- Post-holiday cargo normalisation drags weekly volumes lower

- Seasonal freight weakness and cautious fixing keep shipments under pressure

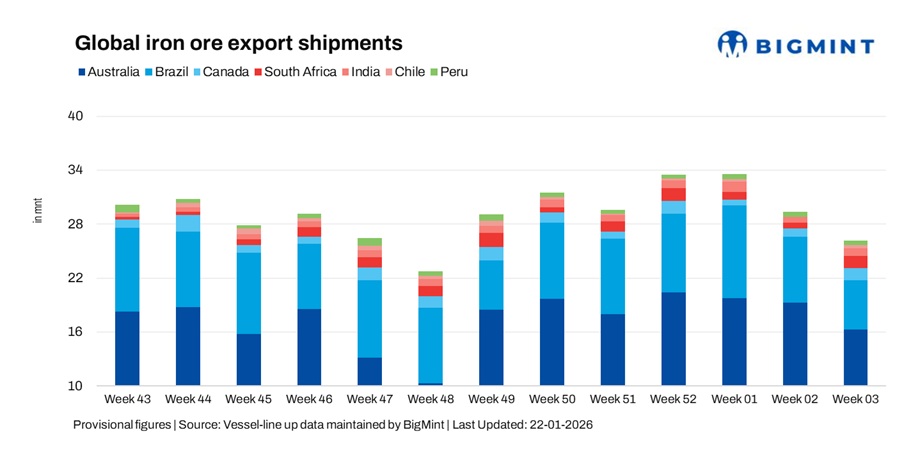

Global seaborne iron ore exports fell 11.1% w-o-w to 26.2 million tonnes (mnt) in the week ended 16 January 2026, down from 29.5 mnt in week 02 (03-09 January), as per BigMint’s vessel line-up data. The decline extended the post-holiday slowdown, with weak freight sentiment and cautious chartering continuing to limit shipment momentum.

The fall was mainly driven by sharp drops in exports from Australia and Brazil, which more than offset increases from South Africa, Canada, India, and Chile. With long-haul freight economics still unattractive and cargo urgency low, exporters preferred to slow shipments rather than fix vessels at weak rates.

Seasonal softness ahead of the Lunar New Year, thin fixing activity, and ample vessel availability reduced charterers’ appetite for fresh long-haul cargoes, keeping global shipments under pressure during the week under review.

Country-wise trends

Australia shipments drop on weak cargo stems

Australia’s iron ore exports fell 15.7% w-o-w to 16.26 mnt due to fewer fresh cargo stems, as miners followed disciplined shipping schedules amid weak Capesize sentiment and limited buying interest from China. The impact of late-December cargo clearances faded, and exporters delayed shipments rather than fix vessels at unattractive freight levels. Despite the fall, Australia remained the largest supplier, supported by stable port operations and its short-haul advantage into Asia.

Port-wise loadings were led by Port Hedland at 9.84 mnt, followed by Walcott at 2.94 mnt and Dampier at 2.75 mnt, showing steady operations across major Western Australian terminals despite the softer weekly outcome. The distribution highlighted disciplined shipment planning rather than operational disruptions. On the shipper side, Rio Tinto led exports with 5.69 mnt, followed by BHP at 4.51 mnt and FMG at 4.03 mnt.

China remained the main destination at 13.07 mnt, while South Korea and Taiwan imported 1.43 mnt and 0.59 mnt, respectively. Additionally, major miners continued strong production, with BHP reporting record first-half output and Rio Tinto achieving record quarterly production in the Pilbara. However, softer Chinese demand, port stockpiling, and lower prices on some contracts are creating uncertainty, which could weigh on export timing and freight activity in the near term.

Brazil exports fall further on weak long-haul economics

Brazil’s iron ore shipments dropped 24.1% w-o-w to 5.55 mnt, extending the previous week’s decline. The fall was driven by weak long-haul freight economics, low fixing interest, and the absence of deferred cargoes that had supported earlier volumes. Exporters stayed cautious, as soft Atlantic freight markets and price-sensitive buyers limited fresh cargo nominations. Meanwhile, Brazil’s wider export performance remains robust, with 2025 seeing record iron ore shipments exceeding 416 million tonnes, even as prices weakened.

Port-wise loadings were led by Ponta da Madeira at 2.92 mnt, followed by Itaguai at 1.25 mnt and Tubarao at 0.81 mnt, showing a broad-based slowdown across Brazil’s main export terminals. The softer port activity reflected reduced cargo stems rather than any major operational disruptions.

On the shipper side, Vale led exports with 2.92 mnt, while CSN shipped 2.06 mnt, reflecting lower cargo nominations after earlier releases. China remained the main destination at 1.97 mnt, while India imported 0.35 mnt. However, lower export values and cautious buying behaviour among steel mills are shaping trading patterns, which may influence near-term export timing and freight demand despite Brazil’s strong underlying supply position.

Canada exports rebound on selective demand

Canada’s iron ore exports rose 35.5% w-o-w to 1.28 mnt, supported by improved cargo readiness and selective European demand. The rebound reflected smoother post-holiday scheduling and the return of some delayed cargoes into the market.

Port-wise loadings were led by Sept-Iles at 0.71 mnt, followed by Port Cartier at 0.57 mnt, showing steady operations across Canada’s key Atlantic export terminals. The increase was driven more by better cargo timing than by any major change in underlying demand. On the shipper side, AMNS India led exports with 0.57 mnt, followed by IOC at 0.36 mnt and Guinea & Nimba Mines at 0.35 mnt. China received 0.18 mnt, while the rest of the volumes moved into other Atlantic and European markets.

