- Australian and Brazilian shipments weaken

- South African, Indian exports support global trade

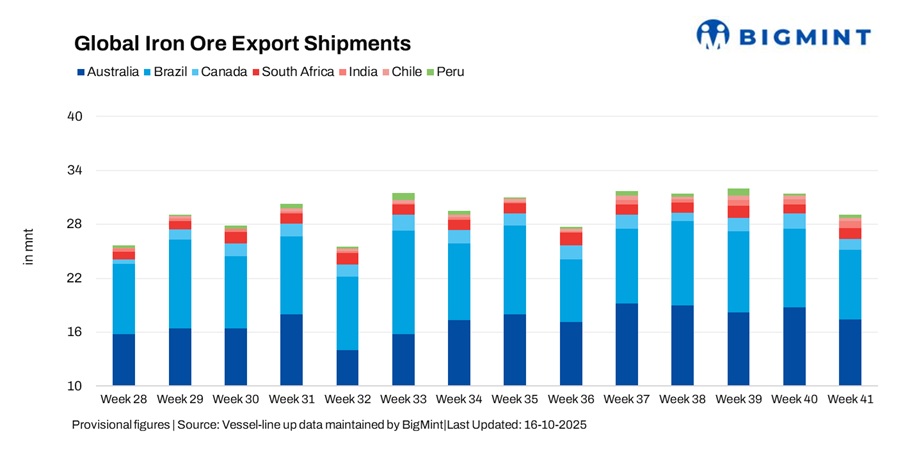

Global iron ore exports fell 6.8% w-o-w in week 41 (4-10 October 2025) to 29.20 mnt, down from 31.32 mnt in the previous week. The drop was primarily driven by a pullback in shipments from Australia, Brazil, Canada, and Chile, while India, South Africa, and Peru posted gains that provided partial support.

The decline in volumes coincided with a sharp drop in dry bulk freight rates across major routes, led by weaker demand, oversupply of tonnage, and subdued chartering sentiment. The resulting freight softness further discouraged new fixture activity, especially from the Pacific basin, adding to headwinds for exporters already grappling with cautious Chinese buying and logistical constraints.

Country-wise trends

Australia’s iron ore exports declined by 7.2% w-o-w to 17.41 mnt, down from 18.76 mnt in week 40. Despite steady production from major miners – Rio Tinto (6.27 mnt), BHP (5.42 mnt), and FMG (4.02 mnt) – export activity was constrained by a muted pace of bookings, driven in part by an ongoing pricing standoff between BHP and China Mineral Resources Group (CMRG) and persistently weak Pacific freight rates. Charterers showed limited urgency to secure cargoes, often negotiating at lower freight rates.

Shipments were led by Port Hedland at 10.77 mnt, followed by Walcott with 3.24 mnt and Dampier with 3.03 mnt. China remained the top importer, receiving 13.69 mnt of Australia’s iron ore exports during the week. Amid the dispute, BHP has reportedly agreed to settle 30% of its spot iron ore trade with China in yuan, with the agreement set to take effect in Q4 2025.

Brazil’s iron ore exports declined by 10.1% week-on-week to 7.80 mnt s, down from 8.68 mnt the previous week. The drop was primarily driven by weaker buying interest from China, which imported only 4.14 million tonnes, and a slowdown in fixture activity across the Atlantic basin. This decline occurred despite stable loading volumes from key ports, including Ponta da Madeira (3.95 mnt), Itaguai (1.19 mnt), and Tubarao (1.48 mnt).

While vessel availability improved slightly, the lack of forward bookings and only occasional fixtures kept export momentum subdued. Vale remained the top exporter with 4.15 mnt but held back on additional loadings in response to soft market signals and tepid demand.

Canada’s iron ore exports dropped by 28.9% week-on-week to 1.21 mnt, down from 1.71 mnt, as shipping activity normalized following the clearance of weather-related backlogs in prior weeks. Loadings eased from key ports, with Sept-Iles handling 0.74 mnt and Port Cartier 0.31 mnt, amid a general slowdown in logistical throughput. Although operational conditions remained stable, the soft freight market and lack of strong restocking interest from major buyers limited fresh cargo movements.

