- Brazilian exports slump nearly 30% amid limited port activity

- Freight market turns mixed on elevated tonnage supply, softer sentiment

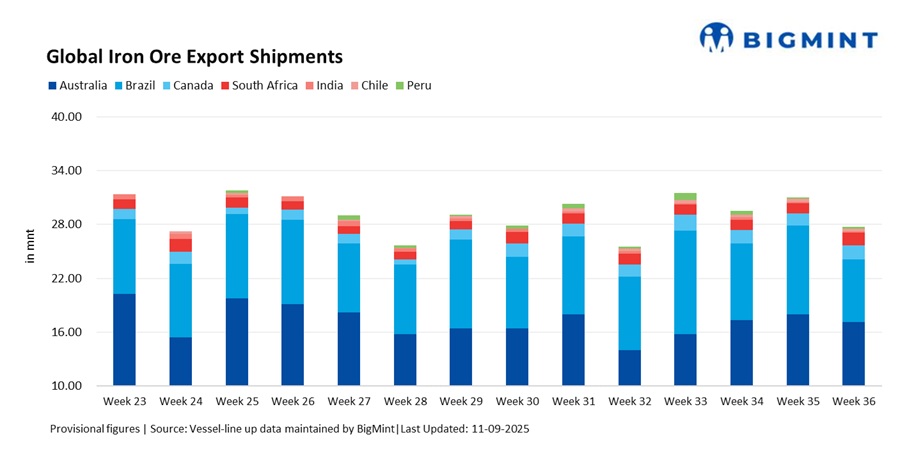

Global iron ore exports declined by 10.5% w-o-w to 27.76 million tonnes (mnt) in week 36 (30 August-5 September 2025), down from 31.02 mnt in week 35. The fall was led by weaker shipments from Brazil and Australia, which overshadowed incremental gains from Canada, South Africa, and Peru.

Market participants noted that Brazilian loadings slowed significantly at key terminals, while Australian shipments also pulled back after a strong run through August. The overall decline coincided with subdued Chinese buying interest, with mills exercising caution as steel margins stayed compressed.

In contrast, Canada and South Africa posted a rebound, supported by steadier port activity and operational catch-up. However, the gains were insufficient to offset declines from the larger producers.

On the freight side, market conditions turned mixed, with the Pacific basin weighed down by elevated tonnage supply and weak fixture activity, while select Atlantic routes showed firmer sentiment.

Country-wise exports

Australia’s iron ore exports slipped 4.6% w-o-w to 17.14 mnt in Week 36 from 17.96 mnt in Week 35, as shipments from Pilbara ports eased after a strong showing in the previous week.

Port Hedland handled around 11 mnt, Dampier Port shipped 2.6 mnt, and Cape Lambert (Walcott) managed close to 3.3 mnt. Among the key miners, Rio Tinto exported 5.9 mnt, BHP shipped 5.1 mnt, and FMG dispatched 4.1 mnt.

On the demand side, China remained the dominant buyer with 13.9 mnt, followed by Japan at 1.6 mnt and South Korea at 1.2 mnt, highlighting Asia’s continued reliance on Australian flows despite softer overall momentum.

Brazilian exports recorded the steepest decline, falling 29.3% w-o-w to 6.99 mnt in week 36 from 9.89 mnt in week 35. Loadings were led by Ponta da Madeira (3 mnt), followed by Itaguai (1.8 mnt) and Tubarao (1.1 mnt), with minor ports contributing the balance. Vale remained the largest shipper at around 3.5 mnt, with China absorbing an equivalent 3.5 mnt as the top buyer.

Adding to market developments, Vale restarted its Capanema mine in Minas Gerais on 4 September, resuming operations after a 22-year shutdown and five years of renovation. The restart is expected to contribute around 15 mnt/year of additional capacity to Vale’s output profile.

The sharp fall followed Week 35’s catch-up surge, as Week 36 saw fewer fixtures, weak Chinese demand, and ample Atlantic tonnage, all of which curbed Brazilian shipments.

