- Brazil, India shipments fall, rise from other countries

- Weak mill margins, high port stocks dull China appetite

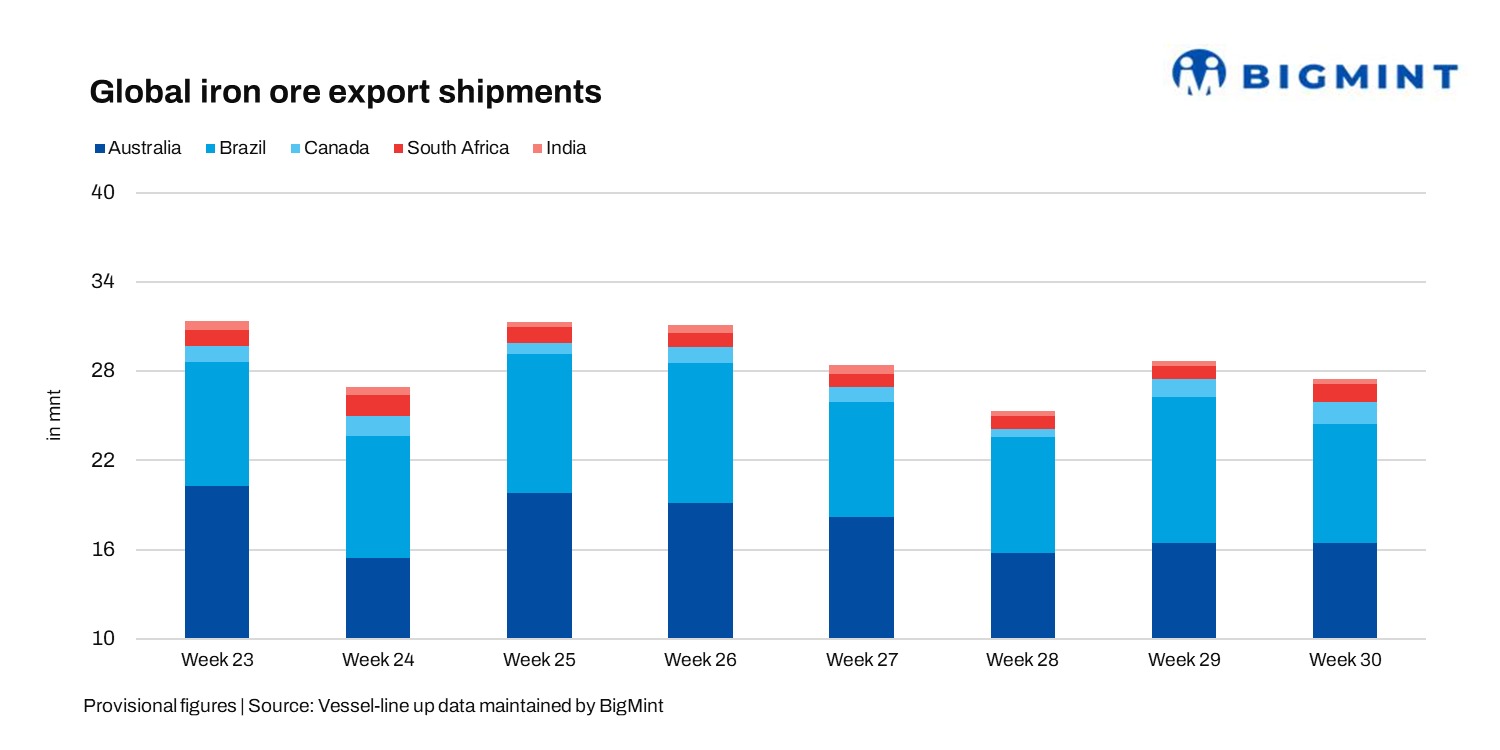

In July 2025, global iron ore and pellet shipments declined 4% w-o-w in Week 30, 2025 (19th-25th July), falling to 27.89 million tonnes (mnt) from 29.10 mnt in Week 29 (12th –18th July), vessel line-up data from BigMint shows. The pullback was driven by easing volumes from Brazil and India amid subdued spot activity and cautious procurement from Chinese mills.

The overall sentiment in the seaborne iron ore market remained slightly bearish in Week 30. Weak Chinese steel margins, combined with persistently high portside inventories, continued to weigh on fresh buying interest from mills. Buyers showed increased price sensitivity, preferring cost-effective, mid-grade Australian fines as benchmark indices softened.

Shipments from Brazil, India fall w-o-w

Australia’s iron ore and pellet exports held steady at 16.41 million tonnes (mnt) in Week 30, recording a marginal dip of just 0.05% from 16.42 mnt in Week 29, reflecting largely flat w-o-w performance. Indian traders also adopted a cautious approach, as Chinese procurement trends shifted towards more competitively priced alternatives, including increased reliance on Australian and Brazilian cargoes. However, the bearish undertone was somewhat offset by logistical recoveries in select origins notably Canada and South Africa which managed to post weekly export growth due to improved rail-port connectivity and stable operations.

Rio Tinto (5.48 mnt), BHP (5.07 mnt), and Fortescue Metals Group (4.22 mnt) remained the primary drivers of export volumes in Week 30. China remained the primary destination, followed by South Korea and Japan.

The sentiment remained stable, supported by uninterrupted port operations and consistent off-take from Chinese mills, particularly for low- and mid-grade fines that offer cost advantages. Australia’s cyclone-affected ports entered recovery by early Q2 2025, with key hubs like Port Hedland and Dampier resuming normal export cycles.

Brazil’s iron ore export volumes eased to 8.01 million tonnes (mnt) in Week 30, marking a 19% decline from 9.86 mnt in Week 29. The drop followed a front-loaded spike in shipments during the previous week.

Minor port congestion and a normalisation in cargo flow after the earlier surge contributed to the slightly reduced volumes.

Some miners also opted to hold back cargoes as Chinese buyers placed lower bids, reflecting a cautious procurement trend amid subdued price sentiment. Meanwhile, Itaminas’ initiation of direct exports via Porto Sudeste signalled a strategic shift in Brazil’s logistics landscape. The terminal’s growing capacity and throughput performance have started playing a key role in streamlining ore shipments.

Canada’s iron ore exports climbed up 23% w-o-w to 1.46 mnt in Week 30, up from 1.19 mnt in Week 29. This surge was largely attributed to smoother logistics, particularly rail-to-port connectivity in eastern Canada where operations at key ports like Sept Iles and Port Cartier underpin efficient cargo handling.

The logistics recovery enabled smoother cargo flow, contributing to higher shipment volumes. Demand was also bolstered by increased interest from European buyers, particularly the Netherlands (0.36 mnt) and Spain (0.26 mnt), which are seeking premium grade iron ore.

South Africa’s iron ore exports recorded the strongest w-o-w growth among key exporters, rising by 43% to 1.25 mnt in Week 30. The surge was driven by improved port activity at Richards Bay, where smoother rail-to-port flows enabled higher shipment volumes.

Additionally, renewed restocking interest from Chinese buyers supported the uptick. Looking ahead, export volumes are likely to remain elevated in the near term, with no major logistics disruptions anticipated.

India’s iron ore exports remained largely stable 0.35 mnt in Week 30 in July 2025 from 0.34 mnt in the prior week. Despite the marginal rise, overall market sentiment remained subdued, pressured by competitive global prices and muted Chinese buying interest.

Leave a Reply