- Tighter global balance sheet shifts trade focus to Asia

- Bangladesh’s EU duty advantage offsets macro headwinds

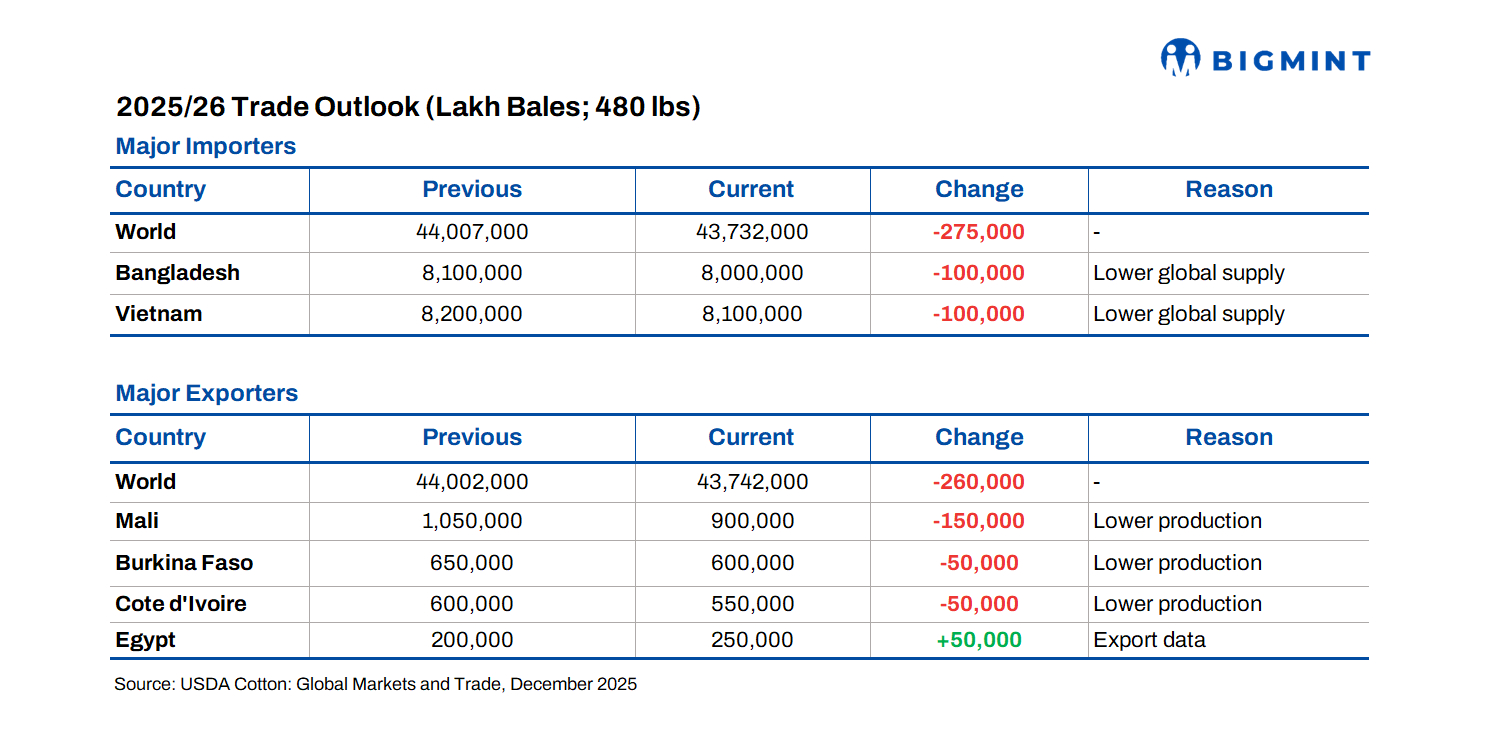

The global cotton market heads into 2026 with a marginally tighter balance sheet and a decisive shift in import demand toward Asia’s textile hubs. The USDA’s December 2025 Cotton: World Markets and Trade report shows world stocks edging up even as consumption weakens, underscoring a market weighed down by softer mill demand and widening regional disparities.

For a decade, China and Bangladesh have traded places as the world’s top cotton importer, with China’s ranking often determined by state-reserve buying. The pattern broke in 2024/25 when Bangladesh surged to 8.05 million bales, supported by a post-pandemic rebound in garment production. Vietnam followed within 100,000 bales, while China slipped to 5.19 million as rising domestic output reduced its need for foreign fibre.

Vietnam set to take the top spot

The 2025/26 projections now place Vietnam marginally ahead of Bangladesh as the world’s largest cotton buyer, though both forecasts were trimmed due to tighter global supply. Vietnam’s spinning sector, heavily reliant on imported fibre, has sustained high utilisation rates, allowing the country to overtake its long-time rival despite macro-sector headwinds.

Bangladesh retains a structural advantage through duty-free access to the European Union until 2029, a benefit that keeps its yarn and textile exports price-competitive even amid foreign-currency shortages, political volatility, and unreliable energy supply. But its ability to defend market share in 2025/26 will be tested by cost pressures and shrinking global apparel orders.

Thailand benefits from price stability, policy clarity

Thai export quotes remained broadly stable across Southeast Asia. Thai 5% traded in the $535–550/t band through 2024-25, maintaining a competitive edge. Premium Thai Fragrant 100% consistently cleared above $1,000/t, consolidating Thailand’s position among high-value import markets. Thai A1 Super and Thai 25% hovered near $394–395/t in 2025, offering a value proposition for buyers seeking predictability during periods of tight Indian policy.

Supply gains in the U.S. offset West African declines

World production for 2025/26 is expected to fall by more than 300,000 bales to 119.8 million, as smaller crops in Mali and West Africa outweigh a larger U.S. harvest. Global trade is set to contract by a similar volume, reflecting a subdued demand environment.

Consumption is projected at 118.6 million bales, dragged down by weaker mill activity in Brazil, the United States and parts of Central America. U.S. mill use is expected to hit 1.6 million bales — the lowest in nearly 150 years — highlighting the industry’s long-term shift toward Asian processing hubs.

Even with a tighter supply-demand setup, global ending stocks are forecast slightly higher at 76 million bales due to inventory accumulation in the United States and Brazil. The heavier carryover has softened prices: the U.S. season-average farm price is pegged at 60 cents per pound, while ICE futures have eased toward 64 cents.

Shifting trade routes deepen Asia’s reliance on a diversified supplier base

Export flows are undergoing a noticeable reconfiguration. Mali is expected to post the steepest decline with a 150,000-bale drop in shipments, while Burkina Faso and Côte d’Ivoire each cut exports by 50,000 bales. The pullback is a setback for West Africa, a key origin for Bangladesh, which sourced 41% of its imports from the region in 2024/25, alongside 25% from Brazil and 15% from India. The United States accounted for only 7% of the highly price-sensitive Bangladesh market.

Egypt, however, is forecast to raise shipments by 50,000 bales, partially offsetting West Africa’s downturn and offering Asian mills an alternative origin as they navigate higher freight, tighter supply and volatile yarn demand.

Leave a Reply