- Export prices, however, retreat w-o-w

- Global banking crisis impacts market sentiments

- Iron ore prices dip on China crackdown

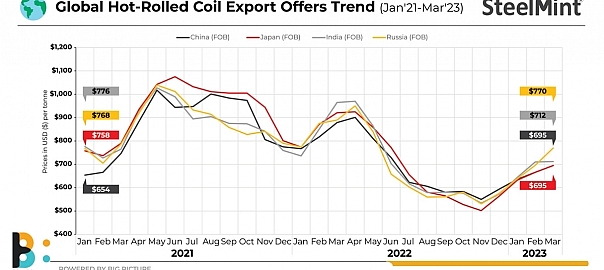

Morning Brief: Global hot rolled coil (HRC) export offers have not really shown any major m-o-m spurt despite the price rise seen recently. Data maintained with SteelMint reveals that both Chinese and Japanese FOB offers upped a mere 4% in the current month from February. Russian prices rose 11% to $770/t over $696/t in February.

It may be noted that the Indian HRC export index, which reflects Middle East and Vietnam prices, has been flat for some time. This is because, with the latter showing a pronounced propensity for Chinese and domestic HRCs for the last couple of months, the Indian export index has been predominantly capturing the Middle East graph where offers have been rather range-bound these past 2-3 weeks.

But, Indian HRC offers to the European Union have gone against the grain, rising with every successive deal. For instance, from say $675/t CNF Antwerp seen three months back, these have currently touched $830-835/t.

SteelMint also heard that Japan’s Nippon Steel, after having concluded April shipments, was now eyeing May HRC offers with a target for EU at $850/t CFR and for Asia, at $800/t CFR.

Japanese mills were busy catering to the domestic market for the past couple of months, and hence were rather quiet in terms of exports. But, on return, they are eyeing a hefty increase against the offers seen in January, buoyed by a good number of enquiries.

“Sentiments are quite volatile in the short term. On the other hand, raw material costs remain high and margins need to be recovered looking at the historical price graph. Hence, the price increase for May shipments,” a source at a Japanese mill disclosed to SteelMint.

Why did export offers rise in March?

Global export offers rose as major mills globally opted to raise prices in their domestic market. In China, on 13 March, Baosteel hiked HRC prices by RMB 200/t ($29/t) for April sales while Shagang Steel raised rebar prices by RMB 50/t (7/t) for mid-March sales. A couple of days later, on 15 March, Vietnamese steel major Formosa Ha Tinh also increased HRC prices by $33/t m-o-m for May shipments.

But, are prices again showing a downtrend?

But the immediate past has thrown up a different story. Prices across key exporting countries China and India have actually remained flat or fallen w-o-w. For instance, Imported Chinese-origin hot-rolled coil (HRC) offers into Vietnam dropped by $10-20/tonne (t) w-o-w, while SteelMint’s HRC export index (for Vietnam & ME), FoB East Coast, have fallen $4/t to $712/t.

There could be a possibility that, just as mills were breathing easy, prices may do an about-turn because of the following factors:

- Global banking turmoil impacts sentiments: The turmoil seen in the global banking space has had an impact, dragging down sentiments and prices. Silvergate Bank, known for handling crypto currencies, recently announced its closing “In light of recent industry and regulatory developments” much to the concern of its depositors. In the United States, two weeks back, Silicon Valley Bank and Signature Bank, collapsed suddenly over a span of three days, taking the global banking community by surprise. In Europe, globally acclaimed Zurich-based Credit Suisse sent further shockwaves as it buckled over, followed by its quick takeover by rival UBS.

In tandem, Chinese HRC export offers have recently fallen by $10-20/t, shaken by the global financial instability.

- Iron ore prices drop: Iron ore fines Fe 62% prices, CFR China, have increased by $3/t on a m-o-m basis to $129/t in March but a closer look at last week reveals a w-o-w drop of $8/t. China’s imported spot iron ore fines inched down w-o-w from $133/t CNF Rizhao to the current $125/t.

- NDRC crackdown: Another reason for the drop in China’s imported iron ore as well as finished steel prices was the crackdown by the National Development & Reform Commission, the key authority that implements the Central Committee’s policies and decisions.

NDRC said the rising prices were driven by speculation and suggested stronger market supervision.

- Tangshan pollution curbs: That apart, Tangshan, China’s main steel hub, announced a second round of level 2 pollution control measures. Such an emergency action inevitably involves steel mills’ production curbs. This is the second time in a fortnight that Tangshan has taken such an emergency decision.

- Coking coal prices fall w-o-w: Coking coal prices have fallen w-o-w, by around $23/t FoB, triggered by a few factors. One, the heavy rains in January in Australia resulted in huge cargo backlogs, but which normalized in February. This led to easing of supply and a consequent price drop. Two, Chinese and India buyers resisted the high price levels seen in February – Australian Premium HCC FoB Haypoint ruled at $379/t a month back. These have currently settled at a lower $338/t.

Outlook

The global financial crisis has spooked markets and put them in a wait-and-watch mode.

Sentiments are bleak and there is uncertainty over how inflation and high interest rates will affect global economies. There are liquidity worries too.

Moreover, Turkey not looking too strong. Its steelmakers have postponed scrap import decisions. Both buyers and sellers are waiting and watching. Mills are trying to push down the prices as demand has become tepid. Enquiries for billets have also slowed down, with more than a month having passed since the earthquake.

Sentiments in the short term may thus remain volatile.

Leave a Reply