- USDA trims global output, ending stocks for 2025-26 season

- Price rallies may face resistance amid stable global demand

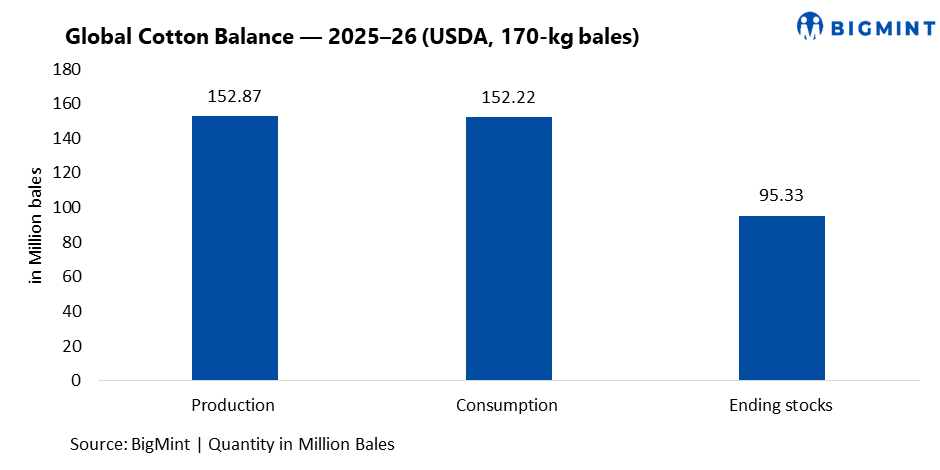

Global cotton fundamentals tightened modestly in January 2026, as per USDA WASDE data, but the overall balance still points to a stable market rather than a supply-led rally. For the 2025-26 season, world cotton production was estimated lower at around 116.0 million bales, while global consumption is projected slightly higher at about 117.0 million bales. Amid consumption marginally exceeding production, world ending stocks were estimated lower, though they remain comfortable at nearly 95.3 million bales, keeping the global stock-to-use ratio close to 46%, a level that limits strong bullish sentiment.

The marginal tightening is largely supply-driven. The US cotton crop for 2025-26 is projected at about 17.8 million bales, lower y-o-y, while ending stocks are estimated at around 5.4 million bales. This brings the US stock-to-use ratio down to nearly 31%, providing some underlying support to Intercontinental Exchange (ICE) cotton prices.

However, this tightening is being partially offset by strong output from key Southern Hemisphere exporters. Brazil’s production is projected at around 24.0 million bales, with exports close to 18.6 million bales, while Australia’s output also remains robust, ensuring steady global export availability and preventing any sharp tightening in trade flows.

Demand continues to be the weak link in the cotton balance sheet. Global cotton consumption is rising only marginally, reflecting cautious buying behaviour by spinning millers amid weak yarn demand, slow downstream textile orders, and continued margin pressure. Global cotton trade is projected at around 43.8 million bales, broadly stable y-o-y, reinforcing the view that mills are buying on a hand-to-mouth basis rather than building forward inventories.

India remains the key stabilising factor in the global cotton market. For 2025-26, India’s cotton production is projected at around 30.1 million bales, while domestic consumption is estimated at about 32.0 million bales. Despite consumption exceeding production, ending stocks are still projected at around 11.9 million bales, translating into a stock-to-use ratio of nearly 35%, one of the highest among major cotton-producing countries. This large inventory base continues to cap any sharp upside in domestic prices, even as global fundamentals show mild tightening.

What may happen next is continued range-bound price action. International prices may remain supported by lower US and global ending stocks, but without a meaningful pick-up in global consumption, rallies are likely to face resistance. In India, steady buying from spinning millers and ongoing procurement are expected to provide a price floor, but comfortable stocks will likely limit sharp price increases. For ginners, sales are expected to remain steady but quality-selective. Spinning millers are likely to continue need-based buying, while brokers should focus on quality differentials and import parity rather than positioning for a strong bullish shift in the near term.

Leave a Reply