- Australian, Indian declines outweigh Brazil and Peru growth

- Weak Capesize market weighs on freight sentiment

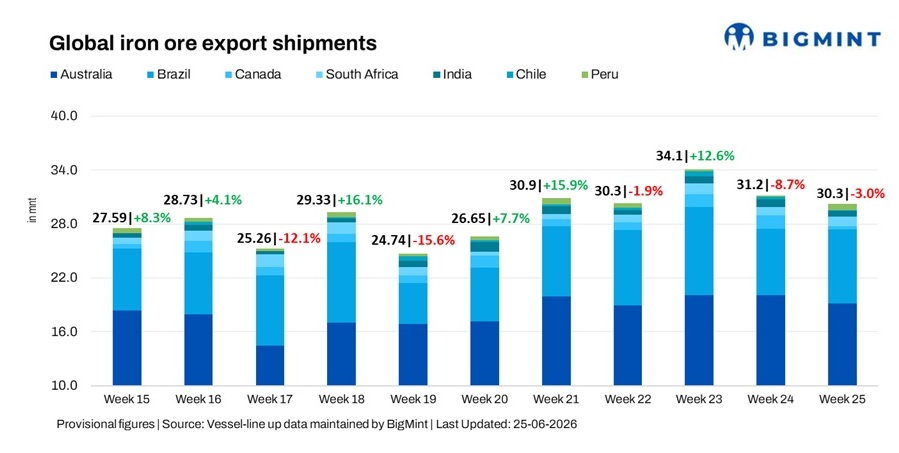

Global iron ore export shipments declined 3% w-o-w to 30.3 million tonnes (mnt) in the week ended 19 June, from 31.2 mnt a week earlier, according to BigMint data, matching a four-week low.

Weaker cargo flows from Australia, India, Canada, and Chile outweighed stronger loadings from Brazil, South Africa, and Peru. Australia continued to be the largest exporter despite reduced shipments from the Pilbara region, while Brazil saw a recovery supported by improved Vale loading programmes.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 12.9 mnt, followed by Dampier (3.3 mnt) and Port Walcott (2.6 mnt). BHP exported 6.3 mnt, Rio Tinto shipped 5.9 mnt, while FMG moved 4.8 mnt. China remained the largest importer at 16.8 mnt, followed by Japan (1.2 mnt).

- Brazil: Ponta da Madeira handled 3.8 mnt, followed by Tubarao (2.2 mnt) and Itaguai (1.5 mnt). CSN exported 7.5 mnt, while Vale shipped 0.5 mnt. China remained the largest importer at 4.3 mnt.

- Canada: Sept-Iles handled 0.3 mnt. Guinea & Nimba Mines exported 0.2 mnt, while Belgium and Germany imported 0.08 mnt each.

- South Africa: Saldanha handled 1.1 mnt, with China importing 0.3 mnt.

- India: Dhamra handled 0.2 mnt, followed by Mormugao (0.17 mnt) and Paradip (0.14 mnt). Rungta Sons exported 0.14 mnt, while China and Malaysia imported 0.14 mnt and 0.12 mnt, respectively.

- Chile: Mejillones handled 0.05 mnt, with China importing the entire volume.

- Peru: San Nicolas handled 0.69 mnt. Shougang Hierro exported 0.69 mnt, with China importing 0.52 mnt.

Freight market remains under pressure

Iron ore freight rates remained under pressure during the week as subdued Chinese buying interest and limited cargo enquiries weighed on Capesize activity. Softer Pilbara loading programmes further dampened Pacific sentiment, while Brazil’s recovery in Vale loadings provided only partial support to Atlantic demand. Lower cargo availability from Canada and Chile also limited long-haul fixture activity.

The Capesize market continued to underperform amid ample vessel availability and weaker market indicators, although Panamax and Supramax segments remained comparatively stable on steady minor bulk demand.

Outlook

Global iron ore shipments are expected to remain mixed in the coming weeks as loading programmes across Australia and Brazil, seasonal weather conditions, and Chinese steel demand continue to shape seaborne trade. Freight sentiment is likely to stay under pressure amid ample Capesize availability, although any improvement in cargo enquiries or vessel utilisation could lend support to freight rates.

</a

</a

Leave a Reply