- Prices rise on tight prompt supply, logistics disruptions

- Coal becomes cheaper alternative, prices lower by $10-15/t

The global petroleum coke market has turned firm over the past few weeks, with prices rising across most regions. However, the real story is unfolding in India, where higher petcoke prices are beginning to face resistance from buyers and are quietly changing how cement companies manage their fuel costs.

Global prices firm up across regions

Petcoke prices have strengthened across both the Atlantic and Pacific markets. Tight supply, logistical disruptions, and uncertainty in key producing regions pushed up offers, particularly for high-sulphur fuel-grade coke.

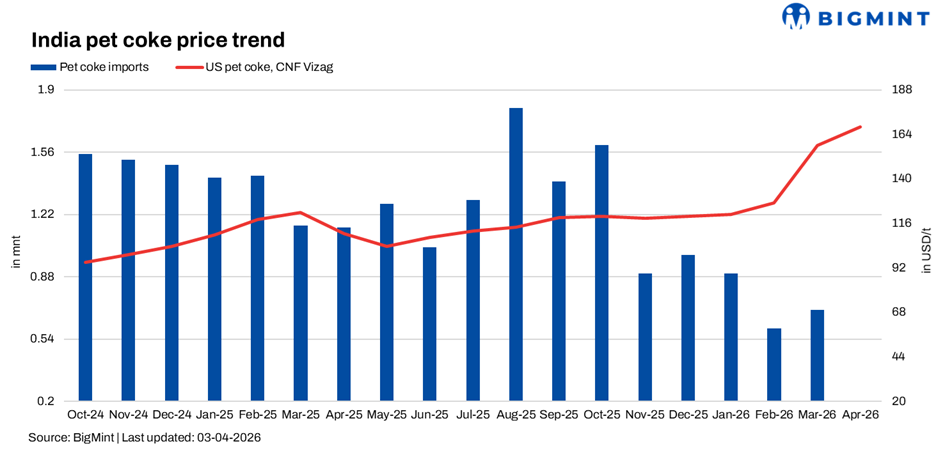

India sees sharp price jump

In India, the market has moved quickly. Within a short span of time, petcoke offers have climbed from the mid-$150s to the high-$160s in early April and even touching $170/t CFR in some cases.

However, while sellers have raised prices, buyers have not followed with the same enthusiasm.

Most buyers are still comfortable bidding closer to the mid-$150s, creating a notable gap between what sellers want and what buyers are willing to pay. This gap is now defining the market.

Supply tightness drives market

The primary reason for rising prices is tighter availability.

Supply disruptions in key exporting regions have reduced prompt cargo availability. At the same time, logistical challenges and uncertainty in global trade flows have made sellers more cautious about committing volumes.

Buyers turn cautious, delay purchases

Despite the rise in prices, buying activity — especially in India — has remained measured.

Cement producers and traders are not rushing to secure cargoes. Instead, many are drawing down existing inventories, waiting for price clarity, and holding back in anticipation of better buying opportunities.

This cautious approach is preventing the market from moving higher at a faster pace.

Coal starts competing again

One of the most important shifts in the market is the return of coal as a strong competitor to petcoke.

As petcoke prices have increased, coal has become relatively more attractive on a cost basis. This is especially true for high-CV imported coal used in cement kilns and lower-cost coal used in blended fuel strategies.

Several cement plants have already started adjusting their fuel mix. Instead of relying heavily on petcoke, they are increasing coal usage, optimising blends to reduce fuel costs, and comparing fuels more actively than before.

In some cases, coal is now cheaper by around $10-15/t, which is enough to influence buying decisions.

Cement sector feels pressure

The impact of rising petcoke prices is clearly visible in the cement sector.

Fuel costs have gone up, putting pressure on margins. Producers are trying to pass on these costs through higher cement prices, but demand conditions are not strong enough to fully support these increases.

As a result, margins are tightening, cost optimisation has become critical, and fuel flexibility is becoming more important than ever.

This is why the shift towards coal is gaining momentum.

A market divided between buyers and sellers

The petcoke market today is split into two clear sides.

On one side are the sellers, who are holding firm on higher prices due to tight supply.

On the other side are the buyers, who are resisting these prices and adjusting their fuel strategies instead.

This has created a market where actual trades are limited. Until one side gives way, this imbalance is likely to continue.

Outlook

The direction of the market will depend on how a few key factors evolve.

If supply remains tight, prices could continue to stay firm or even move higher. However, if supply improves or if demand weakens further, prices may struggle to hold current levels.

At the same time, the role of coal will be crucial. If coal continues to remain cheaper, more cement plants will shift away from petcoke, limiting demand.

In the near term, the market is likely to remain balanced but tense — caught between firm global supply conditions and cautious, price-sensitive demand in India.

Leave a Reply