- Indian production to reach record high in 2024-25

- Indian exports increase by 34% y-o-y in Jan-Sep’25

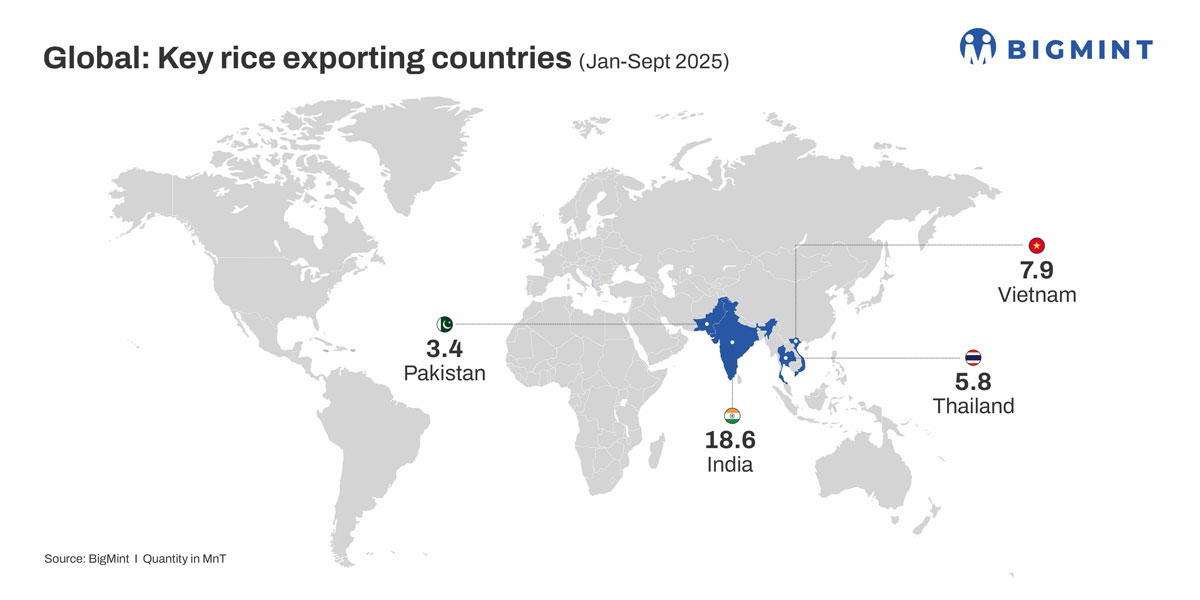

The global non-basmati rice market continues to experience ample supply, with exports from key regions rising y-o-y in January-September 2025.

During this period, India remained the dominant non-basmati rice supplier, with exports of 18.6 million tonnes (mnt), up 34% y-o-y from 13.9 mnt in January-September 2024, as per BigMint data. These volumes put it far ahead of Vietnam, which recorded an 11% increase to 7.9 mnt in January-September 2025 compared to 7.1 mnt in the year-ago period. The third-largest supplier, Thailand, exported 5.8 mnt during this period, though the year-ago volumes are not available. However, Pakistan’s exports fell by 19% y-o-y to 3.4 mnt against 4.2 mnt.

With the bulk of global trade driven by these origins, abundant supply has kept international markets well-balanced despite regional weather disruptions. Although heavy rains and flooding temporarily disrupted crops in Vietnam, Indonesia, and Sri Lanka, the resulting supply constraints did not drive up price significantly due to strong harvest prospects elsewhere.

Additionally, the Philippines’ decision to restrict rice imports until 31 December 2025 has forced traditional exporters such as Vietnam to scout for alternative buyers, adding competitive pressure to the trade.

India, Thailand, Pakistan, and Vietnam are now navigating an aggressive pricing environment. India currently holds a price advantage against Thailand and Vietnam, while Pakistan offered the lowest quotes, with sales at $340/tonne (t) in Bangladesh.

India’s production strengthens, stockpiles remain abundant

India’s non-basmati production is projected to reach a new record of 125.4 million tonnes (mnt) in 2024-25, backed by 44.1 million hectares of kharif sowing and robust government procurement. Domestic supply conditions are further supported by sizeable government inventories, with the Food Corporation of India holding an estimated 33.6 mnt of rice and 30.9 mnt of paddy — the highest stock position in nearly a decade.

While the broader supply situation indicates stability, traders flag selective tightness in premium varieties such as Sona Masuri and BPT due to lower expected availability. Still, no major supply-driven price risk is visible for mainstream non-basmati grades.

Global demand softens but trading interest may revive gradually

African demand, a major driver for India, remains subdued, though traders expect enquiries to pick up if price spreads widen in favour of Indian cargoes. The International Grains Council (IGC) forecasts 2025-26 global rice production at 543-544 mnt, signalling continued abundance and easing concerns of tightness early next year.

With rising supply, heavy stocks, and cautious import programmes among major buyers, the market is likely to stay within a narrow trading band. Analysts do not anticipate steep appreciation in prices unless weather-related disruptions or policy shifts alter the supply narrative.

Leave a Reply