- Indian iron ore exports ditch global softness, rises 24%

- Slower Chinese fundamentals resist supply push

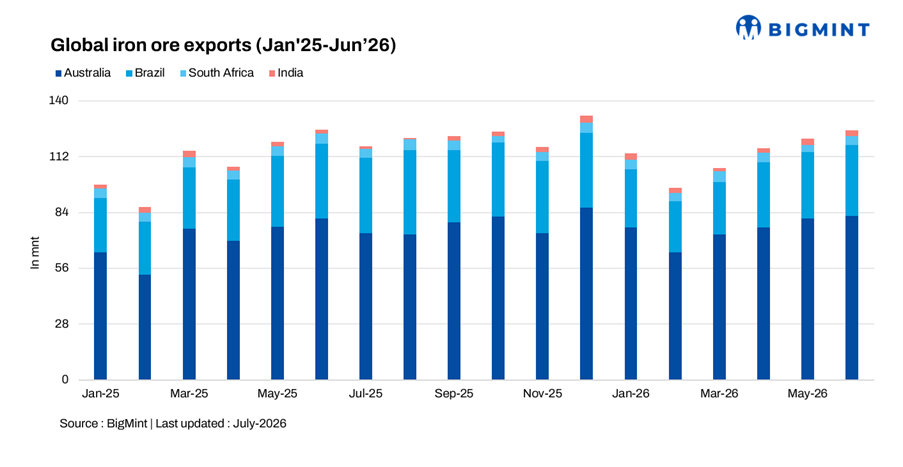

Global iron ore and pellet trade showed mixed trends in H1 CY26, supported by stable shipment activity from major exporting countries and continued buying from Asian markets, particularly China. However, the overall market also faced multiple challenges during the period, including elevated crude oil prices amid the US-Iran conflict, which increased freight costs and impacted global trade flows. At the same time, rising mine supply from major exporters and expectations of additional volumes following the commencement of first ore production from the Simandou iron ore project significantly increased seaborne cargo availability, continuing to exert pressure on international iron ore prices despite intermittent improvement in Chinese demand.

Australian shipments rise 8% y-o-y

Australia’s iron ore exports stood at 451.7 million tonnes (mnt) in H1 CY26, up 7.8% from 419 mnt in H1 CY25. Pellet exports also increased by 10% y-o-y to 1.1 mnt from 1.0 mnt last year. Moreover, Australia exported 82.0 mnt of iron ore and 0.2 mnt of pellets in Jun’26, compared with 80.7 mnt of iron ore and 0.2 mnt of pellets in May’26.

China remained the largest importer of Australian iron ore and pellets at 375.1 mnt, followed by Japan at 28.5 mnt. Among exporters, Rio Tinto led shipments with 156.1 mnt, followed by BHP at 145.9 mnt and Fortescue Metals Group at 105.9 mnt during H1 CY26.

Australian exports remained high on account of greater dispatches particularly to China in order to offset their domestic subdued iron ore production; with ROM production plunging down to 397 mnt in 5M CY26 against 412 mnt in the same period last year.

Moreover, China maintained higher portside inventories ended Jun’26 at 159 mnt (across 34 major ports) which further supported higher shipments at a scenario where the Chinese crude steel production dipped by 4.5% to 434.8 mnt in H1 CY26 against H1 CY25. Additionally, higher exports were aided by stronger shipment activity from major miners, stable mining and rail operations across Pilbara leading to steady procurement during the first half of the year.

Brazilian supply edges down 4% y-o-y

Brazil’s iron ore exports stood at 181.82 mnt in H1 CY26, down 3.8% from 188.95 mnt in H1 CY25. Brazil exported 35.75 mnt of iron ore in Jun’26 against 32.29 mnt in May’26, recording a 10.7% m-o-m increase.

China (126.75 mnt) remained the largest importer of Brazilian iron ore during the period, followed by Malaysia (8.42 mnt) and Japan (5.51 mnt). Demand for Brazilian medium- and high-grade fines stayed relatively healthy, supported by blending requirements and productivity optimisation at steel mills.

South African export cuts by 6% y-o-y

South Africa’s iron ore exports stood at 26.93 mnt in H1 CY26, down 5.5% from 28.49 mnt in H1 CY25. China remained the largest importer of South African iron ore at 13.43 mnt, followed by the Netherlands at 3.56 mnt. South Africa exported 4.37 mnt of iron ore in Jun’26 against 3.42 mnt in May’26.

Export volumes remained under pressure due to continued rail and logistics inefficiencies, along with intermittent disruptions in cargo evacuation to export terminals. In addition, strong availability of Australian and Brazilian cargoes in the seaborne market continued to impact the competitiveness of South African material.

India’s export rises 24% in H1

India’s iron ore exports stood at 13.28 mnt in H1 CY26, rising 23.9% from 10.72 mnt in H1 CY25. In contrast, pellet exports declined by 32.8% y-o-y to 2.17 mnt from 3.23 mnt in the same period last year.

India exported 2.46 mnt of iron ore and 0.32 mnt of pellets in Jun’26 against 2.55 mnt of iron ore and 0.48 mnt of pellets in May’26. Iron ore exports declined by 3.5% m-o-m, while pellet shipments fell sharply by 33.3% m-o-m.

Higher iron ore exports were supported by weaker Indian Rupee against dollar; fetching better realisations. On the other hand, stronger cargo movement from east coast ports, improved exporter participation, and sustained Chinese demand kept momentum high. However, pellet exports declined amid softer overseas pellet demand and increased preference for direct iron ore cargoes in the seaborne market.

Outlook

Global iron ore and pellet trade is expected to remain relatively stable in the near term, supported by steady supply from major exporters and continued procurement from Asian buyers. However, the sharp rise in seaborne iron ore availability, along with expectations of additional supply from the Simandou iron ore project, is likely to keep pressure on global iron ore prices going forward.

Leave a Reply