Meanwhile, Champion Iron’s move to expand its high-grade iron ore portfolio and discussions around Port of Churchill expansion highlight Canada’s efforts to strengthen its export position, which could support future freight demand despite weak Atlantic market conditions.

South Africa shipments jump on better timing

South Africa’s iron ore exports surged 96.2% w-o-w to 1.41 mnt, rebounding from a weak previous week. The increase was mainly due to better cargo timing and improved cargo availability rather than any major improvement in freight sentiment.

Saldanha Bay remained the sole and main loading port, handling the entire 1.41 mnt, reflecting the concentration of export flows through a single terminal. The rebound was driven by shipment timing rather than stronger demand. On the destination side, China imported 0.48 mnt, while the rest of the volumes moved into other Asian and Atlantic markets.

Despite the weekly jump, export flows remained volatile and highly sensitive to freight economics and buyer caution. Meanwhile, South Africa’s wider iron ore sector has faced some near-term pressures, with mining output slipping late in 2025, while long-term initiatives such as potential green trade routes via Saldanha Bay and improved rail logistics are expected to support future exports and freight demand.

India exports recover modestly

India’s iron ore exports rose 21% w-o-w to 0.77 mnt, supported by better east coast loadings as Supramax demand stabilised and post-holiday chartering activity gradually picked up. The rebound followed a sharp decline in the previous week. Paradip remained the main loading port, handling 0.49 mnt, reflecting improved shipment activity from the east coast.

The recovery was driven more by better cargo timing than by any strong improvement in underlying demand. On the shipper side, Rungta Mines led exports with 0.23 mnt, followed by AMNS India at 0.15 mnt. China remained the main destination, importing 0.41 mnt, underlining India’s continued role as a short-haul supplier to Asian markets despite cautious buying interest and strong domestic demand.

Meanwhile, domestic high-grade supply has been tightening and iron ore imports have risen to multi-year highs as mills seek offshore cargoes. At the same time, the government’s move to delay export duty increases on low-grade ore has eased cost pressures but left policy uncertainty, which could influence near-term export timing and freight activity.

Chile resumes shipments

Chile exported 0.4 mnt in week 03 after no shipments in the previous week. The return reflected the clearance of delayed cargoes and improved vessel positioning rather than stronger demand. Port-wise loadings were led by Totoralillo at 0.20 mnt, followed by Huasco at 0.17 mnt and Mejillones at 0.03 mnt, showing that shipments were spread across multiple terminals despite the low overall volume.

On the destination side, China imported 0.20 mnt, while the remaining volumes moved into other markets. Exports remained irregular and closely linked to cargo readiness and freight timing rather than stable demand.

Meanwhile, Chile’s broader mining sector has been in focus, with industry leaders warning that recent changes in government mining leadership and regulatory priorities could influence investment and export planning. At the same time, new shipment activity from smaller iron ore producers at ports like Puerto Las Losas highlights efforts to broaden export capacity, even as iron ore remains a small part of Chile’s overall mineral export mix compared with copper and lithium.

Peru exports ease slightly

Peru’s iron ore exports fell 7.4% w-o-w to 0.52 mnt, as shipments remained tied to selective fixing and cautious chartering. The decline reflected weaker cargo timing rather than any major change in underlying supply. Port-wise loadings were led by San Nicolas at 0.47 mnt, followed by Matarani at 0.05 mnt, showing that shipments remained heavily concentrated at a single terminal. Stable port operations helped keep volumes steady despite weak freight sentiment.

On the shipper side, Shougang Hierro accounted for 0.47 mnt, while Chile contributed 0.05 mnt. China remained the main destination at 0.33 mnt, followed by Japan at 0.15 mnt, underlining Peru’s continued dependence on Asian demand despite cautious chartering.

Meanwhile, Peru’s Central Bank expects modest economic growth in 2026-27, which could support mining activity and help stabilise future iron ore exports and freight demand.

Freight weakness keeps shipments under pressure

Iron ore freight sentiment stayed weak during week 03 due to seasonal softness ahead of the Lunar New Year, cautious chartering behaviour, and ample vessel availability. Softer Capesize demand and mixed macro signals continued to weigh on overall freight market confidence.

Weaker steel margins in China reduced cargo urgency, while slower cargo releases limited fresh spot enquiries. As a result, fixing activity remained thin and charterers stayed largely on the sidelines.

At the same time, more vessels moved into key loading areas, shifting bargaining power toward charterers and leading to lower fixture levels. This discouraged exporters — especially long-haul Atlantic suppliers — from committing additional cargoes, deepening the post-holiday slowdown in global shipments.

Outlook

Global iron ore shipments are expected to remain soft in the near term as freight markets stay weak and chartering sentiment remains cautious ahead of the Lunar New Year. Seasonal demand slowdown, thin fixing activity, and ample vessel availability are likely to keep long-haul freight economics unattractive, limiting fresh cargo commitments.

Australia and Brazil may stabilise once deferred cargoes return and post-holiday schedules normalise, but any recovery is expected to be gradual. Until Chinese steel demand improves and freight markets tighten, global iron ore exports are likely to stay rangebound through late January and early February.

Leave a Reply