- Coking coal prices soften marginally, Chinese supply risks support sentiment

- Indonesian met coke prices rise $7/t w-o-w but Indian buyers show resistance

The global metallurgical coal complex is entering the second half of 2026 caught between two competing forces. On one hand, supply-side disruptions and rising production costs are lending support to coking coal, PCI and metallurgical coke prices. On the other, weak steel profitability across major consuming regions is limiting buyers willingness to accept higher prices.

The result is a market that remains fundamentally supported but increasingly vulnerable to demand-side resistance, as steelmakers across Asia, Europe and North America grapple with narrowing margins.

Supply concerns keep a floor under met coal prices

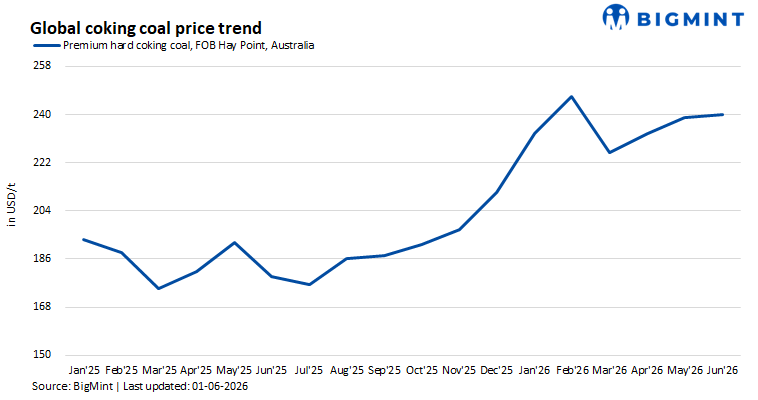

Seaborne coking coal prices softened marginally at the end of May, but the broader market continues to exhibit signs of resilience.

Australian premium hard coking coal (PHCC) was assessed at $240/t FOB Hay Point on 1 June, down $1/t d-o-d but still more than $19/t above levels seen three months ago. BigMint’s Premium Hard Coking Coal assessment at CNF Paradip stood at $267/t, while the weekly BigMint coking coal index remained steady at $268/t.

The modest decline masks a market increasingly influenced by supply-side risks rather than demand growth. Following the fatal mine accident in Shanxi, Chinese authorities have intensified mine inspections and safety reviews. While the immediate impact on seaborne buying has been limited, concerns over potential disruptions to domestic coal production have helped underpin sentiment across the premium coal segment.

The support is particularly visible in the low-volatility segment. Australian low-volatility (low-vol) hard coking coal (HCC) was assessed at $185/t FOB Hay Point, unchanged on the day and up from $177/t three months ago. A 75,000 t cargo of Carborough Downs for June loading traded at the same level on 28 May, indicating that buyers continue to support mid-tier premium coal brands despite broader market uncertainty.

Chinese import prices tell a similar story. Canadian HCC delivered into Rizhao was assessed at $229/t CNF China, while Russian semi-hard coking coal delivered into Jingtang reached $188/t, both significantly above levels prevailing earlier this year.

Meanwhile, the US East Coast met coal market is facing a different challenge. Weak spot demand and competition from Australian material continue to pressure US low-vol and high-vol coal producers. While Australian premium coal has benefited from Chinese supply concerns, US exporters remain dependent on price-sensitive Asian buyers and are finding it increasingly difficult to maintain margins.

Russian PCI gains influence in Asian markets

The PCI market is undergoing a structural shift as Russian material continues to gain market share across Asia. A 75,000 t cargo of Russian low-vol PCI for July loading traded at $156/t on 28 May, reflecting growing acceptance of Russian-origin material among Asian buyers.

The deal closely aligns with BigMint’s assessment of Australian low-vol PCI at $156/t FOB Hay Point and highlights the increasing competitiveness of Russian PCI in a market traditionally dominated by Australian suppliers.

In China, imported PCI prices have risen sharply over recent months. Low-vol PCI delivered into Jingtang was assessed at $145/t CNF China, up from $128/t three months earlier.

For Indian buyers, Australian PCI was assessed at $181/t CNF Paradip. Although demand remains cautious, the market has found support from tightening supply and a reduction in available alternatives.

The growing role of Russian PCI is reshaping trade flows throughout Asia and helping establish a firmer floor beneath PCI prices despite weak steel production growth in several key markets.

Met coke becomes the market’s primary bullish driver

The strongest upward momentum within the steelmaking raw materials complex is now coming from metallurgical coke.

Rising coking coal costs are increasingly being passed through the value chain, forcing coke producers to seek higher prices even as buyers resist.

Chinese domestic coke prices continue to strengthen. Tangshan quasi-grade-I coke was assessed at RMB 1,610/t ($238/t), up more than 15% over the past three months. Chinese exporters have followed suit, with 64% coke strength after reaction (CSR) coke FOB Tianjin assessed at $254/t, up $27/t from three months ago.

The same trend is evident in India.

BigMint’s assessment for Indonesian-origin 65% CSR coke delivered to India’s east coast rose $7/t w-o-w to $309/t CNF, while Chinese-origin 64% CSR coke increased to $267/t CNF. Both products have gained more than $25/t since early March.

Indonesian producers are attempting to push prices even higher. Market indications suggest August-loading cargoes are being offered at $285-287/t FOB Bahodopi as producers seek to recover escalating raw material costs.

Yet the market is far from uniformly bullish.

Indian buyers continue to resist higher imported coke prices, citing anti-dumping duties and weak steel demand. Domestic blast furnace coke prices at Jajpur and Gandhidham have remained largely stable, highlighting the disconnect between international and domestic markets.

The widening gap suggests that while producers are attempting to transfer higher coking coal costs downstream, the ability to do so remains constrained by steel sector profitability.

Steelmakers push back as margin pressures intensify

The central theme emerging across the global metallurgical complex is the growing tension between rising raw material costs and weak steel economics.

In China, mills are facing a fifth round of coke price increases, adding further pressure to production margins. Although steel demand has shown signs of stabilisation, many mills continue to focus on reducing input costs wherever possible.

In India, sluggish steel and pig iron demand has limited appetite for additional coke and coking coal purchases despite relatively healthy inventory positions.

Across Southeast Asia, buyers have largely adopted a wait-and-see approach, preferring to purchase only when necessary rather than chase rising offers.

In North America, met coal producers continue to struggle to achieve desired pricing levels as Asian buyers push back against higher costs and European demand remains largely contract-driven.

The common thread across all regions is clear: steelmakers are becoming increasingly reluctant to absorb additional raw material inflation without a corresponding improvement in finished steel prices.

Outlook

The global metallurgical coal complex enters the summer period with stronger fundamentals than were evident earlier in the year.

Chinese mine disruptions, rising coke prices, growing Russian PCI participation, and disciplined Australian supply have collectively established a firmer price floor across much of the market.

However, the next phase of the rally will depend less on supply concerns and more on the health of the steel industry. Unless steel demand improves sufficiently to restore mill profitability, buyers are likely to continue resisting higher coal and coke prices. This suggests further gains may be gradual rather than explosive.

For now, the market remains caught between tightening supply and fragile demand-a balance that is keeping prices supported but preventing a decisive breakout higher across the metallurgical raw materials complex.

Leave a Reply