- Softer Brazilian and South African shipments weigh on global volumes

- Capesize slump keeps iron ore freight sentiment under pressure

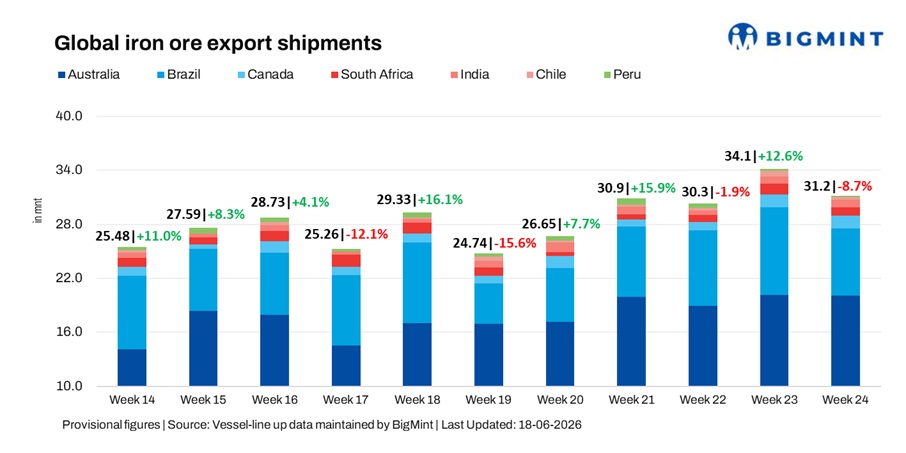

Global iron ore export shipments eased 8.7% w-o-w to 31.2 million tonnes (mnt) in the week ended 12 June, compared with 34.1 mnt a week earlier, according to BigMint data. The decline reflected softer shipments across several major exporting regions, with Brazil and South Africa leading the pullback, while Australia remained broadly stable and gains from Canada and India provided limited support.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 12.5 mnt, Port Walcott 3.8 mnt, and Dampier 3.4 mnt. Rio Tinto exported 7.2 mnt, BHP shipped 6.6 mnt, and FMG 4.5 mnt. China remained the largest importer at 16.5 mnt, followed by Japan (1.8 mnt).

- Brazil: Ponta da Madeira handled 3.1 mnt, Itaguai 1.7 mnt, and Tubarao 1.7 mnt. CSN exported 6.6 mnt, while Vale shipped 0.5 mnt. China imported 4.3 mnt.

- Canada: Sept-Iles handled 1.3 mnt. Guinea & Nimba Mines exported 1.0 mnt, with China importing 0.2 mnt.

- South Africa: Saldanha handled 0.8 mnt, while Richards Bay processed 0.1 mnt. China remained the largest importer at 0.3 mnt, followed by the Netherlands (0.2 mnt).

- India: Paradip handled 0.6 mnt and Dhamra 0.2 mnt. China imported 0.3 mnt.

- Chile: Totoralillo handled 0.2 mnt. China imported 0.2 mnt.

- Peru: San Nicolas handled 0.2 mnt. Shougang Hierro exported 0.2 mnt, with China importing 0.2 mnt.

Capesize weakness deepens as iron ore demand softens

Dry bulk iron ore freight markets weakened during the week, with the Capesize segment remaining under pressure amid subdued Chinese buying interest, limited cargo enquiries and weaker fixture activity. Softer trade flows pushed key Australia-China freight rates to a two-month low, while the Baltic Dry Index also declined.

Meanwhile, Supramax and Handysize markets remained relatively resilient on steady minor bulk demand, while Panamax showed signs of stabilisation. Lower bunker prices offered some cost support but failed to improve overall freight sentiment.

Outlook

Global iron ore shipments are expected to remain influenced by loading programmes across major exporting regions, with maintenance schedules, seasonal weather conditions and Chinese steel demand likely to shape near-term trade flows. Freight sentiment may stay under pressure if Capesize demand remains subdued, although monsoon-related loading precautions could lend support to freight rates in the coming weeks.

Leave a Reply