- China’s steel production up 0.4% y-o-y in 4MCY’25

- India’s crude steel production rises 7% y-o-y on robust demand

- Japan, South Korea hit by economic contraction, trade uncertainties

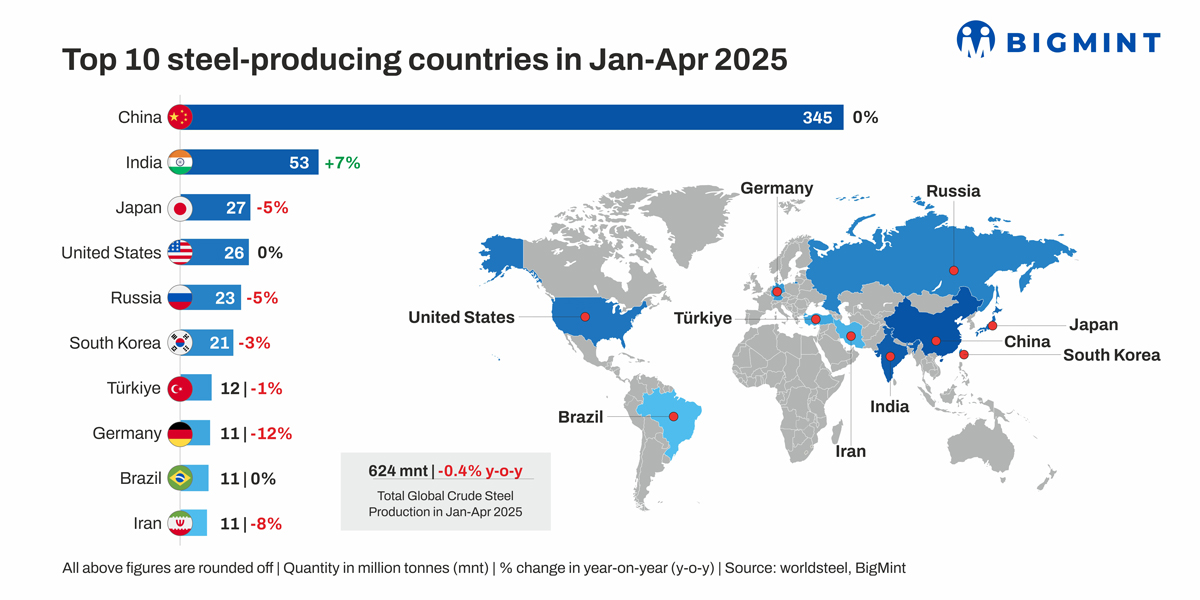

Morning Brief: Global steel production reached 624.4 million tonnes (mnt) in January-April 2025, a marginal decline of 0.4% y-o-y, as per the World Steel Association’s (WSA) recent report for April. The 69 countries that report to WSA accounted for 98% of global crude steel production in CY’24.

In April, global production stood at 155.7 mnt, a 0.3% decrease compared to April 2024. In CY’24, world crude steel output had declined by 0.8% to 1,882.6 mnt, as per WSA data. Therefore, the declining trend is continuing even as the tariff war plays out on the global stage and trade uncertainty grips the market.

The top crude steel producing countries in January-April (4MCY’25) were:

China was the leading producer of crude steel, with total output recorded at 345.4 mnt in January-April, up 0.4%y-o-y. Despite the government’s recommendation of a reduction in crude steel output, actual reductions are yet to be seen. By most predictions, steel consumption in China is set for a marginal decline in CY’25 as the downtrend in the property sector and partial slowdown in infra construction will not be totally compensated for by the growth in steel demand from the engineering goods, shipbuilding, appliances and NEV sectors.

According to an IREPAS report published in March, “it would have been great if the Chinese government reduced production as they did in 2015-16, but, since the economic situation in China is getting more and more difficult, exports are becoming increasingly important … They may simply not be in a position to enforce the production reductions on local governments and individual steel mills.”

India was the second-largest crude steel producer in 4MCY’25, with total output of 53.2 mnt, an increase of 7% y-o-y. While steel demand growth remains strong, the 12% provisional safeguard duty on flat steel imports is likely to boost market sentiment and capacity utilisation further.

The increasing steel intensity in infrastructure and construction and robust government spending on infrastructure are driving steel demand. However, de-growth in steel exports which is likely to impact the primary producers the most and softening prices due to global slowdown are the immediate headwinds.

Japan’s crude steel production contracted by 5.3% y-o-y in 4MCY’25 to 27 mnt. According to Japan’s Ministry of Economy, Trade, and Industry (METI), apart from the prevailing weakness in the construction sector, auto sector headwinds continue. Despite a recovery in automobile production, sales have remained sluggish. The lack of robust domestic demand is contributing to the overall cautious outlook on steel production.

The softening of Asian markets due to increased steel exports from China has hit the Japanese steel industry as export demand has dampened, thereby impacting Japanese manufacturers.

The US recorded total production at 26.4 mnt in 4MCY’25, flat y-o-y, although April production fell marginally by 0.3% y-o-y. Analysts predict that US trade policies and tariff-related uncertainties are expected to affect downstream demand, with gradually mounting inflationary pressure weighing on steel demand.

Russia’s crude steel production decreased by 4.5% y-o-y to 23.4 mnt due to falling global steel prices and the decline in steel exports alongside an appreciating currency, drop in demand from domestic construction and energy sectors, and the weight of sanctions on the economy and industry.

South Korean crude steel production fell by over 3% y-o-y to 20.5 mnt in 4MCY’25. The major reasons were domestic demand slump, typical to matured economies, diminishing cost-competitiveness of key steel producers such as POSCO, downtrend in the export market amid US tariffs and soft global demand, as well as a high level of steel exports from China.

Crude steel production in Turkiye decreased by 1% y-o-y to 12.3 mnt in 4MCY’25 but increased by 7% m-o-m to 3 mnt following a 7% growth recorded in March. Apart from infrastructure growth momentum, including the recovery of regions after the earthquake, export-led growth is also a prospect; however, trade uncertainties, competition from Asian counties and cost pressure due to increasing energy prices are weighing on steel production.

Crude steel production in Germany dropped sharply by 12% y-o-y in 4MCY’25 on continued downturn in the manufacturing sector, throughout the EU in fact, high energy prices, as well as high steel imports. The US tariffs are likely to complicate the situation further. The new safeguard measures in the EU will surely force some of the countries exporting to the region to slow down. A gradual uptick in the auto sector is also likely to push steel demand, as per industry predictions.

While Brazil’s output fell marginally by 0.3% y-o-y to 11 mnt in 4MCY’25 on weaker domestic demand amid industrial slowdown in the key markets of South America amid currency fluctuations, Iran witnessed crude steel output declining by 8% to 10.6 mnt during the review period. However, production increased by 4.6% m-o-m in April. Economic sanctions, energy supply issues and raw material crunch weighed on steel production.

Outlook

The WSA suspended its April bi-yearly global industry outlook due to the uncertainty triggered by the US tariffs and trade war. Crude steel production in CY’25 may witness a deeper decline than in CY’24 if China implements production cuts, and high inflation and economic contraction induced by trade uncertainties hit the advanced economies such as Japan, the US and South Korea.

However, in the short term, May crude steel production may inch higher than April on improving steel spreads in China after the May Day holidays, although overcapacity restricts long-term price growth prospects.

Leave a Reply