- Higher voyage costs, muted China restocking curb shipment activity

- Brazil, Peru provide upside even as South Africa, Chile shipments drop

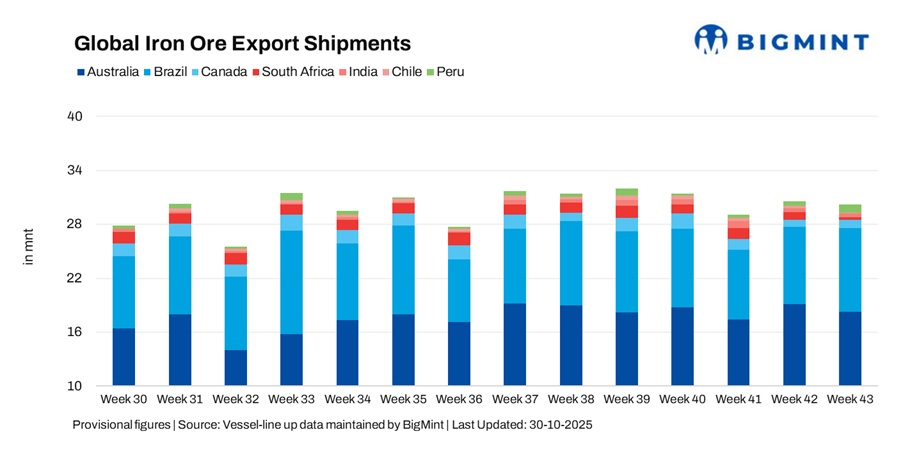

Global iron ore exports edged down 1.9% w-o-w to 30.14 million tonnes (mnt) in week 43 (18-24 October 2025), from 30.73 mnt in week 42 (11-17 October 2025). The marginal decline was led by reduced shipments from Australia, South Africa, India, and Chile, offset partially by higher volumes from Brazil and Peru.

The dip came despite a rebound in freight markets across key Pacific and Atlantic routes. Rising bunker prices and firmer FFAs lifted sentiment, but the accompanying increase in voyage costs restrained exporters from scheduling additional shipments. Traders noted that while freight momentum has improved, subdued Chinese steel margins and cautious restocking interest continued to cap buying appetite.

Country-wise trends

Australia’s iron ore exports fell 4.1% w-o-w to 18.33 mnt in week 43, down from 19.12 mnt in week 42, as miners adjusted shipment schedules amid firmer freight rates and subdued Chinese demand.

Port-wise, Port Hedland led with 11.08 mnt, followed by Dampier (3.39 mnt) and Cape Lambert (3.37 mnt). Among miners, Rio Tinto shipped about 6.75 mnt, BHP 5.49 mnt, and FMG 4 mnt. Maintenance at Dampier, rail bottlenecks, and mine scheduling cuts further constrained volumes. China remained the leading importer of Australian iron ore in Week 43, taking around 15.34 mnt, followed by South Korea with 0.75 mnt and Japan with 0.62 mnt.

Despite firmer Australia-China freights, chartering activity stayed muted as miners favored long-term contracts over spot deals. Additionally, the pricing standoff between BHP and China Mineral Resources Group (CMRG) dampened near-term sentiment, leading to booking delays from Chinese buyers.

Brazil’s iron ore exports rose 7.4% w-o-w to 9.26 mnt in week 43, up from 8.62 mnt in week 42, reflecting a steady rebound supported by improved loading operations and favorable Atlantic weather.

CSN Mineracao led shipments with 4.27 mnt, closely followed by Vale at 4 mnt. Port-wise, activity was concentrated at Ponta da Madeira (3.23 mnt), Itaguai (2.15 mnt), and Tubarao (2.11 mnt). Exporters leveraged the firmer freight environment to advance cargoes ahead of planned maintenance in early November.

On the demand front, Chinese imports from Brazil increased modestly to 3.84 mnt, aided by steady restocking by select mills. Meanwhile, European and Middle Eastern buyers showed stronger interest amid competitive Atlantic freight levels. Overall, stable export performance and balanced demand dynamics kept Brazil’s shipment momentum firm through the week.

Canada’s iron ore exports inched up 5.8% w-o-w to 0.85 mnt in week 43, compared with 0.81 mnt in week 42, supported by stable weather and improved vessel scheduling at key eastern ports. Operations at Sept-Iles (0.47 mnt) and Port Cartier (0.38 mnt) remained steady, helping maintain consistent shipment flows despite moderate global demand.

