- Smelting overcapacity in China intensifies global concentrate imbalance.

- Global concentrate deficit expected in 2026 despite refined surplus.

The global copper market is witnessing a imbalance, as tightening concentrate supply struggles to keep pace with rapidly expanding smelting capacity.

With copper concentrate availability tightening sharply over the past 12-18 months. This has led to an unprecedented collapse in treatment and refining charges (TC/RCs), which have fallen to zero and even negative levels in the spot market. The ongoing imbalance reflects a deeper shift in the copper value chain, where constrained mine supply is colliding with aggressive smelting capacity expansion, particularly in Asia.

Global trade overview

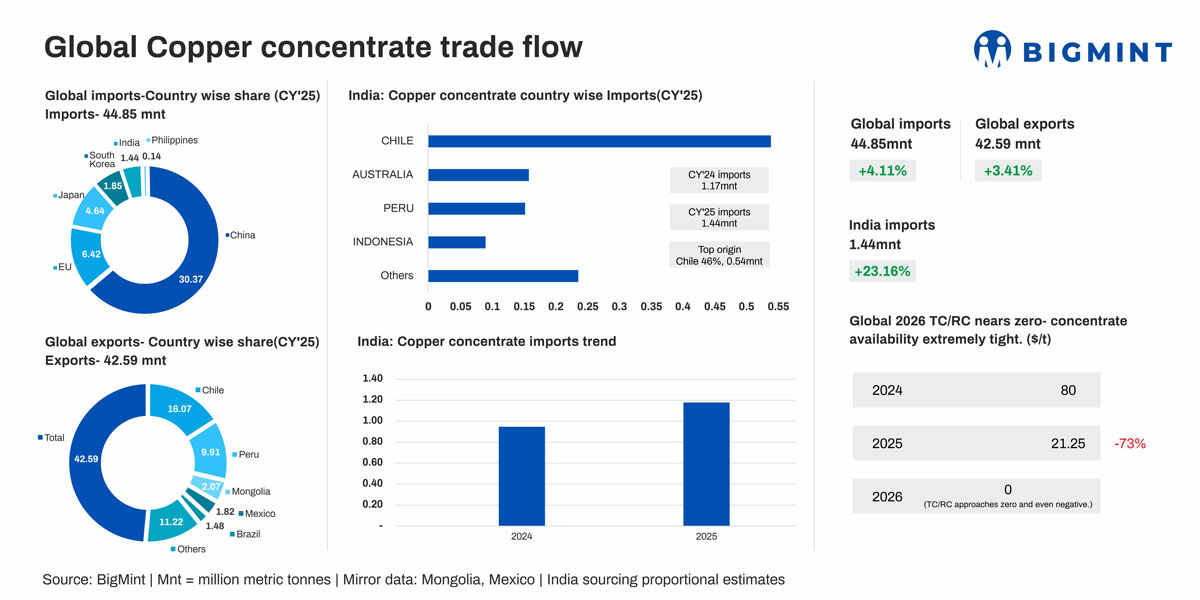

As per BigMint data, Global copper concentrate trade (43-45 mnt) is being increasingly shaped not just by mine output but also by smelter expansions and disruptions. On the import side, China continues to dominate with over 30 mnt (+7.8% y-o-y), driven by aggressive smelter capacity additions expected to reach 16-17 mt by 2025-27. However, this rapid expansion has backfired-TC/RCs have turned negative, forcing authorities to halt 2 mt of new smelter projects and consider output cuts.

India imports surged (+23%) due to new capacity additions and structural dependence following the closure of Sterlite. In contrast, Japan saw declining demand amid plans to shut the Onahama smelter by 2027.

On the export side, Chile and Peru remain dominant, while exports from Indonesia (-40.9%) declined sharply due to policies promoting domestic smelting. Supply disruptions in Democratic Republic of the Congo and Latin America further tightened availability.

How did LME Prices perform?

Copper prices have jumped from $9,270 per tonne in 2024 to $10,500 per tonne in 2025, up about 13%. This rise is mainly due to tight supply, strong demand from smelters, and disruptions in key producing countries.

What is driving the copper concentrate shortage?

The tightening of copper concentrate supply is the result of multiple structural and operational factors across key mining regions. In Chile, declining ore grades and ageing mines continue to weigh on output.

In the Democratic Republic of the Congo, disruptions such as seismic activity at Kamoa-Kakula have intermittently impacted production. Latin America has also faced setbacks, with major miners revising production guidance downward due to operational challenges and project delays.