Canada’s iron ore exports recovered by 12.3% w-o-w to 1.55 mnt in week 36 from 1.38 mnt in week 35, supported by steadier port activity after recent weather-related disruptions.

Sept Iles contributed the bulk at 0.9 mnt, followed by Milne Inlet at 0.4 mnt and Port Cartier at 0.3 mnt. Among shippers, Guinea & Nimba Mines led with around 0.5 mnt.

On the demand side, European buyers remained the key outlet, with The Netherlands taking 0.3 mnt and France 0.2 mnt, underlining Canada’s continued role as a stable supplier of high-grade concentrates to European steelmakers. The week’s rebound reflected a partial operational catch-up, though seasonal weather constraints and navigation challenges still pose risks to sustained momentum.

South Africa’s iron ore exports rose sharply by 26% w-o-w to 1.43 mnt in week 36 from 1.14 mnt in week 35, as stronger activity was recorded at key ports. Saldanha Bay handled the majority at 1.2 mnt, while Richards Bay contributed around 0.3 mnt.

On the demand side, Japan emerged as the largest importer with 0.3 mnt, followed by China at 0.2 mnt, alongside smaller parcels directed to Europe. The recovery reflected improved port performance and firmer demand from Asian buyers, although persistent rail and infrastructure bottlenecks, along with elevated freight costs on the South Africa-China route, continue to limit the country’s ability to scale up exports sustainably.

India’s iron ore exports declined 28.7% w-o-w to 0.12 mnt in week 36 from 0.16 mnt in week 35, as heavy monsoon rains continued to disrupt mining activity and inland transportation, pushing shipments to a multi-year seasonal low and due to higher cost of freight charges and taxes.

Export prices held largely steady, with seaborne trading activity remaining thin and only a handful of deals concluded amid wide bid-offer gaps. However, sentiment has started to firm, as traders are rushing to offload and export cargoes ahead of a potential 30% export duty on low-grade iron ore, expected to take effect from early October, according to a Mumbai-based shipbroker.

Chile’s iron ore exports dipped 10.8% w-o-w to 0.28 mnt in week 36 from 0.32 mnt in week 35, as shipments eased slightly across its limited export hubs. Totoralillo accounted for around 0.2 mnt, while Guayacan handled close to 0.1 mnt.

On the demand side, China absorbed nearly 0.3 mnt, underscoring its continued reliance on Chile’s niche supply. While Chile plays a modest role in the global market, infrastructure limitations and small-scale production keep its export volumes capped, leaving little room for expansion.

Peru’s iron ore exports rose sharply by 42.7% w-o-w to 0.25 mnt in week 36 from 0.17 mnt in week 35, as shipments recovered modestly at key ports. San Nicolas led with around 0.2 mnt, while Matarani contributed close to 0.1 mnt.

On the demand side, China absorbed about 0.2 mnt, highlighting its role as the primary destination for Peruvian cargoes. Despite the week’s rebound, Peru’s exports remain highly volatile given their dependence on a limited number of ports and smaller-scale operations, which leave volumes vulnerable to operational or logistical disruptions.

Dry bulk iron ore freights showed mixed trends in week 36. While Australia-China and Brazil-China Capesize routes eased, India-China and South Africa-China freights edged higher, reflecting varied regional dynamics.

Elevated tonnage supply weighed on Pacific market sentiment, with limited fresh cargoes keeping Supramax and Capesize activity subdued. Atlantic basin trading remained tepid, while charterers in Asia exercised caution amid weaker FFA rates and soft spot demand. Overall, freight sentiment was fragile, with market participants pointing to uncertain direction in the near term.

Outlook

Global iron ore exports are likely to remain range-bound in the near term. Australian flows are expected to stay relatively steady, while Brazil’s shipments may remain volatile given freight sensitivities and uneven demand from Chinese mills.

Seasonal disruptions in India and logistical challenges in South Africa could continue to cap upside. On the freight side, elevated vessel supply and weak derivatives are expected to keep sentiment cautious, though occasional fixtures may lend temporary support.

Leave a Reply