- Copper market seen in deficit in 2026 as demand outpaces supply.

- Zero TC/RC benchmark highlights severe concentrate tightness.

Copper concentrate supply is expected to remain structurally tight in 2026, as smelter demand continues to outpace mine supply, despite a slowdown in new smelting capacity additions, market participants said. Global copper demand is forecast to continue growing in 2026, with refined copper consumption projected to increase by around 2.1% year-on-year, following an expansion of approximately 3% in 2025 as industrial activity and electrification trends sustain usage growth. At the same time, global refined copper production is expected to rise only modestly, with output forecast to increase by about 0.9% in 2026 after a stronger 3.4% rise in 2025, according to the latest estimates from the International Copper Study Group (ICSG). This imbalance-higher consumption growth relative to supply expansion-contributes to expectations of a supply deficit of around 150,000 tonnes in 2026, turning the market from a projected surplus in 2025 to a deficit next year.

As per reports, China is expected to commission two new smelting projects next year with a combined capacity of around 400,000 t/y, significantly lower than the nearly 2 mnt/y of global smelting capacity added in 2025. However, concentrate demand is still projected to rise by around 1.4 mnt in 2026, driven by smelters that started operations this year and continue ramping up.

Several large blister copper projects came online in 2025, including 500,000 t/y units by Adani in India and Tongling Nonferrous in China. The Kamoa-Kakula smelter in the DRC also produced around 500,000 t/y of blister copper in November. Indonesia’s 300,000 t/y Manyar smelter resumed operations in May, while PT Amman’s 220,000 t/y smelter produced its first copper in January, though both units were shut in October following force majeure declarations.

China’s copper cathode output is expected to increase by around 550,000 t in 2026, slower than the estimated 1.16 mnt rise in 2025, reflecting moderation in smelting growth but still adding pressure on concentrate availability.

Mine supply outlook

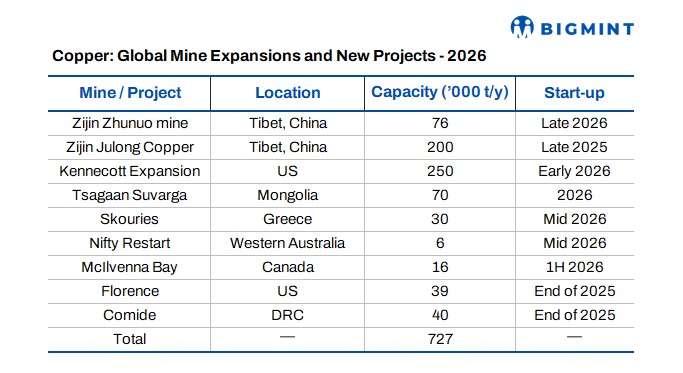

Global copper mine capacity additions are projected at around 730,000 t/y in 2026, down sharply from approximately 1.2 mnt/y this year.

In China, Zijin Mining is expected to ramp up the second phase of its Julong mine, lifting output to 300,000–350,000 t/y, up from 166,300 t in 2024, while production at the Zhunuo mine in Tibet is planned to rise to 76,000 t/y in 2026.

Outside China, Rio Tinto is progressing expansion work at its Kennecott mine in the US, which is expected to add 250,000 t/y of capacity from early 2026. Mongolia’s Tsagaan Suvarga mine is likely to begin production in 2026 with processing capacity of 158,000 t/y, while five other projects are expected to contribute a combined 130,000 t/y.

Meanwhile, Cobre Panama, which produced 331,000 t of copper in 2023, remains shut following its suspension in 2024, limiting global supply growth.

Market participants estimate global mine production could rise by around 700,000 t in 2026, but effective growth may be closer to 300,000 t, assuming a disruption rate of 5.5%.

Benchmark negotiations

Benchmark talks for Chile’s Antofagasta region copper concentrate supplies for 2026 were prolonged, reflecting tight market conditions.

Jiangxi Copper and Antofagasta reached a settlement on 19 December at $0/t TC and $0.0/lb RC for 2026 deliveries, sharply lower than the $21.25/t TC and 2.125¢/lb RC agreed for 2025.

Although annual benchmark terms are typically finalised during Asia Copper Week in late November, negotiations extended into mid-December due to wide gaps in pricing expectations. In the second round of talks, Antofagasta reportedly quoted a minimum TC of $7.50/t, while Jiangxi Copper bid at $11/t.

Some participants expressed concern that the benchmark settled at the lower end of the expected $0–5/t range, particularly after industry bodies warned that zero or negative TC/RCs could undermine the long-term viability of smelters.

In October, smelter cash margins were estimated at around $25/t, assuming half of production was priced at the 2025 benchmark TC and the remainder on spot terms.

Leave a Reply