- Lead market posts 7,000 t surplus despite stable mine output

- Zinc surplus reaches 145,000 t on stronger refined production

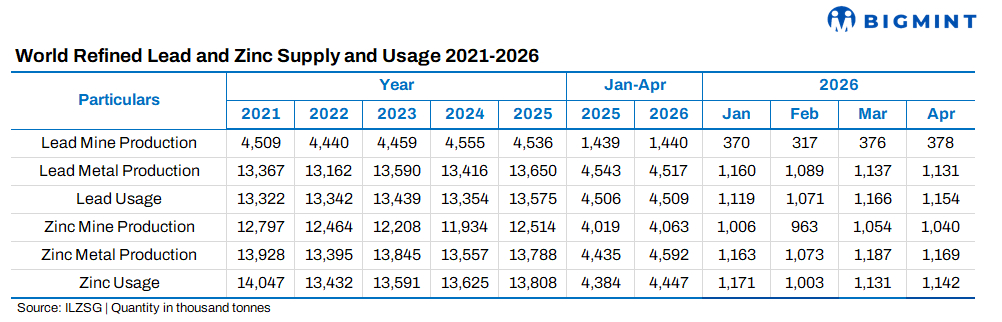

The global refined lead market recorded a surplus of 7,000 tonnes (t) during January-April 2026, while the refined zinc market remained significantly oversupplied with a surplus of 145,000 t, according to preliminary data released by the International Lead and Zinc Study Group (ILZSG). Reported lead inventories increased by 48,000 t during the period, while zinc stocks rose by 58,000 t, reflecting continued supply growth amid moderate consumption trends.

Lead market balanced by weak production and demand growth

Global lead mine production remained largely unchanged year-on-year, as higher output in Portugal and Türkiye offset declines in China, Sweden and the United States. Refined lead production slipped 0.6%, weighed by lower output in China, Mexico and South Korea. Brazil, however, reported higher production following the commissioning of additional secondary lead capacity in 2025.

Refined lead consumption increased marginally by 0.1%, supported by stronger demand in Brazil, Spain and the United States. These gains were largely countered by weaker usage across Argentina, Mexico, South Korea, Türkiye and the UK.

Chinese imports of lead contained in concentrates rose 4.7% y-o-y to 412,000 t, while net refined lead imports surged to 126,000 t, up by 122,000 t from the corresponding period last year.

Zinc surplus expands on higher Chinese output

Global zinc mine production rose 1.1% y-o-y, supported by output growth in Portugal, the Democratic Republic of Congo, Brazil, China, Mexico and Russia. Production at Portugal’s Aljustrel mine and Congo’s Kipushi mine contributed significantly to the increase. Lower output from Peru, Sweden and the US partially offset gains.

Refined zinc production climbed 3.5%, driven primarily by higher Chinese output, alongside increases in Brazil, Mexico, India, South Korea and Canada. Global zinc consumption grew 1.5%, supported by stronger demand in Europe, China, India, Türkiye and the US.

Chinese zinc concentrate imports rose 16% to 954,000 t, while net refined zinc imports fell by 86,000 t y-o-y to 35,000 t.

Outlook

Lead fundamentals remain broadly balanced, although rising Chinese refined imports indicate tighter domestic availability. Meanwhile, the zinc market is expected to remain in surplus in the near term, with expanding mine and refined output likely to outpace demand growth unless consumption improves more sharply across key industrial sectors.

Leave a Reply