- Chinese coke exports drop 15% y-o-y

- India sees imports dropping 13% on-year

- Trade balance shifts to Asia, oversupply worries linger

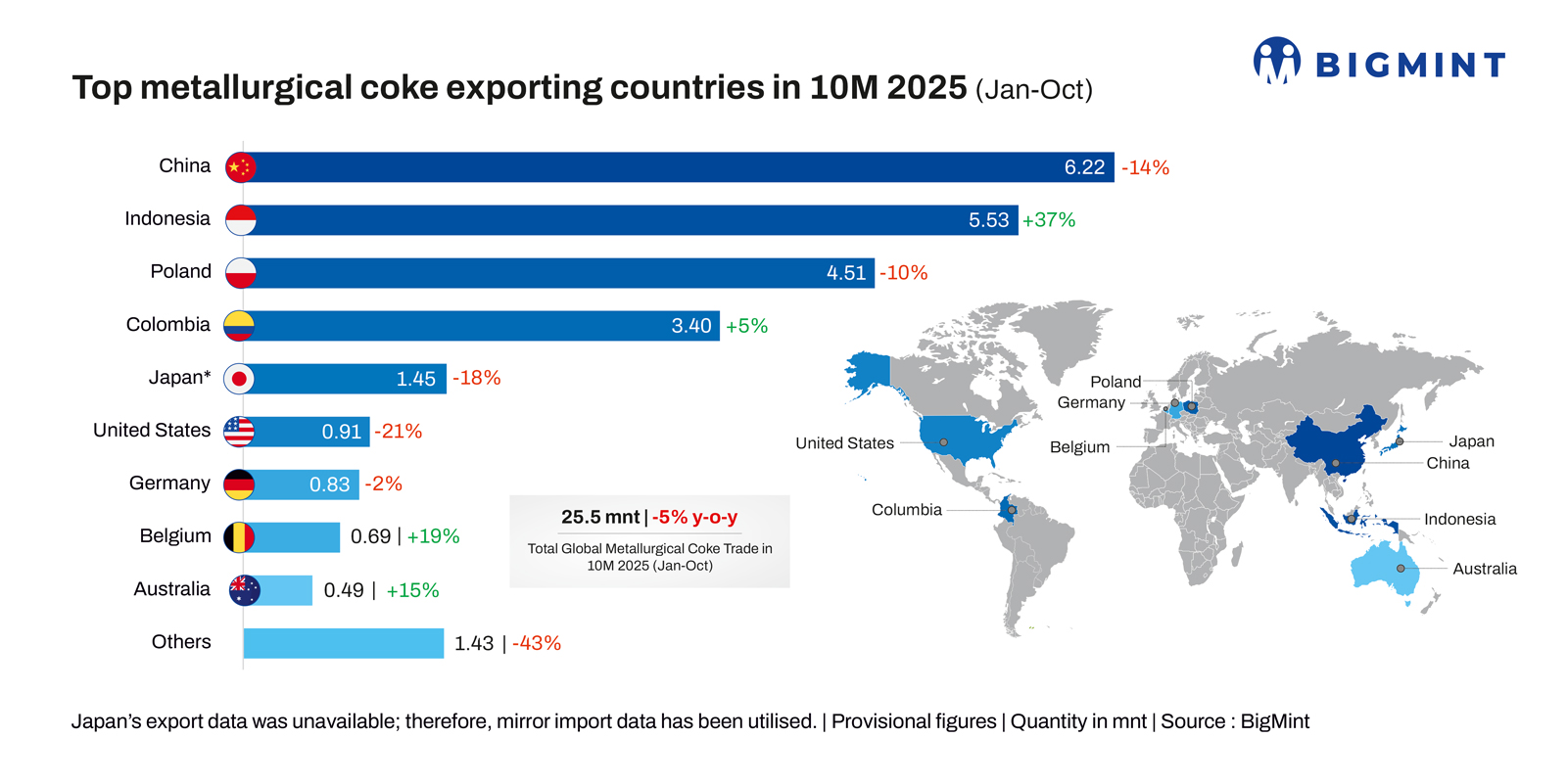

Morning Brief: Global metallurgical coke, or met coke, exports fell by approximately 5% y-o-y in January-October 2025 (10MCY’25) to around 25 million tonnes (mnt), as per latest data with BigMint. The coke market remained under pressure for the greater part of 2025 as world crude steel production fell by 2.1% y-o-y in 10MCY’25.

The coke market and trade dynamics remained under pressure due to declining BF-BOF steel production in China, Japan and the EU. Tariffs and trade remedial measures, upcoming CO2 border regulations and declining global steel prices weighed on the coke market.

