- Australia underpins weekly recovery in iron ore exports

- Selective fixing keeps export momentum uneven

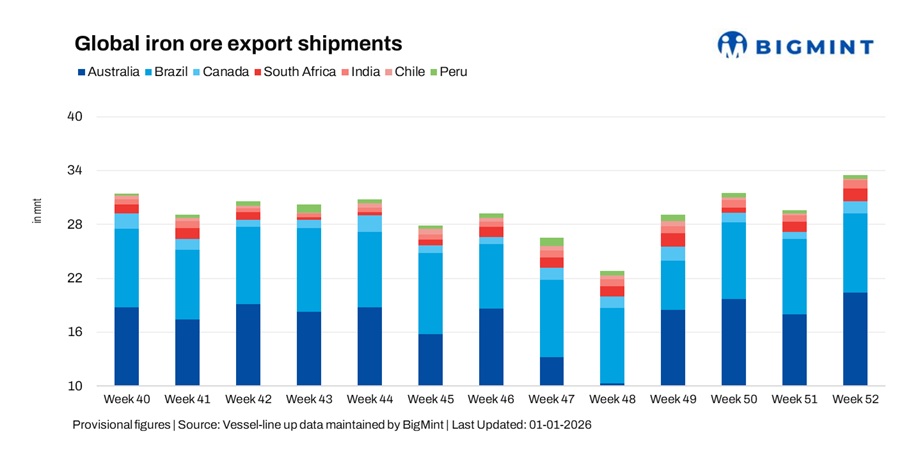

Global seaborne iron ore exports increased 13.5% w-o-w to 33.49 million tonnes (mnt) in the week ended 26 December, up from 29.50 mnt in the previous week, according to BigMint’s vessel line-up data. The rebound was primarily driven by stronger shipments from Australia, Brazil, India, Canada, and South Africa, which collectively outweighed continued weakness across some smaller exporting regions.

The weekly improvement came against the backdrop of a mixed but generally subdued freight environment, as holiday-related slowdown curtailed fixture activity and kept chartering largely selective. While the softer freight tone supported short-haul and opportunistic movements, long-haul shipment economics remained constrained, resulting in an uneven recovery across major iron ore origins.

Overall, week 52 reflected a cargo-driven rebound, aided by the release of deferred stems and improved port operations, rather than a broad-based improvement in freight market fundamentals.

Country-wise trends

Australia’s iron ore exports rebound despite cautious freight

Australia’s iron ore exports rose 13.5% w-o-w to 20.42 mnt, up from 18 mnt in the previous week, reflecting the normalisation of loading schedules at Western Australian ports and the movement of deferred cargoes ahead of the year-end. Port Hedland led loadings with 12.63 mnt, followed by Walcott at 4.10 mnt and Dampier at 3.37 mnt, highlighting steady operational performance across key regions.

Despite cautious Capesize freight sentiment and thin holiday fixing, Australia’s short-haul advantage into Asia continued to underpin volumes. Rio Tinto remained the largest shipper at 7.47 mnt, followed by BHP with 6.24 mnt and FMG at 4.78 mnt, reflecting balanced contributions from major producers.

China remained the dominant destination, importing 18.08 mnt, while Japan and South Korea imported 1.48 mnt and 0.39 mnt, respectively. Australia retained its position as the world’s largest iron ore exporter, supported by operational reliability and long-term supply commitment. However, China’s state-backed buyer CMRG’s push for tougher contract terms may influence future trade flows and pricing dynamics, adding uncertainty to the long-term export outlook.

Brazil’s iron ore flows tick up despite cautious fixing

Brazil’s iron ore exports increased 5.2% w-o-w to 8.8 mnt, compared with 8.4 mnt in the previous week. The modest rise reflected stable port operations and workable vessel positioning across key load ports, with Ponta da Madeira loading 3.17 mnt, followed by Itaguai at 2.12 mnt and Tubarao at 1.95 mnt.

However, shipment growth remained measured, as resistance to higher long-haul freight ideas and price-sensitive chartering limited more aggressive fixing. As a result, Brazilian exports improved modestly but continued to face freight-related constraints.

China remained the primary destination, importing 3.77 mnt, while Malaysia and Oman each received 0.39 mnt. On the supply side, CSN emerged as the leading shipper at 4.07 mnt, followed closely by Vale with 3.81 mnt, reflecting balanced contributions despite cautious demand conditions. Looking ahead, Vale’s guidance for more disciplined supply growth may influence Brazil’s future export volumes and long-haul Atlantic trade dynamics.

South Africa extends recovery from volatile base

South Africa’s iron ore exports rose 25.3% w-o-w to 1.41 mnt, up from 1.13 mnt in the previous week. The increase was driven by the continued movement of previously deferred cargoes, with Saldanha Bay accounting for 1.24 mnt of shipments, while Richards Bay contributed 0.17 mnt.

