- Coal exports fall 9% w-o-w on post-holiday slowdown

- Weak freights and thin fixing weigh on shipments

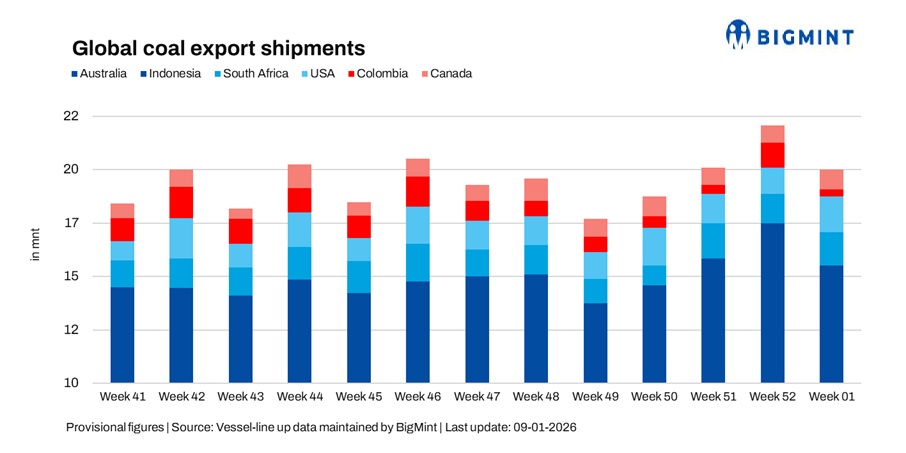

Global seaborne coal exports declined 9.4% w-o-w to 19.59 million tonnes (mnt) hitting in week 1 of 2026 (27 December-2 January), down from 21.62 mnt in week 52, according to BigMint’s vessel line-up data. The drop reflected a post year-end slowdown, with lower shipments from Australia, Indonesia, and Colombia outweighing modest recoveries from South Africa, the US, and Canada.

The week’s performance marked a clear reversal from the strong year-end push seen in week 52. With the holiday period extending into early January, cargo nominations slowed, execution of deferred shipments eased, and chartering activity remained cautious. While port operations stayed largely stable, the absence of fresh demand signals and weak freight sentiment limited exporters’ willingness to push volumes aggressively, resulting in a softer start to CY’26.

Country-wise trends

Australian exports retreat after strong Dec’25

Australia’s coal exports fell 13.4% w-o-w to 7.69 mnt in week 1, down from 8.88 mnt the previous week. The decline reflected the natural unwinding of year-end shipment momentum, as exporters scaled back loadings following an aggressive December dispatch cycle. Reduced cargo stem issuance and extended holiday disruptions weighed on volumes, despite stable port operations.

Major east coast terminals continued to function smoothly, though the slowdown highlighted the lack of immediate demand-side pull. Newcastle remained the leading load port, handling 3.30 mnt, followed by DBCT at 1.57 mnt and Gladstone at 1.36 mnt, reflecting steady but lower throughput across key terminals. Yancoal led shipments with 0.75 mnt, followed by BHP at 0.64 mnt and Glencore at 0.57 mnt, underscoring the supply-led nature of exports during the week.

On the demand side, buying interest from Asia remained selective, with Japan emerging as the largest destination at 2.59 mnt, followed by China at 1.95 mnt and Taiwan at 0.55 mnt. Comfortable inventories and weak downstream margins continued to limit fresh procurement, keeping Australian exports supply-constrained despite smooth terminal operations. Notably, strong December shipments from ports such as Gladstone contrasted with the week 1 slowdown, while forecasts still point to modest growth in Australia’s metallurgical coal exports in 2026 despite softer Chinese demand.

Indonesian volumes ease on cautious demand

Indonesia’s coal exports declined 8.7% w-o-w to 7.58 mnt in week 1, down from 8.31 mnt in week 52. The pullback followed the clearance of delayed cargoes in late December, with shipment flows normalising as the calendar turned. While operational performance remained steady across key loading areas, exporters faced limited incentive to accelerate shipments amid subdued buying interest. Taboneo emerged as the leading load port, handling 1.22 mnt, followed by Samarinda at 0.96 mnt, while Balikpapan and Bunati jointly loaded 0.74 mnt, reflecting stable but moderated throughput across Indonesia’s key export hubs.

On the demand side, India remained the largest destination, importing 1.88 mnt, followed by China at 1.62 mnt, with northeast Asian markets continuing to feature prominently. However, procurement remained measured due to soft pricing signals and weak freight economics. As a result, Indonesian exports stayed sensitive to near-term demand fluctuations, reinforcing a cautious shipment outlook at the start of the year.

Recent logistical disruptions to coal barging on the Lalan River in South Sumatra have also constrained early-year cargo flows, while ongoing policy uncertainty around proposed export taxes and production quotas continues to temper producer shipment planning amid generally weaker export demand from China and India.

