*India re-emerges as top buyer

*Australian shipments dip on weather disruptions

*Russian exports increase by 50%

*China’s lifting of trade ban may drive up prices

Despite the slump in world crude steel production in 2022, global seaborne trade in coking coal remained strong with imports of met coal and PCI increasing by 8% y-o-y to around 320 million tonnes (mnt) from 295 mnt in 2021, as per provisional data maintained with CoalMint.

Leading importers

India was the leading coking coal importer at 69 mnt, accounting for 22% of total global imports. India’s imports were almost stable y-o-y compared to 2021. For Indian importers of coking coal there was no major change in the demand scenario. Demand did not fluctuate much since the steel export duty fiasco but remained generally steady. No major producer cut production sharply. In fact, steel production increased by around 9 mnt y-o-y in the April-December period.

China was the second-largest importer at 63 mnt. Imports by China rose 14% y-o-y, although crude steel production fell by 1.4% in January-November 2022, as per WSA data. Pandemic restrictions impeded the movement of domestic scrap for steelmaking, thereby impacting EAF steel production. Higher shipments by Russia and Mongolia also account for higher imports by China. Mongolian shipments doubled y-o-y in 2022 as COVID-related restrictions were eased enabling truck movement across the border, while Russian cargoes were available at much cheaper rates since sanctions against Russia came into force in August.

Imports by Japan and South Korea remained largely stable y-o-y at 42 mnt and 22 mnt, respectively. Sentiments remained largely bearish on a gloomy global steel export outlook amid high inflation, supply chain problems in the auto industry and natural disasters.

Europe’s coking coal imports fell by 21% y-o-y due to high energy inflation affecting steel production and demand following the outbreak of the Russia-Ukraine conflict. After Europe imposed a complete ban on Russian coal imports from 10 August global trade flows altered. The EU traditionally sourced 55-60% of its coking coal requirement from Russia and Australian and US coking coal made their way into the continent.

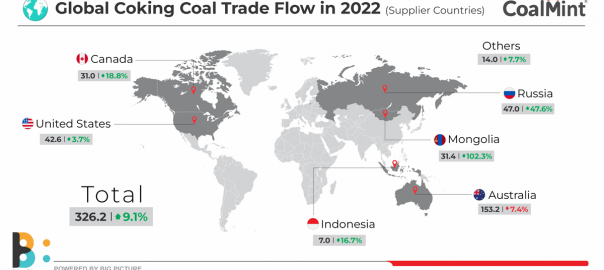

Top exporters

Australia was the largest coking coal exporter in CY22, although its share in global exports fell by 8% compared to 2021 due to bad weather. The La Nina event in the country led to heavy rains in the mining regions which affected operations, leading to supply disruptions. In addition, strikes by mine workers and unavailability of labour weighed on production. The US and Canada emerged as an alternative to Australian coal due to supply disruptions.

Russia emerged as the second largest exporter with 47 mnt, an increase of 48% y-o-y. After sanctions were imposed by the European countries on Russia following its invasion of Ukraine, the country started exporting coal at cheaper prices to Asian countries like China and India, resulting in a hike in export volumes.

It may be mentioned that India imported 2.77 mnt of Russian coking coal in 2022, up 141% on-year, while China imported 21 mnt, an increase of 90% y-o-y.

The war between Russia and Ukraine affected seaborne trade dynamics of metallurgical coal. As more Russian coal found its way into China and India, Japan and South Korea reduced sourcing of Russian coal in response to Western sanctions.

Outlook

Coking coal imports by India from Australia are expected to remain stable in 2023, with the FTA between the countries leading to duty-free inflow of coal. Prices remained strong after a bumper 2022, driven largely by global energy prices and shortages cause by the Russia-Ukraine war. The other big-ticket item in January was the news that China is set to end its unofficial ban on importing coal from Australia, which is largely positive for global met coal prices.

Three central government-backed utilities and China’s top steelmaker would be allowed to resume imports. A recent report in the Australian Financial Review also indicates that Australian met coal imports might displace lower quality and higher cost Chinese domestic or US met coal, particularly for Chinese steelmakers in the southern region. Note that China’s proposed import duty on coal leaves Australia and Indonesia unaffected.

Australia had diversified its coal exports to non-traditional buyers and ramped up supplies to traditional ones in the absence of China from the seaborne market. But now that Chinese inquiries are expected to rise post the Spring Festival holidays there could well be a dearth of cargoes for other buyers, thereby pushing prices higher.

On the other hand, bad weather in Australia could constrain supplies from the eastern ports, particularly Newcastle, as per latest reports. Tight spot supplies may drive up coking coal prices in the near term, CoalMint understands.

How will coking coal trade dynamics in Asia change now that China has lifted the embargo on Australian coal? Will tight seaborne spot supplies drive up prices again? How will steel demand and met coal trade in Asia pan out till 2025? To follow the discussion book your seat at CoalMint’s 2nd Asia Coal Trade Summit to be held in Bangkok, Thailand from 24-25 April, 2023 .

Leave a Reply