While volumes improved for a second consecutive week, soft long-haul freight sentiment and comfortable vessel availability continued to restrain more sustained export momentum, keeping shipments below recent weekly averages.

The Netherlands remained the leading destination, importing 0.87 mnt during the week, reflecting selective European demand amid cautious Atlantic market conditions. Looking ahead, stronger underlying production growth and the potential shift toward greener South Africa-Europe shipping routes could enhance the country’s longer-term export competitiveness and sustainability.

Canada rebounds sharply on improved cargo nominations

Canada’s iron ore exports surged 82.9% w-o-w to 1.4 mnt, rebounding from 0.8 mnt in week 51. The recovery was driven by higher cargo nominations and smoother Atlantic scheduling, following last week’s subdued activity. Sept-Iles handled 0.91 mnt, while Port Cartier loaded 0.47 mnt, reflecting improved throughput at key export terminals.

Despite the sharp rebound, exports remained sensitive to muted Atlantic demand and cautious chartering, which limited a broader recovery in fixing activity. On the supply side, IOC emerged as the leading shipper at 0.69 mnt, followed by AMNS with 0.47 mnt and Guinea & Nimba Mines at 0.22 mnt.

The Netherlands was the leading destination, importing 0.44 mnt, highlighting continued European demand despite softer overall Atlantic market conditions. Looking ahead, investments in high-grade and DR-grade iron ore projects could support Canada’s medium-term export outlook, particularly into European markets.

Indian shipments recover on east coast loadings

India’s iron ore exports increased 32.3% w-o-w to 0.92 mnt, up from 0.70 mnt in the previous week. The rise was supported by higher loadings from east coast ports, aided by comfortable Supramax availability. Paradip accounted for 0.40 mnt, followed by Dhamra at 0.29 mnt, while Mangalore contributed 0.11 mnt, reflecting a broad-based improvement in port activity.

However, cautious chartering behaviour and limited demand visibility continued to cap fixing activity, keeping shipment momentum selective rather than aggressive. China remained the leading destination, importing 0.57 mnt of Indian iron ore during the week, underpinning export flows despite subdued regional demand conditions.

Chilean exports remain subdued despite modest rebound

Chile’s iron ore exports rose 11.2% w-o-w to 0.2 mnt, but volumes remained subdued amid limited cargo availability and selective Pacific fixing. All shipments originated from Huasco, which loaded 0.19 mnt during the week.

Despite the modest rebound, uneven vessel positioning and cautious chartering continued to limit export momentum, keeping Chilean shipments well below recent averages. Looking ahead, ongoing investment and expansion plans at key Chilean iron ore operations could support future export capacity and help Chile maintain its niche role in the Pacific basin.

Peruvian shipments ease on scheduling constraints

Peru’s iron ore exports declined 7.5% w-o-w to 0.4 mnt, reflecting scheduling constraints and reduced cargo nominations during the holiday period. Shipments were concentrated entirely at San Nicolas, which loaded 0.35 mnt, led by Shougang Hierro at 0.4 mnt.

China remained the major destination, importing the complete of Peruvian iron ore during the week. Despite generally workable mid-Pacific freight conditions, shipment flows remained uneven, constrained by cargo timing and selective fixing.

Weak freight market continues to cap iron ore shipment momentum

Dry bulk freight sentiment across key iron ore routes remained mixed but largely subdued during the week, reflecting holiday-related slowdown, uneven cargo demand, and ample vessel availability. Trading activity thinned across most segments as charterers stayed cautious and fixing remained selective amid year-end conditions.

Freight performance diverged across basins, with selective long-haul cargoes offering limited support on some Atlantic routes, while Pacific trades stayed under pressure amid thin fixing and improving tonnage lists. Overall market confidence remained restrained, with owners adjusting expectations in response to weak seasonal demand.

As a result, the broader freight backdrop continued to favour short-haul movements while constraining long-haul shipment economics, reinforcing uneven export performance across major iron ore origins during the week.

Outlook

Global iron ore shipments are expected to remain mixed in the near term, with volumes likely to stabilise rather than accelerate as markets transition out of the year-end holiday period. Australia is set to retain volume leadership supported by operational efficiency and short-haul advantages, while Brazil and other Atlantic suppliers remain sensitive to long-haul freight economics and price-disciplined chartering.

Smaller exporters may continue to experience week-to-week volatility driven by selective fixing, cargo timing, and freight availability. Unless freight sentiment improves materially and visibility on Chinese steel demand strengthens, a broad-based and sustained recovery in global iron ore exports is likely to remain uneven across regions.

Leave a Reply