South African exports recover modestly

South Africa’s coal exports rose 13.7% w-o-w to 1.48 mnt in week 1, up from 1.30 mnt in week 52. The increase reflected a partial recovery following the previous week’s pullback, supported by steady operations at Richards Bay, from where all shipments originated. The rebound was largely logistical rather than demand-driven, as exporters executed scheduled cargoes rather than responding to fresh buying interest.

On the demand side, India remained the primary destination, importing 0.62 mnt, though buying interest stayed selective amid soft freight conditions and a subdued import appetite. Despite the week-on-week improvement, overall volumes remained below potential, underscoring continued demand-side constraints and limited follow-through demand from the Atlantic basin.

South African exporters have also been diversifying their destination base, with increased shipments to markets such as Israel following the suspension of Colombian supplies, providing some support to outbound tonnage despite broader demand constraints.

Colombian shipments fall sharply

Colombia’s coal exports declined 71% w-o-w to 0.32 mnt in week 1, down from 1.10 mnt in the previous week. The sharp drop followed the execution of pent-up and delayed cargoes in Week 52, with shipments reverting to subdued levels as logistical catch-up faded. Export activity remained concentrated at key terminals, led by Puerto Bolivar, which handled 0.16 mnt, followed by Puerto Brisa at 0.06 mnt, highlighting the narrow base of shipment flows during the week.

Cerrejon Mines emerged as the leading shipper with 0.16 mnt, underscoring the supply-driven nature of exports.Weak European demand and limited flexibility to redirect cargoes continued to constrain volumes, reinforcing the fragile nature of Colombia’s export recovery amid persistent Atlantic market weakness.

Colombia’s broader export landscape has been under pressure, with total coal and coke shipments declining significantly in 2025 amid weak global demand and a continued retreat of European coal imports, reinforcing the subdued shipment backdrop seen in week 01.

US exports rebound

US coal exports rose 30.2% w-o-w to 1.58 mnt in week 1, up from 1.21 mnt in week 52, supported by the execution of scheduled cargoes and improved follow-through demand after a softer end to December. Loadings across major terminals improved, reflecting steady operational performance rather than a broad-based demand recovery.

Mobile led export activity during the week, handling 0.59 mnt, followed by Norfolk at 0.52 mnt, indicating improved throughput at key US load ports. On the demand side, India emerged as the leading destination, importing 0.22 mnt, followed by The Netherlands and Germany at 0.16 mnt each.

While the rebound helped partially offset declines from other Atlantic suppliers, overall buying interest remained cautious, and the increase did not signal a sustained shift in underlying demand conditions. Export sentiment for US coal remains challenged by broader trade headwinds — including the impact of earlier Chinese tariffs that sidelined shipments — while weaker seaborne import demand from key markets continues to temper export momentum even as domestic coal markets show cautious resilience early in 2026.

Canadian shipments edge higher

Canada’s coal exports increased 14.9% w-o-w to 0.94 mnt in week 1, up from 0.82 mnt in the previous week. The rise was supported by consistent port operations and the execution of planned shipments from west coast terminals.

Roberts Bank led loadings with 0.63 mnt, followed by Vancouver at 0.16 mnt and Prince Rupert at 0.15 mnt, reflecting steady throughput across Canada’s key export hubs. Elk Valley Resources emerged as the leading shipper with 0.16 mnt, underscoring the supply-driven nature of the week’s increase.

On the demand side, buying interest from northeast Asia remained selective, with Japan emerging as the leading destination at 0.44 mnt, followed by South Korea at 0.24 mnt. Despite the week-on-week gain, exports continued to trail available capacity amid muted demand visibility at the start of the year.

Coal freights start CY’26 on weak footing

Dry bulk coal freight markets into India remained under sustained pressure during week 1, as thin fixing activity, cautious chartering sentiment, and ample prompt tonnage weighed on rates across key Australia, South Africa, and Indonesia origin routes.

Weak freight sentiment, reinforced by softer FFAs and easing bunker prices, reduced owners’ resistance to lower rate ideas and limited exporters’ urgency to push additional cargoes.

As a result, despite stable port operations and available supply, the subdued freight backdrop constrained shipment momentum, keeping trade flows largely demand-led and preventing a meaningful recovery in coal exports at the start of CY’26.

Outlook

Global coal exports are expected to remain mixed in the near term, with shipment levels sensitive to post-holiday demand recovery and freight market direction. Australian and Indonesian volumes may stabilise if buying interest improves, while South African and US exports are likely to fluctuate based on selective import demand from India and Asia. Atlantic suppliers remain vulnerable to subdued European interest.

Freight markets are expected to stay soft in early January, with ample vessel availability and muted cargo enquiry continuing to cap rates. In the absence of a clear pickup in downstream demand, any recovery in exports is expected to be gradual, keeping coal trade flows cautious as 2026 unfolds.

Leave a Reply