Among exporters, AMNS led with 0.38 mnt, followed by the IOC at 0.30 mnt, and Guinea & Nimba Mines contributing around 0.10 mnt. Exporters continued to focus on optimizing vessel turnaround and blending higher-grade cargoes to attract European and East Asian buyers.

However, European demand stayed soft due to elevated freight costs and compressed steel mill margins, prompting cautious booking activity. Of the total shipments, approximately 0.29 mnt were directed to Europe and 0.17 mnt to Japan, while Asian intake remained limited as buyers favored shorter-haul origins amid steady Pacific freight levels.

South Africa’s iron ore exports slumped 66% w-o-w to 0.29 mnt in week 43, down from 0.86 mnt in week 42, marking the sharpest weekly fall among major exporters. The decline was primarily driven by logistical disruptions on the Transnet rail network, which restricted movement to Saldanha Bay, the sole active export hub, while Richards Bay recorded negligible activity.

Despite stable mine output, shipment activity was hampered by rail bottlenecks, vessel delays, and limited port stock availability, prompting several cargo deferments. The impact of these logistical challenges outweighed the benefit of a firmer freight market, which otherwise supported exporters in other regions.

At the production level, Kumba Iron Ore’s output remained largely steady in Q3CY’25, but maintenance and infrastructure constraints continued to affect its export performance.

India’s iron ore exports declined 4.2% w-o-w to 0.42 mnt in week 43, down from 0.44 mnt in week 42, as exporters adopted a cautious stance amid rising freight rates and tepid Chinese buying interest. Despite adequate vessel availability, shipment activity slowed as traders focused on margin protection and deferred select cargoes due to higher voyage costs.

Port activity was concentrated at Dhamra (0.18 mnt) and Paradip (0.14 mnt), supported by steady loading operations. Among exporters, Vedanta (0.13 mnt) and Rungta Sons (0.12 mnt) led the week’s shipments, primarily targeting China.

While freight levels on the India-China Supramax route strengthened alongside broader market gains, the higher voyage expenses eroded exporter margins. China accounted for nearly 0.25 mnt of India’s exports. Market participants noted that ongoing freight volatility and subdued buying appetite are likely to keep near-term export activity moderate.

Chile’s iron ore exports fell sharply by 69.8% w-o-w to 0.10 mnt in week 43, compared with 0.34 mnt in week 42, as tight cargo availability and subdued trading interest weighed on overall shipments.

All loadings were concentrated at Mejillones Port (0.10 mnt), while other key terminals remained inactive amid reduced mining dispatches. Market participants noted that weak Chinese demand and rising freight costs eroded margins on smaller cargoes, prompting several traders to defer shipments.

With exporters prioritising cost efficiency and buyers showing limited appetite for long-haul cargoes, Chile’s short-term export outlook remains muted, despite stable mine output and adequate port capacity.

Peru’s iron ore exports jumped 61.9% w-o-w to 0.89 mnt in week 43, up from 0.55 mnt, marking the second consecutive weekly rise amid smoother port operations and steady mining output.

Shipments were concentrated at San Nicolas (0.69 mnt) and Matarani (0.20 mnt), with Shougang Hierro contributing nearly the entire export volume. All cargoes were bound for China (0.83 mnt), driven by restocking demand from northern steel mills.

However, traders suggested the rebound was primarily operational rather than demand-led, with limited signs of sustained growth as Chinese buying interest remains cautious amid volatile steel margins.

Dry bulk iron ore freight markets strengthened w-o-w on improved sentiment and higher fixtures across major routes. Gains were led by increased chartering activity in both the Pacific and Atlantic basins, supported by firmer FFAs and rising bunker prices.

However, the higher voyage costs limited exporters’ flexibility, prompting selective shipment delays, particularly from Australia and India. Despite this, active miner-led fixtures from Brazil and robust Capesize demand lent support to overall freight averages. The firmer freight backdrop, while positive for vessel owners, constrained marginal exporters, keeping total global shipment volumes slightly lower on the week.

Outlook

The global iron ore trade is expected to remain range-bound in the near term as freight markets stabilize and demand indicators stay mixed. Australia may see continued moderation amid miner caution and cost pressures, while Brazil could maintain momentum if Atlantic fixture activity remains strong.

Peru’s rebound and Canada’s steady performance offer limited upside, whereas South Africa and Chile face persistent logistical and operational challenges. Although freight sentiment remains firm, sustained recovery in export momentum will depend on Chinese restocking appetite and the stability of Capesize market dynamics over the coming weeks.

Leave a Reply