Although some growth is expected, including a projected 17% increase from Antofagasta plc in 2026, these additions are unlikely to offset the broader supply shortfall. The limited pipeline of new projects and long development timelines continue to constrain global mine supply.

Why did TC/RCs collapse to zero despite rising concentrate imports?

Under balanced conditions, TC/RCs typically range between $60-80/t. However, in 2025, benchmark levels dropped to ~$20-25/t, while spot TC/RCs fell to zero and even negative levels.

In a landmark development, Antofagasta plc agreed to zero TC/RCs for 2026 with major Chinese smelters including Jiangxi Copper and Tongling Nonferrous Metals. In the spot market, TC/RCs plunged further to around -$40/t, effectively forcing smelters to pay miners to secure concentrate.

This reflects a fundamental imbalance—smelting capacity has expanded much faster than concentrate availability. Despite rising imports, particularly into China, the supply of feedstock has not kept pace, giving miners significant pricing power and inverting traditional pricing structures.

How has smelting overcapacity intensified the imbalance?

The most critical factor is the rapid expansion of smelting capacity, especially in China. Global capacity is expected to increase from ~26 mt in 2024 to ~30 mt by 2028.

China alone accounts for over 50% of global smelting capacity, far exceeding Japan (~7%). Large players such as Tongling Nonferrous Metals and Jiangxi Copper have significantly expanded output, pushing refined production to ~15 mt in 2025.

However, the crisis has forced coordinated action. China’s top smelters, under the China Smelters Purchase Team (CSPT), have:

Refused to accept negative TC/RC benchmarks

Announced potential >10% production cuts

Pressured for capacity rationalisation

Despite weak margins, many Chinese smelters continue operating at high utilisation rates, supported by by-product credits like sulphuric acid and downstream integration, further intensifying competition for concentrate.

What has been the global impact?

The impact of collapsing TC/RCs has been uneven. While Chinese smelters remain resilient, others are under significant pressure.

In Japan, Mitsubishi Materials plans to shut its Onahama smelter by 2027 due to margin pressure. JX Advanced Metals has also reduced output amid declining profitability.

In Australia, smelters have required support to sustain operations, while in the Philippines, facilities such as PASAR have faced shutdowns due to unviable economics under negative TC/RC conditions.

Demand trends remain mixed. Structural demand from electrification and renewables is strong, but near-term indicators such as weak manufacturing activity and declining premiums suggest softer consumption. Meanwhile, rising global inventories have added pressure on refined copper prices.

Global: Copper concentrate deficit to persist in 2026

As per ICSG, Copper concentrate supply is expected to remain tight into 2026. Refined demand is projected to grow 2.1%, while production may rise only 0.9%, shifting the market toward a deficit of 150,000 tonnes.

What lies ahead: Outlook on supply, capacity, and prices

Looking ahead, the market will remain structurally tight on the concentrate side. While refined copper may show a surplus (380,000 tonnes in 2025), this masks underlying raw material constraints.

Incremental mine supply is unlikely to match the pace of smelting expansion. At the same time, new smelters across Asia will continue to increase demand for concentrate, keeping TC/RCs under sustained pressure.

From a pricing perspective, the outlook remains constructive, supported by supply tightness and long-term demand. However, risks such as macroeconomic uncertainty, high inventories, and currency strength may create short-term volatility.

Iran isreal war had limited affect- Limited impact on concentrate market

The conflict has also had minimal direct effect on the global copper concentrate market.

Iran accounts for a relatively small share of global copper supply, and much of its concentrate production is processed domestically rather than exported. As a result, disruptions to Middle East shipping routes have not significantly altered the availability of concentrate on the seaborne market.

More broadly, any meaningful shift in copper supply would need to involve major producing regions such as Chile, Peru, China or the DRC, rather than the Middle East.

Recent developments such as the expected gradual restart of production at Indonesia’s Grasberg mine in the second quarter are expected to increase supply, but are unlikely to materially shift the balance of the concentrate market in the near term, particularly given the integrated nature of operations.

The collapse of TC/RCs to zero marks a shift in the copper market. Constrained mine supply, combined with aggressive smelting expansion-led by China-has fundamentally altered the industry balance.

Conclusion

Until significant mine supply additions materialise or smelting capacity is rationalised, the market is likely to remain in a tight concentrate, low TC/RC regime.

In this environment, miners-led by players like Antofagasta plc-retain pricing power, while smelters face sustained margin pressure, reshaping the economics of the global copper value chain.

Will emerging small- and mid-scale smelters in India, China, and Southeast Asia increase local concentrate demand and keep domestic prices elevated?

Leave a Reply