- Mine production declines 1.4% on major supply disruptions

- Exchange copper inventories hit highest level since 2003

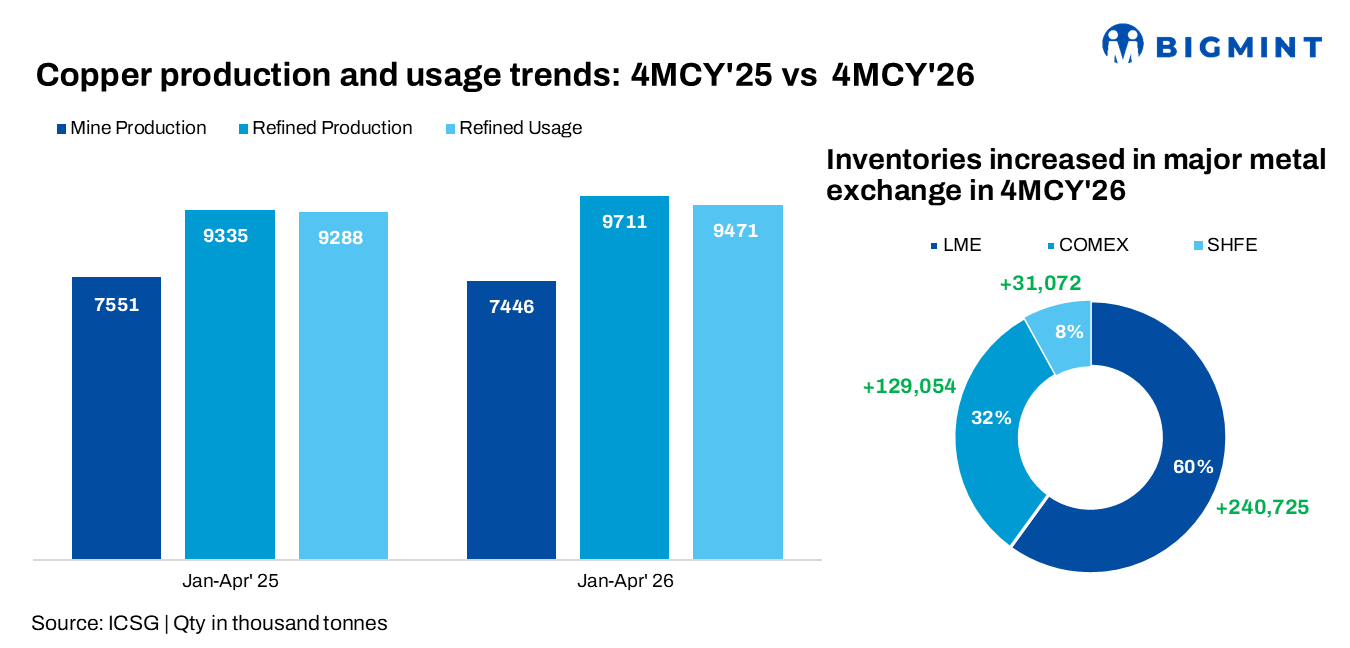

According to the International Copper Study Group (ICSG), global copper mine production declined by 1.4% y-o-y to 7.45 mnt during January-April’26 from 7.55 mnt in the corresponding period last year. On a monthly basis, mine production also eased by 3.6%, falling to 1.8 mnt in April from 1.9 mnt in March.

The decline in global mine production was primarily attributed to lower concentrate output, which fell 2.7%, outweighing a 3.5% increase in solvent extraction-electrowinning (SX-EW) production.

Major mines disruptions weigh on global supply

Indonesia remained the largest drag on global mine supply, with concentrate production plunging 40% due to continued constraints at the Grasberg mine following the September 2025 mud rush.

Chile’s mine output declined 7.9% as lower production from Candelaria, El Teniente, Escondida, Los Pelambres and Spence outweighed gains at Collahuasi, Anglo Sur and Quebrada Blanca.

However, downstream refined copper production remained resilient as mine production in DRC remained stable as an 8.5% increase in SX-EW output offset a 33% decline in concentrate production following the seismic event at the Kamoa mine.

Peru recorded a 3.6% increase in mine production, driven by higher output from Antamina, Las Bambas and Antapaccay, while Mongolia’s concentrate production surged 29% on the back of the continued ramp-up of the Oyu Tolgoi underground project.

Refined copper output expands

Despite weaker mine supply, global refined copper production increased 4% y-o-y to 9.7 mnt during 4MCY’26 compared with 9.3 mnt a year earlier. However, refined output moderated on a monthly basis, declining 6% to 2.4 mnt in April from 2.6 mnt in March.

Among major producing countries, China and the DRC, together accounting for nearly 60% of global refined copper output, recorded combined production growth of 7.6%, with China rising 7.4% and the DRC 8.4%.

In contrast, Chile’s refined copper production declined 11%, mainly due to smelter maintenance and operational constraints that reduced electrolytic output by 26%.

Production across Asia excluding China fell 1.3%, primarily because of lower output in Japan, Indonesia and the Philippines.

India stood out as one of the fastest-growing producers, with refined copper production surging 28%, driven by improved operating rates and the ongoing ramp-up of the Adani copper refinery.

Copper market records wider surplus

Global refined copper usage increased 2% in 4MCY’26, with consumption outside China growing 1.4%, while China’s apparent demand rose 2.4% despite a 25% decline in net refined copper imports. Based on these trends, the global refined copper market recorded an apparent surplus of 0.24 mnt during the first four months of the year, significantly higher than the 47,000 t surplus reported during the same period in 2025.

Copper inventories continued to build across the major exchanges where combined stocks held at the LME, COMEX and SHFE reached 1.15 mnt at the end of May 2026, marking the highest level since January 2003. Inventories increased by 400,851 t, or 54%, compared with end-2025 levels, with stock builds observed across all exchanges—LME (+240,725 t), SHFE (+31,072 t), and COMEX (+129,054 t), highlighting continued accumulation of material amid subdued demand conditions.

Copper prices remain firm despite rising exchange stocks

Copper prices remained elevated amid tight mine supply and continued optimism surrounding long-term demand fundamentals. The average LME cash copper price increased 4.8% m-o-m to US$13,507.13/t in May from US$12,891.38/t in April. Although rising exchange inventories point to improving short-term metal availability, ongoing mine disruptions in Chile, Indonesia and the DRC, together with geopolitical uncertainties and expectations of sustained demand from the energy transition, electric vehicles and power infrastructure sectors, continued to underpin market sentiment.

Market outlook

Looking ahead, the global copper market is expected to remain balanced but vulnerable to supply-side risks. While expanding refined copper production, particularly in China and India, is likely to remain supported by capacity expansions and higher secondary output, mine supply recovery could continue to face headwinds.

Copper prices are expected to remain well supported as structural demand from renewable energy, electric vehicles, power grid expansion and data center investments continues to strengthen. Going forward, market sentiments will majorly depend on mine recovery rates, Chinese consumption trends, inventory movements and geopolitical developments, which are likely to determine the direction of copper prices and the overall market balance in the coming months.

Leave a Reply