Horizon Insights – As iron ore shipments continue to remain high, expectations of a surplus within the year continue to strengthen.

Two unexpected points to be noted: One, the resumption of shipments from Ukraine, and two, weakness in the ability to divert iron ore supply overseas. Crude steel production in the second quarter was significantly weaker than usual, and the increase in overseas iron ore demand failed to cover the decline in domestic iron ore production.

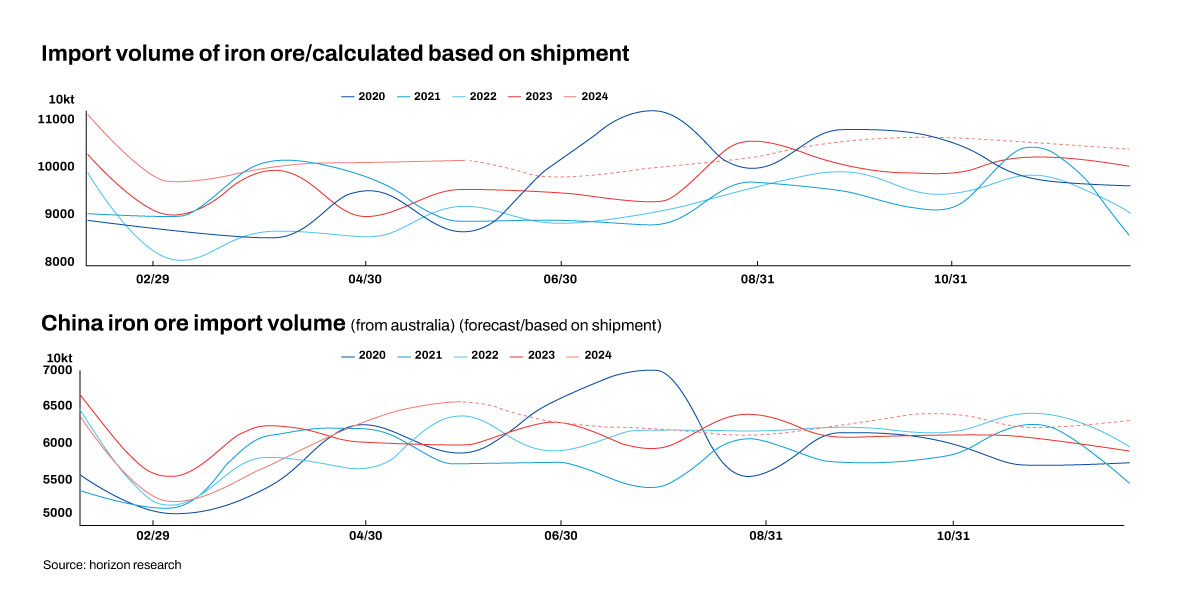

If the current shipping trend is maintained in the second half of the year, the increase in imports of iron ore to China for the whole year of 2024 may reach 70 million tonnes (mnt), with Australia becoming the main source of the additional supplies in the second half of the year.

As for hot metal output, current policy proposals can provide support for further production increase, but due to financial constraints, construction materials may face a slight reduction in production.

From a medium-to-long term perspective, especially as China enters the peak season in August, the actual demand will increase. And, the question, whether steel mills need to reduce/increase production needs to be evaluated. It is still difficult to see greater room for increasing production of hot metal. This will result in the iron ore price range being firmly suppressed.

In the short term, the market does not have high requirements for steel hence there is not much inventory depletion. There are two meetings in July (the Third Plenum and the Politburo meeting), and the signals released during the meeting will still impact market sentiments. Therefore, it is expected that in July, prices will show a weak and volatile pattern, and a certain downward movement.

In June, mainstream iron ore shipments surged, followed by a seasonal decline in July. It is observed that shipments from Brazil continued to rise compared to the same period in the past years.

This has led to higher share of shipments to China

The Australia-to-China iron ore ratio in 2024 Q2 has significantly increased compared to Q2 of 2023. Although the share of shipments from Brazil to China is still at a seasonally high level. The suppliers’ ability to divert iron ore overseas this year is weaker than expected.

In H12024, with China’s crude steel production at -1.4% and pig iron production at -3.6%, the overseas crude steel production failed to offset China’s domestic reduction. The reasons were two-fold: One, geopolitical issues (Iran’s DRI production sharply decreased in March and April), two, overseas demand was subdued.

China’s domestic mining production has declined due to safety issues

Recently, coinciding with the safety inspection month in Hebei, the province has strengthened its safety norms for mining enterprises. The resultant impact on local mining production is 0.5 to 0.8 mnt per month. Domestic mining production is expected to continue to decline.

Hot metal output is expected to remain stable in July

In the short term, considering the low market demand, there has been only marginal changes in inventory levels during the off-season, which will not help to increase crude steel output.

Construction sector yet to show signs of improvement

The temporary increase in housing transactions in mid to late June has indeed boosted market sentiments, but recent indications are that the improvement was mostly seasonal and had poor sustainability. At present, real estate steel demand is still negative, and the infrastructure sector is constrained by local government fiscal measures.

Note: This article has been written in accordance with an article exchange agreement between Horizon insights and BigMint.

Leave a Reply