- Shipments from Canada rise two-fold

- Lunar New Year lull caps fixing momentum

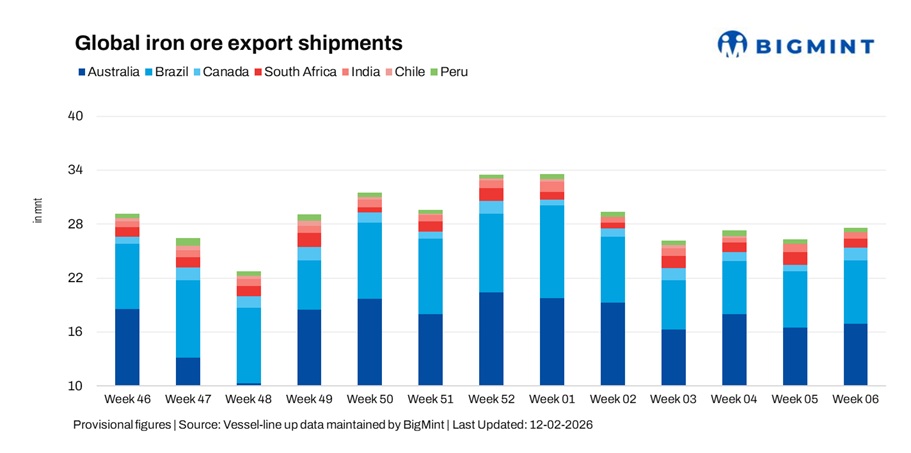

Global seaborne iron ore exports rose 4.8% w-o-w to 27.5 mnt in the week ended 06 February 2026, compared with 26.3 mnt in the previous week, as per vessel line-up data. The increase was supported by higher shipments from Brazil, Canada, and Australia, which outweighed declines from South Africa, India, and Peru. Export momentum strengthened on improved cargo scheduling and stronger long-haul flows, although overall market sentiment remained cautious amid softer Chinese demand signals and a seasonal slowdown around the Lunar New Year.

Despite the weekly rise, fixing activity remained selective as weaker freight fundamentals and subdued steel margins encouraged charterers to adopt a wait-and-watch approach. The market remained sensitive to shipment timing, with producers prioritising steady flow rather than aggressive volume expansion.

Country-wise trends

Australian exports rise slightly

Australia’s iron ore exports increased 2.5% w-o-w to 16.9 mnt, supported by stable cargo flow from key West coast terminals. Port Hedland led loadings with 10.03 mnt, followed by Walcott (3.29 mnt) and Dampier (2.92 mnt).

Rio Tinto led shipments at 6.21 mnt, followed by BHP (5.33 mnt) and FMG (3.48 mnt). China remained the main destination at 13.47 mnt, with Japan and South Korea importing 1.49 mnt and 1.02 mnt. Shipments stayed steady but timing-driven, with cautious fixing sentiment amid softer freight, while Pilbara hubs resumed operations after cyclone clearance.

Brazilian exports rise on stronger cargo flow

Brazil’s iron ore shipments rose 12.1% w-o-w to 7.1 mnt, supported by improved cargo availability and firmer export momentum from key terminals. Ponta Da Madeira led loadings with 2.95 mnt, followed by Tubarao (1.26 mnt), Itaguai (1.20 mnt), and Ilha Guaiba (1.08 mnt).

Vale shipped 4.03 mnt and CSN 2.46 mnt, with China remaining the key destination at 3.33 mnt amid cautious buying and weak margins. Despite improved volumes, long-haul fixing stayed selective due to freight weakness and demand uncertainty, while Vale’s output is expected to remain strong, supported by ramp-ups at Capanema and VGR1.

Canadian exports increase two-fold

Canada’s iron ore exports jumped 98% w-o-w to 1.4 mnt, recovering strongly after a weak previous week on improved cargo nominations and a return of Atlantic shipment flow. Sept-Iles led loadings with 0.71 mnt, followed by Port Cartier at 0.66 mnt.

AMNS led shipments at 0.66 mnt, followed by IOC (0.36 mnt) and Guinea & Nimba Mines (0.35 mnt), with the Netherlands remaining the top destination at 0.36 mnt. Canadian exports stayed volatile and timing-driven, though output is projected to exceed 55 mnt in 2026, supported by expanding capacity and resilient European demand.

South African exports fall

South Africa’s iron ore exports fell 25% w-o-w to 1.0 mnt, pressured by weaker cargo flow from the Saldanha Bay corridor. Saldanha handled 0.93 mnt, while Richards Bay contributed 0.11 mnt during the week.

The Netherlands emerged as the key destination, importing 0.20 mnt, reflecting selective European demand amid limited long-haul fixing. Meanwhile, South Africa has progressed discussions on a Framework Economic Partnership with China that could enhance duty-free access for mineral exports, including iron ore, while industry stakeholders continue to push for rail-port concession upgrades along the Sishen-Saldanha corridor to ease logistics bottlenecks.

South Africa remains a freight-sensitive exporter, with volumes highly timing-driven and vulnerable to infrastructure constraints.

Indian exports ease

India’s iron ore exports declined 26.1% w-o-w to 0.7 mnt, as east coast cargo flow softened after a strong previous week. Dhamra led shipments with 0.31 mnt, followed by Paradip at 0.23 mnt.

China remained the key destination, importing 0.42 mnt, with buying cautious amid weak steel demand and seasonal slowdown. India’s easing export regulations and port capacity upgrades at Paradip and Dhamra may support future export flows, though shipments remain timing-driven and freight-sensitive, with intermittent support from short-haul advantages.

Peruvian exports slip slightly

Peru’s iron ore exports slipped 4.6% w-o-w to 0.5 mnt, reflecting slightly weaker cargo movement and shipment timing adjustments. San Nicolas remained the sole active loading port, handling 0.50 mnt, while Shougang Hierro accounted for the entire volume.

China remained the sole destination, importing 0.50 mnt, underscoring Peru’s strong reliance on Asian demand. Shougang’s planned investment to extend the Marcona mine’s life may support long-term export stability, though shipments remain relatively steady but freight-sensitive and timing-driven.

Chilean exports remain nil

Chile’s iron ore exports remained nil during the week, unchanged w-o-w, as no cargoes were recorded, highlighting the country’s marginal and highly timing-driven export flow. Meanwhile, Chile’s mining export sector reportedly recorded its highest-ever January trade, while iron ore producers are advancing capacity expansion plans at units such as Cerro Negro Norte to improve long-term export flexibility.

Freight softens

Iron ore freight rates softened w-o-w due to weaker cargo demand and ample vessel availability. Capesize sentiment declined as shipment momentum from Australia and Brazil slowed, with miners showing limited urgency to fix amid muted price signals and stable inventories. Cautious Chinese procurement, comfortable port stocks, weak steel margins, and Lunar New Year disruptions further reduced spot activity, while rising ballasting and prompt tonnage availability intensified competition among shipowners, capping long-haul shipment expansion despite improved export volumes in Week 06.

Outlook

Global iron ore exports are expected to stay broadly steady but volatile in the near term, driven by cargo scheduling and selective fixing. Brazil and Canada may see some support from improved availability, though cautious Chinese buying, weak steel margins, and Lunar New Year disruptions could limit upside. Freight markets may remain under pressure due to ample vessel supply, aiding long-haul voyage economics, while Australia will remain the key swing factor in volumes, with South Africa and India likely to witness intermittent, logistics-driven fluctuations.

Leave a Reply