- Pacific gains offset mixed Atlantic performance

- Soft freights, ample tonnage continue to slow down fixing

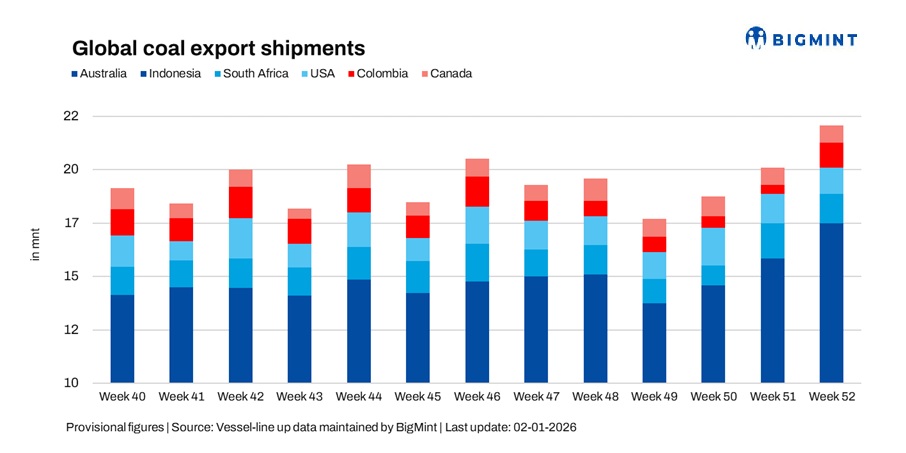

Global seaborne coal exports rose 9.7% w-o-w to 21.62 million tonnes (mnt) in the week ended 26 December (week 52 of 2025), up from 19.70 mnt in week 51, according to BigMint’s vessel line-up data. The increase was primarily driven by stronger shipments from Australia and Indonesia, alongside a sharp rebound in Colombian exports, which together more than offset declines from South Africa and the USA.

This reflected improved cargo availability from key Pacific suppliers, clearance of deferred and year-end cargoes, and stable port operations that allowed exporters to lift shipments ahead of the holiday period. Australia and Indonesia led the gains, benefitting from smoother logistics and the release of previously delayed cargoes, supporting a strong finish to December volumes.

However, despite the increase in shipments, overall market conditions remained uneven. Soft freight sentiment, ample vessel availability, and cautious chartering behaviour continued to limit aggressive fixing activity, keeping trade largely supply-driven rather than demand-led.

Country-wise trends

Australia sees steady year-end loadings

Australia’s coal exports rose 9.5% w-o-w to 8.9 mnt in week 52, up from 8.1 mnt in week 51, marking a third consecutive weekly increase. The rise was supported by steady operations across major east coast ports and exporters’ efforts to maximise shipments ahead of the year-end. Improved operational flows enabled higher loadings despite the absence of a strong demand push. Newcastle remained the leading load port, handling 4.08 mnt, followed by Gladstone at 1.59 mnt and DBCT at 1.38 mnt, reflecting stable throughput across key terminals.

Japan and China emerged as the major importers, taking 2.44 mnt and 2.01 mnt, respectively, accounting for the bulk shipments during the week. Despite the increase in volumes, demand conditions remained restrained, with Indian and northeast Asian buyers continuing to procure selectively on weak downstream margins and comfortable inventories.

BHP led shipments with 0.86 mnt, followed by Glencore at 0.83 mnt and Yancoal at 0.53 mnt, indicating that the rise in exports was largely supply-led, with limited improvement in underlying demand signals. More broadly, Australia’s coal industry saw better coordination across the global coal supply chain in 2025, strengthening its position as a reliable exporter.

Indonesian exports rebound

Indonesia’s coal exports rose 10.8% w-o-w to 8.3 mnt in week 52, up from 7.5 mnt in the previous week, supported by the release of delayed cargoes and stable port operations. The rebound reflected improved shipment execution and logistical normalisation rather than a meaningful shift in underlying market sentiment. Taboneo remained the leading load port with 1.79 mnt, followed by Samarinda at 1.17 mnt and Bunati at 0.87 mnt, highlighting steady throughput across key Indonesian export terminals.

Cargo flows improved as deferred material was cleared ahead of the year-end. On the demand side, China, India, and Japan were the major destinations, importing 2.36 mnt, 1.50 mnt, and 1.11 mnt, respectively. However, buying interest remained cautious due to soft pricing and subdued freight markets, keeping fixing activity measured and leaving Indonesian volumes sensitive to near-term demand fluctuations.

Looking ahead, potential policy headwinds — including plans to tighten production controls and review export levies — could influence shipment volumes and competitiveness in the medium term, particularly in the midst of soft demand.

