- Global cotton production falls 6.6 million bales year on year

- India’s import demand jumps 25% as mill consumption outpaces output

The sharp correction in global cotton prices is increasingly being viewed by traders as a disconnect from underlying market fundamentals, with India emerging as the key factor reshaping global trade flows in the 2026/27 season. While ICE cotton futures have fallen nearly 17% over the past month to around 66 cents/lb, the global balance sheet is pointing toward a tighter supply environment, driven by declining production, rising consumption, and growing import demand from India.

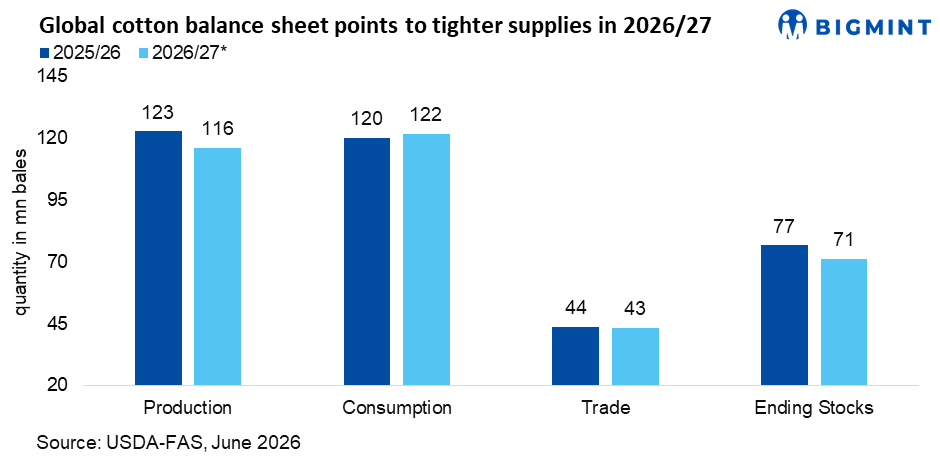

According to the latest USDA outlook, global cotton production is forecast at 116 million bales in 2026/27, down 6.6 million bales from the previous season, while consumption is expected to rise to 121.8 million bales. The resulting supply deficit of nearly 6 million bales is projected to reduce global ending stocks to 71.1 million bales, more than 5.5 million bales below the previous year’s level.

India becomes the market’s balancing buyer

At the centre of this shift is India, where USDA raised its cotton import forecast by 500,000 bales to 2.5 million bales after the government temporarily removed import duty through October. The revision represents a 25% increase from the previous estimate and makes India the largest source of incremental import demand globally, offsetting weaker buying from Bangladesh and Pakistan.

The development is significant because India remains the world’s second-largest cotton producer. However, domestic fundamentals have tightened considerably. Production is forecast at 24 million bales in 2026/27, while mill consumption is expected to reach 26 million bales, extending the country’s structural supply deficit for another season.

Traders said the gap between domestic demand and production is encouraging mills to secure imported fibre, particularly as lower international prices improve import parity. Brazilian and U.S. cotton have become increasingly attractive to Indian buyers, especially for export-oriented spinning mills seeking quality consistency and competitive raw material costs.

“India is becoming the buyer that global exporters are watching most closely,” a Mumbai-based trader said. “The market is focusing on weak textile sentiment, but the bigger story is that consumption continues to exceed production across several key markets.”

Tightening supplies across major origins

The tightening global picture extends beyond India. U.S. cotton production is forecast to decline to 13.3 million bales from 13.9 million bales a year earlier, while Brazil’s output is expected to retreat from a record 19.5 million bales to 17.5 million bales. Australia’s crop is projected to fall sharply by one-third to 3 million bales. Together, these reductions are removing a substantial volume of exportable supplies from the global market.

Meanwhile, global consumption continues to show resilience, led by China, India, Vietnam and Uzbekistan, where textile processing demand remains firm despite ongoing macroeconomic uncertainty.

Outlook

Market participants believe the recent price decline may ultimately stimulate additional buying rather than trigger a prolonged bearish trend. With global consumption expected to exceed production for a second consecutive season and inventories trending lower, India’s return as a major importer could provide a floor to international prices in the months ahead.

For traders, the key takeaway is that the cotton market is increasingly shifting from a story of weak demand to one of tightening availability. If Indian mills continue to capitalize on lower prices and the duty-free import window

Leave a Reply