- Shipments fall across major exporters; Peru records a modest rise

- Freight rates strengthen on steady cargo demand and geopolitical uncertainties

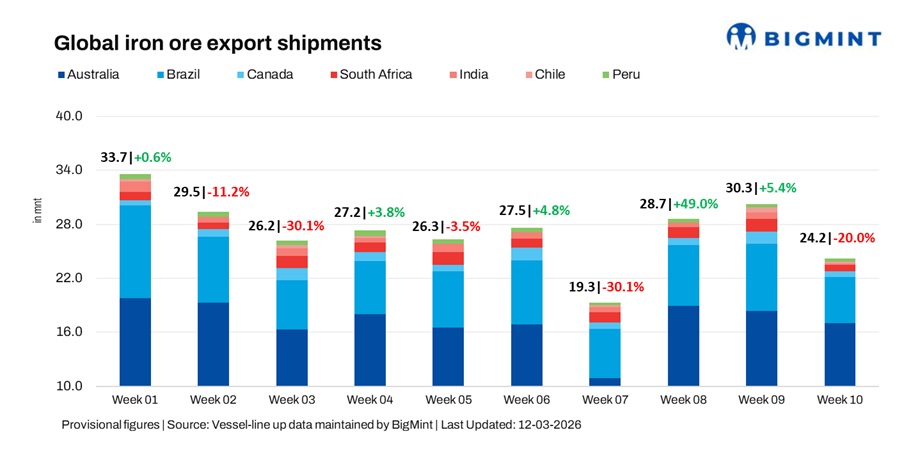

Global iron ore export shipments declined 20% w-o-w to 24.2 million tonnes (mnt) in the week ended 6 March, compared with 30.3 mnt in the previous week, according to BigMint vessel-line up data. The decline was largely driven by lower exports from Brazil, Canada, South Africa, India, and Chile, while Australian shipments also eased moderately after strong loading activity in previous weeks. Peru was the only major exporter to record a slight increase during the week.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 10.2 mnt, Dampier 3.2 mnt, and Cape Lambert 3.1 mnt. Rio Tinto exported 6.3 mnt, BHP 5.4 mnt, and FMG 3.1 mnt, with China absorbing 14.2 mnt and South Korea 1.5 mnt.

- Brazil: Ponta da Madeira shipped 2.2 mnt and Tubarao 1.2 mnt. Vale exported 3.1 mnt, while CSN shipped 1.8 mnt. China imported 3.1 mnt.

- Canada: Port Cartier handled 0.5 mnt, while Sept-Iles shipped 0.2 mnt. AMNS exported 0.5 mnt and IOC 0.2 mnt, with Spain importing 0.3 mnt.

- South Africa: Saldanha handled 0.5 mnt and Richards Bay 0.2 mnt, with China receiving 0.5 mnt

- India: Krishnapatnam and Paradip each shipped 0.1 mnt, with Malaysia importing 0.1 mnt.

- Peru: San Nicolas shipped 0.4 mnt and Matarani 0.1 mnt, with Shougang Hierro exporting 0.4 mnt to China.

- Chile: Guayacan shipped 0.2 mnt, with China importing 0.2 mnt.

Dry bulk iron ore freight improves w-o-w

Dry bulk iron ore freight rates rose w-o-w supported by improved cargo enquiries and firm vessel demand. The Pacific market remained steady on Australia-China flows and Chinese restocking, while the Atlantic stayed firm on continued Brazil-China trade and longer tonne-mile demand. Freight sentiment was further supported by geopolitical tensions influencing global shipping markets, pushing rates to multi-month highs on certain routes.

Outlook

Market participants expect iron ore shipments to remain relatively stable in the near term as export programmes from major producers such as Australia and Brazil continue. However, freight market sentiment may remain sensitive to vessel availability, bunker price movements, and geopolitical developments, which could continue to influence global dry bulk shipping dynamics.

Leave a Reply