- Australia volumes ease on weaker cargo flow and cautious fixing

- Freight firm on higher bunkers, but China demand cautious

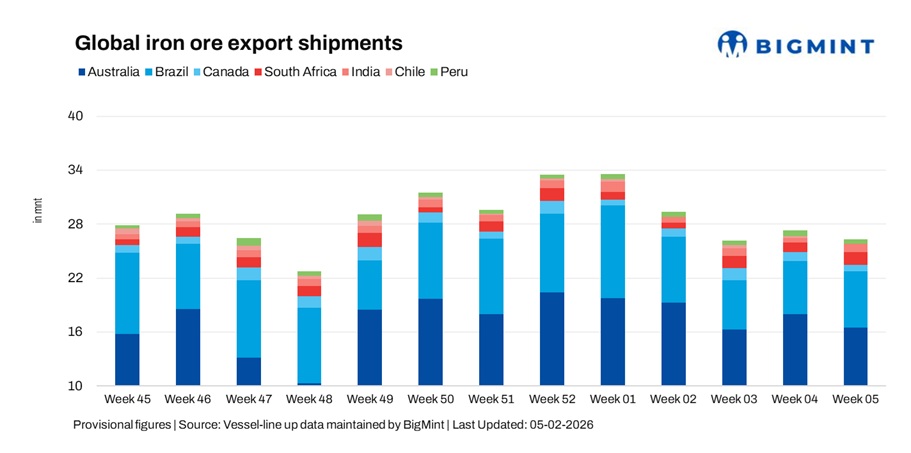

Global seaborne iron ore exports fell 3.5% w-o-w to 26.3 mnt in the week ended 30 January 2026, compared with 27.2 mnt in the previous week, as per vessel line-up data. The decline was led by lower shipments from Australia, Canada, Peru and Chile, which outweighed gains from Brazil, South Africa and India. Freight markets stayed firm on higher bunker costs and stronger fixtures, but export momentum remained capped by cautious chartering and weak Chinese steel margins.

The fall reflected uneven cargo scheduling, with some producers slowing loadings after last week’s rebound. Higher voyage costs supported freight sentiment but kept long-haul shipments sensitive to timing and freight affordability.

Country-wise trends

Australia exports ease on slower cargo flow

Australia’s iron ore exports fell 8.5% w-o-w to 16.5 mnt, easing as cargo flow slowed and shipment schedules normalised, while firm freight costs kept fixing cautious. Port Hedland led loadings with 10.34 mnt, followed by Walcott (2.95 mnt) and Dampier (2.47 mnt).

Rio Tinto shipped 5.41 mnt, BHP 5.06 mnt and FMG 3.96 mnt. China remained the key destination at 14.88 mnt, while Japan, Indonesia and South Korea imported 0.44 mnt, 0.43 mnt and 0.41 mnt, respectively. Despite the weekly decline, Australia’s January exports remained firm on a year-on-year basis, reflecting resilient supply capacity and steady long-term demand from Asia.

Brazil exports rise on firmer long-haul fixing

Brazil’s iron ore exports rose 7.2% w-o-w to 6.3 mnt, supported by improved long-haul fixing sentiment and higher cargo releases from key terminals despite cautious steel demand. Ponta Da Madeira led loadings with 1.66 mnt, followed by Itaguai (1.46 mnt), Tubarao (1.36 mnt) and Ilha Guaiba (1.01 mnt).

On the shipper side, CSN accounted for 2.82 mnt, while Vale shipped 2.67 mnt. China remained the key destination, importing 3.19 mnt, though buying stayed selective amid weak downstream margins and bunker-driven voyage costs. Meanwhile, recent operational disruptions at Vale-linked units in Minas Gerais, following water overflow incidents and regulatory action, have increased market attention on potential near-term shipment scheduling risks.

Canada exports slide on weaker Atlantic flow

Canada’s iron ore exports fell 28.7% w-o-w to 0.7 mnt, pressured by weaker Atlantic cargo flow and fewer cargo nominations, with the decline largely driven by shipment scheduling rather than operational issues. Sept-Iles led loadings with 0.43 mnt, followed by Port Cartier at 0.26 mnt.

