- Australia and Brazil remain key contributors despite softer weekly trends

- Smaller exporters experienced higher volatility due to selective fixing

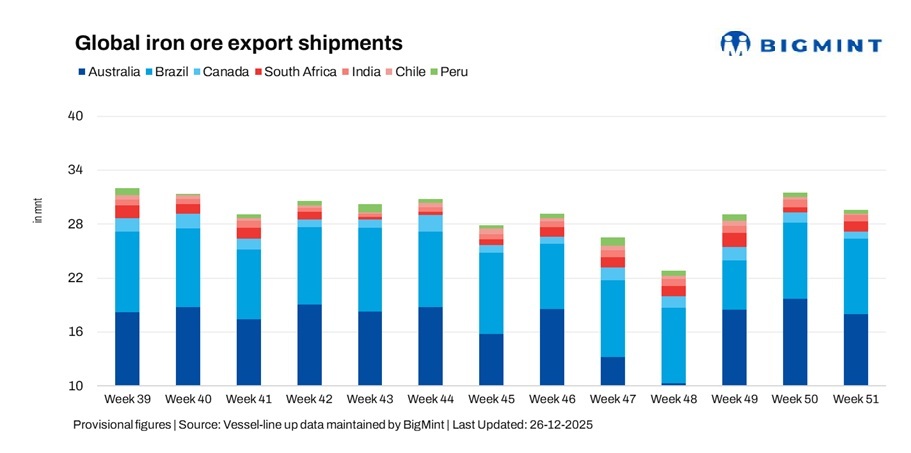

Global seaborne iron ore exports declined 6.5% w-o-w to 29.50 million tonnes (mnt) in the week ended 19 December, down from 31.56 mnt in the previous week, according to BigMint’s vessel line-up data. The moderation was primarily driven by lower shipments from Australia and India, which outweighed steady exports from Brazil and a sharp rebound in South African volumes.

The weekly decline came against the backdrop of a mixed but generally softer freight environment, as cautious chartering activity, ample vessel availability, and subdued demand visibility particularly from China limited fresh fixing. While freight weakness supported selective short-haul movements, it constrained long-haul shipment economics, contributing to uneven export performance across major iron ore origins.

Shipments from Canada, Chile, and Peru also fell w-o-w, reflecting reduced cargo availability, scheduling constraints, and selective fixing amid softer Atlantic and Pacific freight sentiment, which capped any broader recovery in global export volumes during the week.

Country-wise trends

Australian iron ore exports retreat after prior gains

Australia’s iron ore exports declined 8.5% w-o-w to 18 mnt in the week ended 19 December, down from 19.7 mnt previously. The drop followed two weeks of strong shipments and reflected a normalisation of loading schedules at Western Australian ports, alongside fewer fresh cargo nominations. Rio Tinto remained the largest shipper at 7.12 mnt, followed by BHP with 5.28 mnt and FMG at 3.76 mnt.

Port operations were steady, with Port Hedland loading 10.13 mnt, Walcott 3.91 mnt, and Dampier 3.21 mnt, though softer freight sentiment and cautious chartering capped volumes. China led imports at 15.36 mnt, while Japan and South Korea imported 0.96 mnt and 0.89 mnt, respectively.

Despite the weekly decline, Australia maintained its position as the world’s largest iron ore exporter, supported by its short-haul advantage into Asia. Australia’s iron ore outlook remains underpinned by operational reliability despite rising geopolitical and trade-related noise. While isolated trade tensions surfaced in 2025, shipment continuity and long-term supply contracts continue to support its dominance in global iron ore flows.

Brazilian iron ore shipments ease as cargo flows normalize

Brazilian iron ore exports edged down marginally by 1.3% w-o-w to 8.4 mnt, compared with 8.5 mnt in the previous week. The slight decline followed last week’s sharp rebound and pointed to a normalisation in cargo flows rather than a loss of export momentum.

Vale remained the leading shipper at 4.11 mnt, followed by CSN with 3.32 mnt. Loadings were well spread across key ports, with Ponta da Madeira handling 3.18 mnt, Itaguai 1.67 mnt, and Tubarao 1.64 mnt, supported by stable operations and workable vessel positioning.

China continued to dominate demand, importing 2.72 mnt of Brazilian iron ore. However, resistance to firmer long-haul freight levels limited further upside, keeping shipment volumes broadly stable but measured. On the regulatory front, a Brazilian court has temporarily suspended Samarco’s mining expansion in Minas Gerais over environmental concerns, although the company said it has not been formally notified and that current operations continue as usual.

