in January 2026, up slightly from 6.30 mnt in December. The marginal rise reflects steady smelter operations across major producing regions and disciplined output management, particularly in China. The country produced around 3.79 mnt, operating near its 45 million tonne annual capacity cap, which limits rapid supply growth but ensures consistent output. China’s dominant position continues to underpin global supply and price resilience.

Production in Africa and South America declined due to high energy costs, constrained power supply, logistical disruptions, and operational challenges that limited smelter utilisation. In South America, additional pressure from softer downstream demand further restricted output, tightening regional supply and supporting underlying price levels. These declines highlight ongoing regional disparities in production efficiency and cost competitiveness.

Conversely, North American output edged higher, driven by improved smelter utilisation and steady demand from downstream sectors such as automotive, construction, and packaging. Similarly, modest growth was observed in Asia (excluding China), Europe, Oceania, and the GCC region, supported by stable operations, competitive energy access, and disciplined production strategies. These regions contributed to overall global production gains, offsetting declines elsewhere.

Overall, global aluminium production in January 2026 remained broadly firm, underpinned by steady smelter performance, tight supply conditions, and ongoing operational discipline. While China and North America led the gains, persistent energy, regulatory, and logistical constraints in Africa and South America limited output growth, maintaining structural supply tightness and supporting global market fundamentals.

Global aluminium capacity to rise over 4% by end-2026

Global primary aluminium operating capacity is set to increase by 20.9 million tonnes, or 4.58%, reaching around 77.16 million tonnes by the end of 2026, with Indonesia leading incremental additions. Global production grew marginally to 73.78 million tonnes in 2025, constrained by China’s 45 million tonne cap. While demand from automotive and construction sectors remains steady, the market is expected to stay in deficit in 2026, easing only as new overseas projects come online in 2027.

Impact of pricing

LME aluminium prices rose by $243/t m-o-m in January 2026, climbing to $3,153/t from $2,910/t. Meanwhile, LME inventories declined by 4%, easing to 0.50 mnt from 0.52 mnt over the same period.

Aluminium prices strengthened in January 2026, driven by tightening global supply and ongoing inventory drawdowns. China’s output remained near its 45 mnt capacity, while limited expansion in energy-constrained regions like Europe reinforced market tightness. Higher US import tariffs reduced physical availability and elevated regional premiums.

LME aluminium traded above $3,000/t, supported by firm demand and constrained inventories, signaling a structurally tight market outlook for 2026.

Outlook

Global aluminium supply is expected to remain structurally tight in 2026, with China operating near its 45 million tonne capacity ceiling and limited new additions elsewhere. Energy constraints, feedstock availability, and cautious investment across key regions are likely to keep primary supply growth modest. With LME prices sustaining above $3,000/t, declining inventories, and US trade measures limiting physical availability, steady demand from automotive, construction, renewables, and electrification sectors is expected to maintain a tight market balance, supporting a firm price outlook through the year.

Leave a Reply