- Higher shipments from Australia, Brazil, Canada drive gains in total

- Steady Australian, Brazilian export programmes to keep volumes high

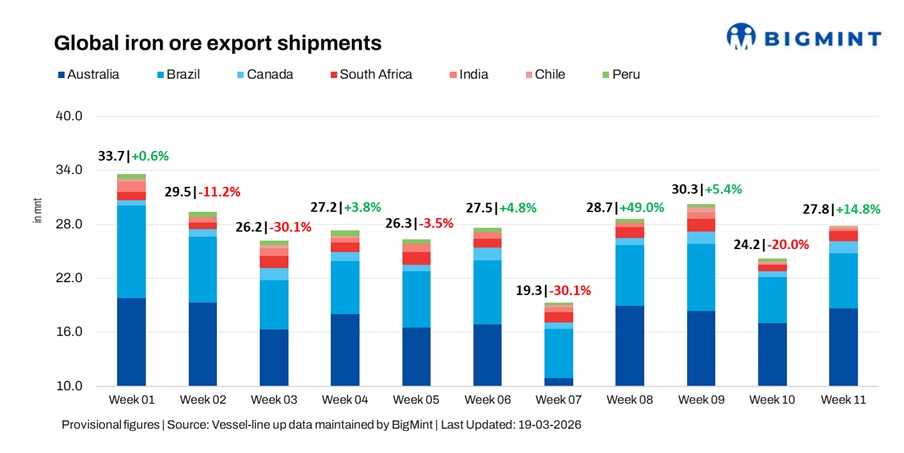

Global iron ore export shipments increased 14.8% w-o-w to 27.8 million tonnes (mnt) in the week ended 13 March, compared with 24.2 mnt in the previous week, according to BigMint vessel-line up data. The rise was primarily driven by higher exports from Australia, Brazil, Canada, South Africa, and India, supported by improved loading activity and logistics. Chile also recorded a slight increase, while Peru was the only major exporter to witness a sharp decline during the week amid lower vessel line-ups.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 11.2 mnt, Walcott 3.5 mnt, and Dampier 3.3 mnt. Rio Tinto exported 6.9 mnt, BHP 5.4 mnt, and FMG 4.7 mnt, with China absorbing 14.9 mnt, South Korea 1.5 mnt, and Japan 1.5 mnt.

- Brazil: Ponta da Madeira shipped 2.2 mnt. Vale exported 2.7 mnt, while Anglo shipped 1.9 mnt, with China importing 2.9 mnt and Bahrain 1.8 mnt.

- Canada: Sept-Iles shipped 0.8 mnt, while Port Cartier handled 0.5 mnt. Guinea and Nimba Mines exported 0.6 mnt and AMNS 0.5 mnt.

- South Africa: Saldanha handled 1.1 mnt and Richards Bay 0.1 mnt, with China receiving 0.4 mnt.

- India: Paradip shipped 0.1 mnt. KIOCL exported 0.1 mnt, with China importing 0.1 mnt.

- Peru: Matarani shipped 0.04 mnt, with Japan importing 0.04 mnt.

- Chile: Totoralillo shipped 0.2 mnt, with China importing 0.2 mnt.

Dry bulk iron ore freights edge up

Dry bulk iron ore freight rates edged up w-o-w on firm demand, geopolitical tensions, and higher bunker prices. The Pacific remained steady on Australia-China flows, while the Atlantic was supported by Brazil-China trade and longer tonne-mile demand.

Outlook

BigMint expects iron ore shipments to remain firm next week, supported by steady export programmes from major producers such as Australia and Brazil. However, freight market sentiment is likely to remain sensitive to bunker price volatility, vessel availability, and geopolitical developments, which could continue to influence global dry bulk trade dynamics.

Leave a Reply