South African exports ease

South Africa’s coal exports declined 18.2% w-o-w to 1.3 mnt in week 52, down from 1.56 mnt in week 51, following the sharp recovery seen in the previous week. The pullback reflected a normalisation of shipment levels after disruption led pent-up cargoes were cleared, rather than any fresh operational constraints.

All shipments originated from Richards Bay, which handled 1.30 mnt during the week, underscoring stable port operations despite the lower volumes. The easing in exports highlighted the supply-driven nature of the prior week’s surge, with shipment levels reverting closer to underlying demand conditions.

On the demand side, India remained the leading importer, taking 0.38 mnt, followed by Pakistan at 0.16 mnt. However, buying interest stayed selective, and the absence of stronger follow-through demand, combined with soft Atlantic market conditions, continued to cap export volumes despite limited diversification support.

Colombian exports rebound sharply

Colombia’s coal exports surged 178% w-o-w to 1.1 mnt in week 52, rebounding from 0.4 mnt in week 51, as shipments normalised after several weeks of subdued activity. The sharp increase reflected the execution of delayed cargoes and improved shipment flows rather than any meaningful recovery in underlying European demand.

Puerto Nuevo led loadings during the week, handling 0.79 mnt, followed by Puerto Bolivar at 0.11 mnt, highlighting the concentration of export activity at Colombia’s key terminals. The rebound largely represented logistical catch-up after prior-week weakness rather than a sustained improvement in export momentum.

On the demand side, Turkiye and The Netherlands were the leading destinations, importing 0.19 mnt and 0.17 mnt, respectively. Prodeco Group emerged as the dominant shipper with 0.85 mnt, followed by Cerrejon Mines at 0.11 mnt. Despite the recovery, Colombian exports remain vulnerable to ongoing Atlantic basin weakness, with limited flexibility to redirect cargoes and continued reliance on cautious European buyers constraining medium-term recovery prospects.

US shipments decline on weaker demand

US coal exports declined 8% w-o-w to 1.21 mnt in week 52, down from 1.32 mnt in the previous week, reflecting softer follow through demand after earlier seasonal stocking. Competitive pressure from alternative suppliers and muted freight economics limited fresh fixing interest, leading to a moderation in shipment volumes.

Baltimore led loadings with 0.41 mnt, followed by Norfolk at 0.39 mnt and Mobile at 0.24 mnt, indicating steady but reduced export activity across key US terminals. Shipment flows eased as exporters adjusted to softer international demand conditions.

On the demand side, India emerged as the leading importer, taking 0.31 mnt, followed by Turkiye at 0.22 mnt. While domestic market conditions remained relatively supportive, seaborne shipments ended the year on a softer note as exporters balanced international opportunities against stable domestic demand.

Canadian shipments edge up

Canada’s coal exports rose 4.3% w-o-w to 0.82 mnt in week 52, up from 0.79 mnt in week 51, supported by steady port operations and the execution of scheduled cargoes. The marginal increase reflected stable shipment flows rather than any improvement in underlying demand conditions.

Roberts Bank led loadings with 0.48 mnt, followed by Prince Rupert at 0.17 mnt and Vancouver at 0.16 mnt, indicating consistent throughput across Canada’s key export terminals during the week. Operational performance remained stable, allowing exporters to complete planned shipments.

On the demand side, South Korea was the leading importer, taking 0.39 mnt, followed by Japan at 0.18 mnt. Elk Valley Resources shipped 0.16 mnt, while overall buying interest from northeast Asia remained cautious, keeping export volumes below potential capacity despite supportive port operations.

Coal freights soften across key routes

Global dry bulk coal freight markets remained under pressure during week 52, with soft sentiment, ample vessel availability, and thin holiday-period fixing weighing on rates across key Australia, Indonesia, and South Africa to India routes. Cautious buying behaviour, weak downstream visibility, and comfortable inventories reduced charterers’ urgency to secure tonnage, while intense competition among owners continued to cap rate ideas.

Although lower bunker prices offered some marginal cost relief, the benefit was largely offset by subdued freight earnings and limited cargo enquiries. As a result, the softer freight backdrop slowed fixing momentum and muted the impact of higher export volumes, particularly from Indonesia and South Africa, reinforcing a supply-heavy, demand-light market environment.

Outlook

Global coal exports are expected to remain mixed in the near term, with Australia likely to sustain relatively higher shipments if operational stability continues. Indonesian and South African volumes may fluctuate depending on demand visibility and prevailing freight conditions, while Atlantic suppliers are expected to remain under pressure amid subdued European buying interest.

Freight markets are likely to stay soft into early January, with spot fixing activity expected to remain thin until post-holiday normalization. With downstream demand still muted and vessel availability ample, any recovery in trade flows and freights is expected to be gradual, keeping exports sensitive to short-term shifts in demand and overall market confidence as 2026 begins.

Leave a Reply