Exporters such as IOC (0.49 mnt), AMNS Canada (0.31 mnt), and Guinea & Nimba Mines (0.25 mnt) reported lower vessel turnover compared to late September. The Netherlands was the largest importer at 0.47 million tonnes, followed by Spain, Japan, and Bahrain, each receiving 0.17 million tonnes.

South Africa’s iron ore exports increased by 25.1% week-on-week to 1.23 mnt, up from 0.98 mnt, as improved logistical conditions supported a recovery in volumes. Saldanha Bay led the surge with 1.11 mnt shipped, driven by improved rail connectivity and better vessel coordination, while activity at Richards Bay remained subdued at 0.12 million tonnes.

The uptick was primarily supported by Asian demand, with South Korea importing 0.38 mnt, although shipments to China remained sluggish at 0.17 mnt. Despite the rebound, market participants remained cautious about the sustainability of the recovery amid ongoing infrastructure challenges.

India’s iron ore exports surged by 48.9% w-o-w to 0.83 mnt, up from 0.56 mnt in Week 40, marking a strong rebound. Loadings picked up across key ports, with Paradip handling 0.28 mnt, Dhamra 0.19 mnt, and Gopalpur 0.17 mnt, supported by easing concerns around export duty changes and improved availability of Supramax vessels.

Strong restocking demand from China (0.42 mnt) and Southeast Asia following the Golden Week holiday, coupled with competitive pricing, boosted booking activity. However, market sentiment remains cautious amid ongoing freight rate volatility and lingering policy uncertainty.

Chile’s iron ore exports fell by 24.3% week-on-week to 0.32 mnt, down from 0.43 mnt in Week 40, as cargo availability declined and port activity slowed at Totoralillo (0.20 mnt) and Mejillones (0.13 mnt).

Although buyers in China (0.23 mnt) and South Korea (0.05 mnt) remained engaged, their activity was subdued due to weak near-term demand and declining freight rates. Traders reported that while port infrastructure remained stable, the overall lack of urgency in procurement continued to weigh on shipment volumes.

Peru’s iron ore exports surged by 89.1% week-on-week to 0.39 mnt, up from 0.21 mnt, rebounding from previous lows as loadings resumed at San Nicolas (0.34 mnt) and Matarani (0.05 mnt).

All shipments were directed to China, which received 0.22 mnt, with Shougang Hierro contributing the majority of exports at 0.34 mnt. Despite the sharp increase, traders emphasized that the rebound was primarily operational, and sustained export momentum would depend on stronger forward demand.

Dry bulk iron ore freights came under sharp pressure during week 41, with rates across key global routes declining to one month low. In the Pacific basin, the oversupply of tonnage, limited post-holiday cargo inquiries, and the ongoing standoff between BHP and Chinese buyers led to a steep decline in freight levels. Exporters from Australia and India faced mounting difficulty in securing competitive fixtures, with many choosing to delay or cancel bookings altogether.

In the Atlantic basin, trade remained thin, with very few fixtures reported on the Brazil-China and South Africa-China corridors. The freight weakness acted as both a constraint and a disincentive for exporters, as falling rates failed to generate meaningful spot demand and instead added to the overall cautious sentiment in the market.

Outlook

The global iron ore trade is expected to remain subdued in the near term, as weaker freight economics, muted Chinese buying, and operational adjustments post-holidays shape market direction. Australia may continue to see volume pressure if freight sentiment fails to improve and the BHP-CMRG pricing standoff persists. Brazilian exports could remain underwhelming unless Atlantic fixture activity revives.

India may hold up in the short term if Supramax availability stays high and policy clarity is sustained. South Africa’s trajectory remains dependent on infrastructure stability, while Canada and Chile may continue to experience quieter weeks. Peru’s recent recovery may not last unless buyer engagement improves. Overall, with freight markets under strain and no immediate catalysts for demand revival, export momentum is likely to stay range-bound.

Leave a Reply