South Africa rebounds sharply from a low base

South Africa’s iron ore exports surged 91.2% w-o-w to 1.1 mnt in the latest week, rebounding sharply from 0.6 mnt in the previous week. All shipments originated from Saldanha Bay, reflecting the release of deferred cargoes after subdued activity in the prior week.

The recovery was supported by improved scheduling and selective fixing. However, weak long-haul freight sentiment and cautious chartering behaviour continued to restrain more aggressive export growth, keeping volumes below recent monthly averages despite the sharp weekly rebound.

China remained the leading destination, importing 0.47 mnt of South African iron ore during the week.

Canada exports decline further on subdued Atlantic demand

Canada’s iron ore exports declined sharply by 34.3% w-o-w to 0.8 mnt, down from 1.15 mnt in the previous week, as reduced cargo nominations and muted spot demand weighed on shipments. Exports were split between Sept-Iles at 0.46 mnt and Port Cartier at 0.29 mnt.

Key shippers included Guinea & Nimba Mines at 0.36 mnt, followed by Arcelor Mittal with 0.29 mnt and IOC at 0.10 mnt. Despite stable port operations, softer Atlantic freight sentiment and limited buying interest from major destinations curtailed fixing activity.

As a result, weekly export volumes continued to pull back, reflecting cautious market conditions across the Atlantic basin. Looking ahead, Canada’s iron ore sector is positioning for cleaner steel demand, with Champion Iron acquiring Norway’s Rana Gruber to expand access to high-grade, low-carbon ore in Europe, while Sojitz, Champion and Nippon Steel are advancing the Kami Project to develop DR-grade iron ore for low-emission steelmaking.

Indian shipments fall on weaker regional demand

India’s iron ore exports fell 17.5% w-o-w to 0.7 mnt, down from 0.84 mnt in the previous week. The decline was driven by lower loadings from Paradip at 0.28 mnt and Dhamra at 0.17 mnt, reflecting softer regional demand and fewer spot cargoes.

China remained the leading destination, importing 0.28 mnt of Indian iron ore during the week. Despite comfortable Supramax vessel availability, cautious chartering and weaker freight sentiment constrained fixing activity.

As a result, shipment momentum eased, marking a notable weekly correction following recent gains.

Chilean exports slide amid limited cargo availability

Chile’s iron ore exports dropped sharply by 46.9% w-o-w to 0.2 mnt, reversing part of the recovery seen in the previous week. All shipments were concentrated at Totoralillo at 0.17 mnt, as reduced cargo availability and subdued Pacific fixing interest weighed on volumes.

China remained the sole destination, importing 0.17 mnt. However, uneven vessel positioning and cautious chartering continued to limit export momentum, keeping shipments subdued.

Peruvian shipments soften on scheduling constraints

Peru’s iron ore exports fell 22.4% w-o-w to 0.38 mnt, down from 0.49 mnt in the previous week. Shipments were concentrated at San Nicolas with 0.34 mnt and Matarani at 0.04 mnt, led by Shougang Hierro at 0.34 mnt.

China remained the primary destination, importing 0.34 mnt of Peruvian iron ore. Reduced cargo nominations and timing-related constraints weighed on loading activity.

As a result, shipments failed to achieve a steadier flow despite generally workable mid-Pacific freight conditions.

Weak freight market weighs on iron ore shipment momentum

Dry bulk freight sentiment across key iron ore routes remained mixed but largely subdued during the week, reflecting uneven cargo demand, ample vessel availability, and cautious chartering as the year-end approaches. Trading activity slowed across most segments, with weaker Chinese steel demand limiting fresh enquiries and keeping pressure on rates.

Supramax markets softened amid slower iron ore and minor bulk demand from the Indian east coast, while Capesize sentiment stayed cautious as steady but unaggressive Pacific loadings met improving tonnage availability. Atlantic routes saw selective support from long-haul cargoes, though gains were capped by price-sensitive chartering.

Operational frictions, including port-related delays in China, disrupted vessel turnaround times in some areas. Overall, the softer freight backdrop supported selective short-haul movements but constrained long-haul shipment economics, reinforcing uneven export performance across major iron ore origins.

Outlook

Global iron ore exports are expected to remain mixed and largely unchanged through the remainder of December. Australia is likely to retain volume leadership, supported by operational efficiency and short-haul advantages, while Brazil’s shipments remain sensitive to long-haul freight economics.

Smaller exporters may continue to see week-to-week volatility due to selective fixing and cautious demand. Unless freight sentiment stabilises and visibility on Chinese demand improves, a sustained rebound in global iron ore exports appears limited, with shipment momentum likely to remain uneven across regions.

Leave a Reply