On the shipper side, AMNS India and IOC shipped 0.26 mnt each, while Guinea & Nimba Mines contributed 0.18 mnt. The Netherlands remained the top destination at 0.36 mnt, followed by France at 0.19 mnt, as rising freight costs and cautious demand kept export volumes vulnerable to timing shifts. Additionally, recent regulatory clearance for the expansion of Canada’s Mary River iron ore project has renewed focus on the country’s longer-term export growth potential, even as near-term volumes remain volatile.

South Africa exports rebound on Saldanha flow

South Africa’s iron ore exports rose 25% w-o-w to 1.4 mnt, supported by improved cargo scheduling and steady terminal operations. Saldanha Bay handled the complete volume during the week, reflecting smoother cargo clearance compared with the previous period.

China remained the key destination, importing 0.44 mnt. Despite the rebound, South African exports continued to remain volatile and highly sensitive to freight economics and long-haul demand. Meanwhile, ongoing government and industry efforts to improve rail-port logistics linked to the Saldanha bulk minerals corridor could provide medium-term support to export stability, although infrastructure bottlenecks remain a key risk factor.

India exports surge on stronger east coast flow

India’s iron ore shipments jumped 76.6% w-o-w to 0.9 mnt, supported by stronger east coast loadings and improved short-haul fixing interest. Paradip led shipments with 0.61 mnt, followed by Dhamra at 0.12 mnt, reflecting firmer cargo flow compared with the previous week.

On the shipper side, Vedanta accounted for 0.20 mnt, while China remained the key destination, importing 0.42 mnt. India’s rebound helped cushion the overall global decline, though export momentum remains sensitive to domestic demand conditions and freight economics. Meanwhile, ongoing discussions around iron ore export duty structures, along with gradual infrastructure upgrades at key east coast ports, could influence India’s shipment flexibility and competitiveness in the coming weeks.

Chile exports drop to zero on no cargoes

Chile’s iron ore exports fell 100% w-o-w to nil, as no cargoes were recorded during the week compared with 0.2 mnt in the previous week. The decline reflected the absence of scheduled shipments and irregular cargo availability, keeping export volumes highly timing-driven rather than demand-led.

Chile remains a marginal contributor to global iron ore trade, leaving weekly flows volatile. However, the country’s recently announced National Critical Minerals Strategy, aimed at diversifying mining exports beyond copper, highlights Chile’s longer-term intent to strengthen its broader mineral export footprint despite short-term shipment irregularities.

Peru exports ease on softer cargo flow

Peru’s iron ore exports slipped 5.4% w-o-w to 0.5 mnt, as cargo movement eased slightly due to shipment timing and selective fixing. San Nicolas remained the sole active loading port, handling 0.52 mnt during the week.

On the shipper side, Shougang Hierro accounted for 0.52 mnt, while China remained the only destination, importing 0.52 mnt, highlighting Peru’s heavy dependence on Asian demand and freight-led shipment scheduling. Meanwhile, Peru’s broader mining outlook is expected to improve, with the government anticipating several large-scale mining projects to begin construction in 2026, which could support export stability over the medium term.

Freight firm on higher bunkers

Iron ore freight rates strengthened w-o-w, supported by higher bunker costs following a sharp rise in Brent crude prices and firmer fixture conclusions across key routes. The rise in voyage expenses encouraged shipowners to push for higher levels, while improved fixing activity provided near-term support despite softer iron ore prices.

However, the freight strength appeared largely cost-driven rather than demand-led, as Chinese steel demand remained cautious. Higher voyage costs also tightened long-haul economics, potentially limiting aggressive shipment expansion from Atlantic exporters as charterers stayed selective and timing-focused.

Outlook

Global iron ore shipments are expected to remain broadly steady but volatile in the near term, with exporters continuing to prioritise shipment timing over aggressive volume expansion. While firm freight sentiment and higher bunker costs may support rates and encourage owners to hold ground, the upside in export momentum is likely to remain capped by cautious Chinese demand, weak steel margins, and selective chartering behaviour.

Australia is expected to remain the key swing factor in global volumes, while Brazil and South Africa may continue to see selective long-haul support depending on freight economics. Short-haul suppliers such as India may retain intermittent strength, though overall trade flows are likely to stay range-bound with pockets of week-to-week fluctuation.

Leave a Reply