However, the relative strength in global coking coal prices following supply tightening in key countries and shortage of premium grade coal amid growing trade concentration and competition in Asia have also been key factors driving coke market dynamics.

Highlights of trade flow in 10MCY’25

China’s coke exports drop 15%: China’s exports of met coke fell by 15% y-o-y in 10MCY’25 as exports to major Asian buyers – India and Malaysia -edged down significantly due to quantitative restrictions on coke imports by India, anti-dumping investigations, and AD duty on flat steel product imports by Malaysia, harming mainly Chinese exports. On the other hand, exports to Indonesia increased due to re-routed shipments intended for sales to other destinations via Indonesia.

On the domestic front, Chinese crude steel output fell by 3.9% on-year in 10MCY’25 while the decline in pig iron production was slower – at just 1.1% in 9MCY’25 but 8% y-o-y in October. Restrictions on domestic coal mining led to tight domestic coking coal supplies in China, which supported the coke market although too feeble to offset the sharp deceleration in demand.

Mysteel’s survey of 30 merchant coke-makers in China showed that throughout most of October they kept losing money on coke sales, with their average loss hitting RMB 41/t in late October, the largest loss since early August. As of 30 October, coke producers were still losing RMB 32/t. So, the domestic market remains under cost pressure even as winter steel production cuts gather steam and export sentiments in Asia remain weak.

Indian coke imports down 13%: While India’s coking coal imports climbed 5% y-o-y in 9MCY’25, as per BigMint data, on the roughly 10% y-o-y surge in crude steel output, coke imports fell sharply by 13% during the review period. This was due to the DGFT sanctioning the imposition of quantitative restrictions on imports of low-ash metallurgical coke till December of this year. The restrictions include country-wise quotas for imports.

Again, in November, the DGFT issued its preliminary findings in the anti-dumping investigation on imports of LAM coke from Australia, China, Colombia, Indonesia, Japan, and Russia, concluding that the domestic industry has suffered material injury due to dumping from these six countries and proposing AD duties for each origin. Import volumes from the subject countries were shown to have increased by 179% throughout the injury period.

Global trade pivots around Asia: At a time of dwindling steel production worldwide and deepening concerns around sustainability, the global coke market would appear to be under a lot of pressure. However, Southeast Asia remains the sole glittering exception even as the EU, China, JKT gradually lose the demand momentum.

Indonesia is moving its capital to Nusantara, a project expected to drive a massive construction boom and demand for steel and coke. Vietnam is progressing with its North-South High-Speed Railway, set to begin construction in 2027. Spanning over 1,500km, it will also require vast quantities of steel. Thailand’s Eastern Economic Corridor (EEC), a $45 billion development zone, is attracting foreign investment in manufacturing, logistics and infrastructure.

Indonesian overcapacity concerns: Despite coke exports to India dropping over 25% on-year, Indonesia’s total exports surged nearly 40%, thanks to higher shipments directed by mainly Chinese operators of new Indonesian coking facilities to Latin America and other countries. Indonesia’s met coke production has been steadily rising due to new projects coming online. Its total operational capacity of coke reached around 12 mnt tonnes in 2024.

While Southeast Asia has a strong demand potential, it is still unlikely to fully absorb this increased coke production capacity. Market participants are unsure if demand from infrastructure projects will completely offset the effect of trade barriers imposed by India.

Polish coke exports bear India QR brunt: Poland, a leading coke exporter, saw volumes sliding 10% y-o-y in 10MCY’25 because shipments to India dropped over 25% during the review period, as well as weak steel production and market conditions in leading EU countries such as Germany.

For instance, Poland’s JSW, the top producer and exporter of coke, exports 35% of its total production to India. The coking coal miner coke producer, battered by weak EU demand, is withstanding severe capacity underutilization and decline in exports resulting from competition from emerging Indonesian supply.

Outlook

Among the other traditional coke exporters, Japanese exports sunk 18% y-o-y mainly because of the sharp drop in shipments to the UK as Britain drastically cut its dependence on traditional BFs which are making way for state-of-the-art new steel production facilities. However, exports to India increased and, with the DGFT proposing the lowest AD duty among other counties for Japan, shipments may remain steady even as steel production in Japan remains depressed.

At roughly an AD duty of $120/t on coke imports from China, market participants in India are of the view that landed costs will remain at the same level as domestic prices. Increasing domestic coke output after the AD duty and QRs will offset some import demand. However, if cost parity is maintained with rising domestic prices in India, imports will still remain attractive due to tight domestic supply.

Leave a Reply