- Atlantic mixed as Brazil, South Africa offset partial weakness

- Pacific freights ease on FFA pressure, demand steady

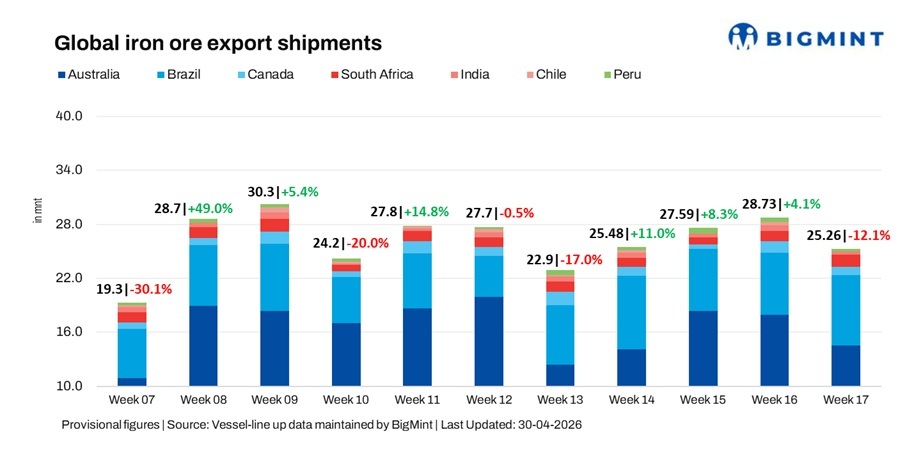

Global iron ore export shipments fell 12.1% w-o-w to 25.3 million tonnes (mnt) in the week ended 24 April, from 28.7 mnt a week earlier, according to BigMint data. The decline was led by lower Australian volumes amid maintenance, while Atlantic flows remained mixed, with Brazil and South Africa offering partial support.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 7.65 mnt, Walcott 3.63 mnt, and Dampier 2.92 mnt. Rio Tinto exported 6.55 mnt, BHP 4.22 mnt, and FMG 3.00 mnt, with China absorbing 12.52 mnt, followed by Japan (1.61 mnt).

- Brazil: Ponta da Madeira shipped 2.96 mnt, Tubarao 1.94 mnt, and Itaguai 1.38 mnt. Vale exported 3.52 mnt, while CSN shipped 3.44 mnt, with China importing 4.40 mnt.

- Canada: Port Cartier shipped 0.63 mnt and Sept-Iles 0.31 mnt, with AMNS exporting 0.63 mnt and Guinea & Nimba Mines 0.21 mnt, while the USA received 0.22 mnt.

- South Africa: Saldanha handled 1.19 mnt and Richards Bay 0.17 mnt, with China receiving 0.56 mnt.

- India: Dhamra shipped 0.14 mnt and Paradip 0.11 mnt, with China importing 0.17 mnt.

- Peru: San Nicolas shipped 0.17 mnt and Matarani 0.12 mnt, with Shougang Hierro exporting 0.17 mnt, while China imported 0.30 mnt.

Bulk iron ore freights under pressure

Freights softened w-o-w, with the Pacific under pressure from weaker FFAs and cautious sentiment despite steady cargo demand. Limited fresh enquiry weighed on key Australia-China routes. The Atlantic remained relatively firm, supported by balanced cargo flows from Brazil and South Africa, though ample vessel supply capped upside.

Outlook

Shipments are likely to remain uneven in the near term, with ongoing maintenance at key Australian ports continuing to influence loading activity, while Atlantic flows are expected to stay relatively stable amid improving operational performance.

Freight sentiment may remain mixed, with Pacific rates sensitive to FFA movements and demand visibility, while Atlantic fundamentals remain comparatively balanced, though vessel availability could limit gains.

Leave a Reply