- Canada, South Africa, India see export volumes rise

- Freight dynamics support recovery in Atlantic basin flows

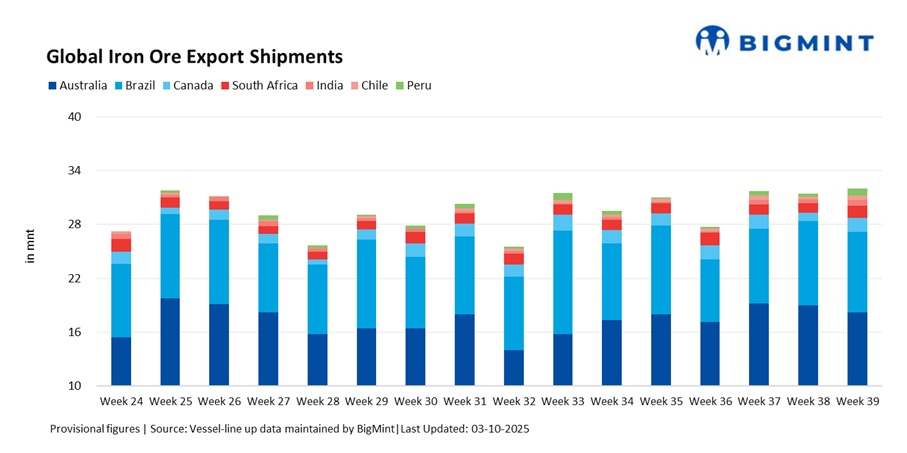

Global iron ore exports recovered modestly in week 39 (20-26 September 2025), rising 1.7% w-o-w to 32.07 million tonnes (mnt) from 31.52 mnt in week 38. The rebound was driven by strong gains from Canada, South Africa, India, Chile, and Peru, which outweighed declines from the two largest exporters, Australia and Brazil.

Market sources highlighted that improved freight availability in the Atlantic and opportunistic scheduling by smaller exporters were key in lifting volumes, even as the Pacific market softened. Overall, the week reflected a rebalancing between major and minor suppliers, with smaller origins driving global gains while the top two exporters eased back.

Country-wise trends

Australia’s iron ore exports dropped 4.3% week-on-week to 18.20 mnt in week 39 from 19.02 mnt in week 38, led by Port Hedland, where shipments eased to 11.01 mnt amid routine maintenance and weaker restocking demand from Chinese mills. In contrast, Walcott and Dampier maintained steady flows at 3.83 mnt and 2.93 mnt, supported by smoother operations, but these gains could not offset the slowdown at Hedland. Miner-wise, Rio Tinto shipped 6.76 mnt, BHP 5.76 mnt, and FMG 4.24 mnt.

On the demand side, Chinese imports of 15.15 mnt highlighted cautious procurement and subdued margins, tempering appetite for fresh cargoes. Market participants noted that while Australia’s export fundamentals remain solid, weekly volumes are now more vulnerable to maintenance schedules and shifts in Chinese buying sentiment, a trend reinforced by BHP’s ongoing pricing dispute with China, which adds uncertainty to shipments and buyer confidence.

Brazil’s iron ore exports slipped 4% w-o-w to 8.98 mnt in week 39 from 9.36 mnt in week 38. Loadings at major terminals such as Ponta da Madeira (3.67 mnt), Itaguai (2.33 mnt), and Tubarao (1.75 mnt) stayed steady, but weaker fixture activity in the Atlantic basin pulled overall volumes lower.

Vale led shipments with 4.08 mnt, though efforts to raise output were capped by limited fresh demand and tighter vessel availability. While Brazil’s long-haul voyages typically support freight by tying up tonnage, muted Chinese buying at 3.23 mnt and cautious chartering sentiment kept flows restricted. As a result, Brazil’s exports remained vulnerable to freight-related constraints despite broadly steady underlying demand.

Canada’s exports rebounded sharply in week 39, rising 65% w-o-w to 1.51 mnt from 0.91 mnt in week 38. Improved weather conditions and better scheduling allowed key terminals to clear previously delayed shipments, reversing the disruptions seen in the prior week. Milne Inlet handled 0.53 mnt, while Port Cartier and Sept-Iles each processed 0.49 mnt.

European buyers accounted for the bulk of the volumes, with The Netherlands emerging as the largest importer at 0.46 mnt. In contrast, interest from Asian markets remained limited, keeping overall demand regionally skewed despite the strong export recovery.

South Africa’s exports rose 23% w-o-w, reaching 1.39 mnt in week 39 from 1.13 mnt in week 38. The increase was largely driven by shipments from Saldanha Bay, which handled 1.22 mnt, supported by improved freight availability in the Atlantic.

The Netherlands emerged as the largest importer at 0.18 mnt, while Vietnam and South Korea took 0.17 mnt each. However, market sources noted that persistent rail and port bottlenecks continue to constrain export potential despite steady demand from China.

India’s shipments rose 31% w-o-w to 0.59 mnt in week 39 from 0.45 mnt in week 38, led by Dhamra (0.23 mnt) and Paradip (0.14 mnt). The recovery followed easing rains in Odisha and Chhattisgarh, which allowed miners to dispatch opportunistic cargoes that had been delayed.

Market sentiment, earlier dampened by concerns over a potential export duty, stabilised as activity normalised following rumours that the government is unlikely to impose it. China emerged as the largest importer, taking 0.20 mnt of India’s shipments.

Chile’s exports jumped 57% w-o-w to 0.55 mnt in week 39 from 0.35 mnt in week 38, driven by catch-up shipments from Huasco (0.20 mnt) and Totoralillo (0.17 mnt). The rebound reflected improved operational activity after earlier delays.

Strong offtake from China (0.47 mnt) and Japan (0.05 mnt) underpinned the recovery, even though Chile accounts for a relatively small share of the global market.

Peru’s shipments rose sharply by around 188% w-o-w to 0.85 mnt in week 39 from 0.29 mnt in week 38. Loadings at San Nicolas (0.68 mnt) and Matarani (0.17 mnt) gained momentum, with all cargoes destined for China. Shougang Hierro led the shipments, moving 0.68 mnt, of which 0.61 mnt went to China.

Market participants noted that Peruvian exports remain highly volatile due to infrastructure constraints. Nevertheless, strong demand for magnetite concentrate helped sustain the surge in shipments.

Freight market trends

Dry bulk iron ore freights remained firm in Week 39, with Pacific basin routes supported by steady demand from Australian miners, while Atlantic basin rates edged higher despite limited fixture activity. Australia-China flows benefitted from balanced tonnage and consistent cargo lists, though softer late-week sentiment capped upside.

Brazilian shipments were constrained by fewer fixtures, but the long-haul nature of the trade kept vessel supply tight, aiding owners’ position. South Africa’s exports gained from improved vessel availability, while Indian shipments faced pressure as Supramax rates softened on duty speculation, impacting cargo movement. Overall, freight conditions favoured smaller exporters in the Atlantic, helping offset declines in Australia and Brazil.

Outlook

Global iron ore exports are expected to remain broadly range-bound in the coming weeks. Australian iron ore exports may face pressure amid BHP case developments., while Brazil’s flows will depend on Atlantic fixture activity and vessel supply. Canada’s rebound highlights sensitivity to weather and port conditions, whereas South Africa faces persistent infrastructure constraints.

Indian exports are likely to stay opportunistic, while Chile and Peru may continue to contribute incremental gains. Freight trends across basins will remain the key driver, with Pacific rates underpinning steady flows and Atlantic dynamics dictating volatility.

Leave a Reply