- Canada posts modest gains, Peru resumes exports after week-long lull

- Freight rates stay supported as stronger Capesize demand lifts sentiment

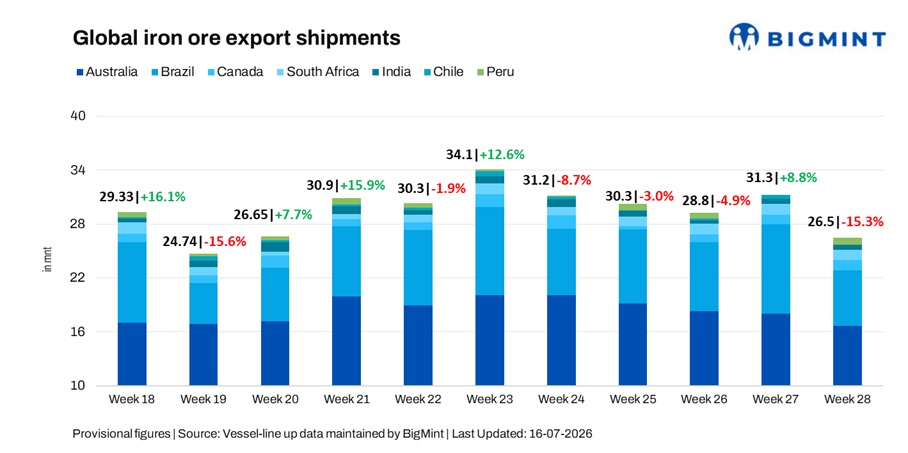

Global seaborne iron ore exports fell 15.3% w-o-w to a nine-week low of 26.5 million tonnes (mnt) in the week ended 10 July, driven by lower shipments from Australia and Brazil. Although Canada posted a modest recovery and Peru resumed exports after a quiet previous week, the increase failed to offset the decline in volumes from the two leading exporters.

Port & shipper-wise trends

- Australia: Port Hedland handled 10.77 mnt, followed by Dampier (3.16 mnt) and Port Walcott (2.09 mnt). BHP shipped 5.47 mnt, followed by Rio Tinto (5.26 mnt) and FMG (3.90 mnt). China remained the leading destination at 13.53 mnt, followed by Japan (1.37 mnt).

- Brazil: Ponta da Madeira handled 2.75 mnt, followed by Itaguai (1.84 mnt) and Tubarao (0.78 mnt). Vale shipped 3.21 mnt, while CSN accounted for 2.62 mnt. China remained the largest importer at 1.70 mnt, followed by the Netherlands (0.50 mnt).

- Canada: Sept-Iles handled 0.62 mnt, followed by Port Cartier (0.55 mnt). AMNS shipped 0.55 mnt, while Guinea & Nimba Mines accounted for 0.38 mnt. The Netherlands emerged as the key destination at 0.29 mnt, followed by Vietnam (0.17 mnt).

- South Africa: Saldanha handled 1.10 mnt, followed by Richards Bay (0.08 mnt). Japan emerged as the leading destination at 0.25 mnt, followed by the Netherlands (0.20 mnt).

- India: Paradip handled 0.18 mnt, followed by Kandla (0.11 mnt) and Dhamra (0.11 mnt). Rungta Sons shipped 0.12 mnt. China remained the major destination at 0.17 mnt, followed by the UAE (0.11 mnt).

- Chile: Mejillones handled 0.04 mnt. China accounted for the entire shipment volume at 0.04 mnt.

- Peru: San Nicolas handled 0.70 mnt. Shougang Hierro shipped 0.70 mnt. China accounted for the entire shipment volume at 0.75 mnt.

Capesize strength lifts freight

The iron ore freight market strengthened during the week, supported by firmer Capesize demand across the Pacific and Atlantic basins. Higher cargo enquiries from Australia and Brazil improved vessel utilisation, while tighter prompt tonnage and healthy long-haul fixtures underpinned freight rates. Labour developments in Australia’s Pilbara region remained under watch, though loading operations continued without significant disruption.

Outlook

Global iron ore exports are expected to remain broadly range-bound in the near term, with shipment volumes dependent on loading programmes in Australia and Brazil, seasonal logistics and vessel line-ups. Demand from key Asian importers, particularly China, will also remain a crucial factor. Meanwhile, freight rates are likely to stay firm as healthy Capesize demand, improving vessel utilisation and tight prompt tonnage continue to underpin the market.

Leave a Reply