- Trade activity rises despite weak ICE prices

- Tighter output outlook narrows global surplus ahead

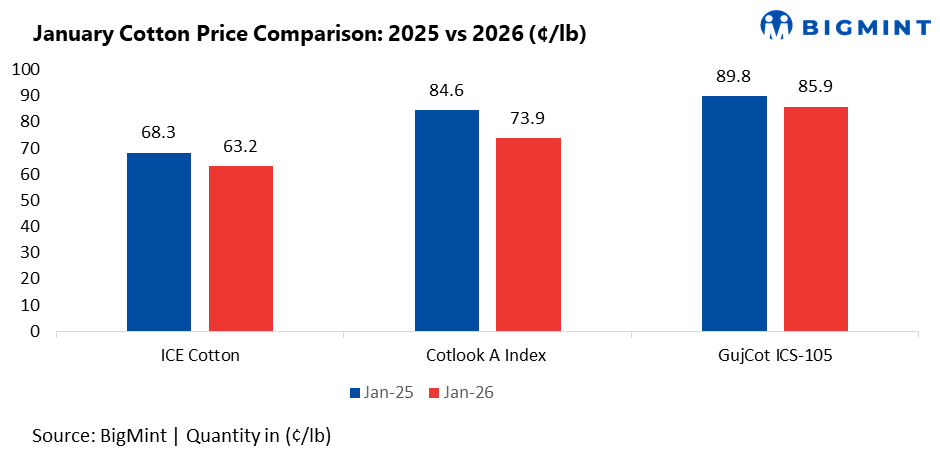

Global cotton prices eased modestly in January. The Cotlook A Index ended the month at 73.95 cents/lb, while ICE New York futures remained under pressure, with the March contract falling 110 points m-o-m to 63.17 cents/lb and touching a life-of-contract low of 62.97 cents on January 26. Despite softer futures, physical trade stayed active. Shippers lifted basis levels – particularly for Brazilian cotton – and pricing progressively rolled from March-to-May based quotations. Daily volumes were firm and open interest climbed to a record 373,415 contracts, signalling strong participation from both commercial and speculative players even at depressed price levels.

Import demand improved across several key consuming regions, led by China in the first half of the month. Buying was supported by a wide ZCE-ICE spread and fresh Tariff-Rated Quota allocations, with purchases focused on Brazilian and US origins. Yarn demand also strengthened for both domestic and imported supplies, lending price support and modestly improving spinning margins, which encouraged replenishment.

Pakistan increased its reliance on imports as domestic availability tightened, covering second-quarter requirements with competitively priced lots and replacement cargoes from multiple origins. Indian mills continued to show interest despite the re-imposition of the 11% import duty, as local cotton remained above international parity. In Bangladesh, demand for African and Brazilian cotton was intermittent, with buying restrained ahead of the February 12 general elections and uncertainty over policy measures on duty-free yarn imports, although immediate shutdown risks eased following government assurances.

On the supply side, US upland export commitments strengthened sharply, with net sales of 955,800 running bales over three weeks to January 22. While cumulative commitments of 7.55 million bales still trailed last year’s pace, shipments improved steadily and reached a marketing-year high. USDA lowered US production to 13.92 million bales and cut ending stocks to 4.2 million bales. Globally, output was reduced to 119.43 million bales as cuts for India, the US, Argentina and Turkey outweighed a higher estimate for China, while consumption forecasts were raised, tightening projected stocks.

In India, arrivals slowed seasonally, with the Cotton Corporation of India procuring around 4.4 million tonnes of seed cotton, roughly 30% of expected output, and auctions from the new crop already underway, with over 300,000 bales sold. In the Southern Hemisphere, Brazilian planting advanced quickly, while Australian output prospects remained subdued due to reduced area and water constraints.

Looking ahead, global balances are tightening. Cotton Outlook now projects the 2025/26 production surplus at 841,000 tonnes, down from 970,000 previously. While weak futures may continue to cap near-term sentiment, firmer trade flows, improving mill demand and lower output estimates suggest the downside is increasingly limited, with prices likely to stabilise as the supply cushion narrows through the season.

Leave a Reply