- Australia shock hits flows; Brazil cushions the fall

- Resumption of operations to unlock deferred volumes

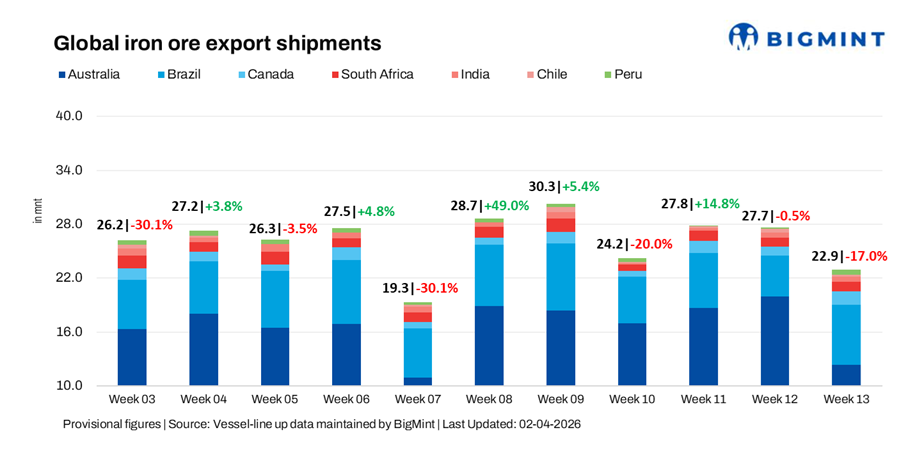

Global iron ore export shipments declined 17% w-o-w to 22.95 million tonnes (mnt) in the week ended 27 March, from 27.66 mnt a week earlier, according to BigMint data. A sharp drop in Australian shipments due to cyclone disruptions weighed on volumes, even as Brazil, Canada, and Peru saw recoveries, while South Africa and India remained stable and Chile witnessed weaker activity.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 8.2 mnt, Walcott 1.9 mnt, and Dampier 2.0 mnt. BHP exported 4.4 mnt, Rio Tinto 3.8 mnt, and FMG 3.2 mnt, with China absorbing 10.4 mnt.

- Brazil: Ponta da Madeira shipped 2.7 mnt, Tubarao 1.8 mnt, and Itaguai 1.1 mnt. Vale exported 3.2 mnt, while CSN shipped 2.8 mnt, with China importing 3.5 mnt.

- Canada: Port Cartier shipped 1.1 mnt and Sept-Iles 0.4 mnt, with AMNS exporting 1.1 mnt and Guinea & Nimba Mines 0.3 mnt.

- South Africa: Saldanha handled 0.9 mnt and Richards Bay 0.2 mnt, with the Netherlands receiving 0.2 mnt.

- India: Paradip shipped 0.2 mnt and Dhamra 0.2 mnt, with China importing 0.2 mnt.

- Chile: Guayacan shipped 0.2 mnt, with China importing 0.2 mnt.

- Peru: San Nicolas shipped 0.5 mnt, with Shougang Hierro exporting 0.5 mnt and China importing 0.4 mnt.

Bulk iron ore freights show mixed-to-soft trend

Dry bulk iron ore freight rates softened w-o-w amid limited enquiry and cautious fixing. The Pacific remained subdued on weak Australian cargo availability, while the Atlantic found some support from Brazil flows. Ample vessel supply and volatile bunker prices kept overall sentiment under pressure, despite firmness on select routes.

Outlook

Iron ore shipments are expected to recover in the near term as weather conditions stabilise and port operations resume in Australia, aiding clearance of backlog cargoes. However, ongoing maintenance and residual logistical constraints may keep flows uneven. Freight sentiment is likely to remain cautious amid vessel oversupply and bunker volatility, though improving cargo availability could offer limited support.

Leave a Reply