- Scheduled cargo execution lifts exports

- Firming of freight rates supports coal flows

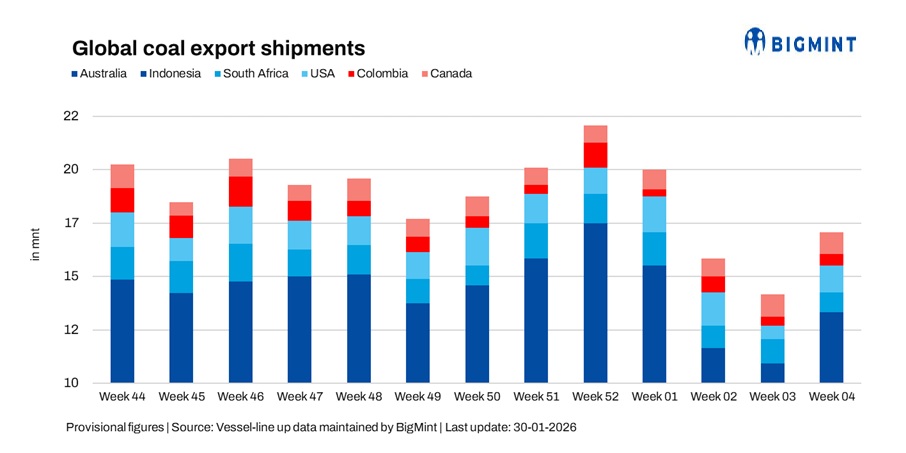

Global seaborne coal exports rebounded sharply by around 20% w-o-w to 16.8 million tonnes (mnt) in week 4 of 2026 (17-23 January) from 14 mnt in week 3 (10-16 January), as per vessel line-up data. The recovery followed three consecutive weeks of softness and marked the first broad-based improvement in shipments this year.

The weekly increase was driven primarily by Indonesia and the US, alongside moderate gains from Australia and Colombia, which outweighed declines from South Africa and Canada. The rebound reflected stronger execution of scheduled cargoes rather than a decisive shift in global demand fundamentals, as buyers remained selective and inventory-led procurement continued across Asia.

Although shipment volumes rose, exporters largely maintained controlled loading programmes, signalling caution amid mixed freight economics and uneven downstream consumption.

Country-wise trends

Australian coal shipments recover

Australia’s coal exports increased 11.3% w-o-w to 6 mnt in week 4 from 5.4 mnt in week 3, reflecting improved cargo execution after earlier disruptions. The rise was supported by stabilising terminal throughput and the clearance of delayed loadings from east coast ports. Shipment activity was led by Newcastle (2.74 mnt), followed by DBCT (1.15 mnt), Gladstone (0.97 mnt), and Hay Point (0.73 mnt), reflecting steady operational throughput across major terminals.

On the supply side, BHP led shipments at 0.73 mnt, followed by Glencore (0.63 mnt) and Yancoal (0.53 mnt), highlighting the schedule-driven nature of export recovery. The rebound also coincided with elevated Australian coal prices after earlier weather disruptions tightened supply, supporting exporters in prioritising planned cargoes. At the same time, domestic coal use in Australia continues to gradually decline as renewable energy expands, keeping export markets a key focus for producers.

On the demand front, China emerged as the largest destination at 0.97 mnt, followed by India (0.31 mnt), while flows into northeast Asia remained broadly stable. Demand showed mild improvement, helping exporters move scheduled cargoes, though buying interest remained measured. Shipments stayed below late-December levels, underscoring continued exporter discipline amid uncertain market direction.

Indonesian exports rise sharply

Indonesia recorded the strongest weekly growth among major exporters, with shipments rising 32.2% w-o-w to 7.22 mnt from 5.46 mnt in the previous week. The surge was driven by heavy execution of backlogged cargoes and smoother loading operations across Kalimantan hubs. Shipment activity was led by Taboneo (1.30 mnt) and Balikpapan (0.89 mnt), reflecting improved terminal throughput and cargo clearance.

On the demand side, China emerged as the largest destination at 1.69 mnt, followed by India (1.26 mnt), Philippines (0.68 mnt), and Vietnam (0.68 mnt), indicating broad-based regional offtake. Despite the rebound in volumes, the recovery remained largely operational rather than demand-led, as importers continued to procure selectively amid cautious market sentiment.

The rebound also comes amid ongoing policy discussions in Indonesia around tighter coal production and export controls, which are encouraging exporters to manage volumes carefully. Meanwhile, demand from key buyers such as China and India remains selective, with utilities continuing short-term procurement rather than aggressive restocking.

South African exports retreat

South Africa’s coal exports fell 20.1% w-o-w to 0.9 mnt from 1.12 mnt, reversing the prior week’s increase. The drop reflected shipment timing and the absence of large scheduled cargoes rather than structural supply constraints. Export activity remained concentrated at Richards Bay (0.90 mnt), reflecting stable terminal operations despite lower weekly throughput.

On the demand side, India remained the largest destination at 0.35 mnt, followed by Pakistan (0.17 mnt) and Israel (0.17 mnt). Indian buying interest was present but cautious, limiting exporters’ willingness to accelerate additional loadings and keeping shipments largely schedule-driven. Shipment consistency remains tied to rail and logistics performance in South Africa, where ongoing operational bottlenecks continue to limit exporters’ ability to maintain steady flows.

Colombian shipments rebound

Colombia’s coal exports increased 28% w-o-w to 0.5 mnt from 0.4 mnt, supported by execution of scheduled Atlantic Basin cargoes. Despite the rise, shipment momentum remained fragile as European demand stayed subdued and largely timing-driven. Structural weakness in Atlantic Basin demand, particularly from Europe’s energy transition, continues to cap Colombia’s ability to sustain higher export volumes.

Export activity was led by Puerto Bolivar (0.35 mnt), followed by Puerto Nuevo (0.15 mnt) and Barranquilla (0.03 mnt), reflecting shipment-specific scheduling rather than broad-based recovery.

On the supply side, Cerrejon Mines led shipments at 0.35 mnt, followed by Prodeco Group (0.15 mnt). The Netherlands emerged as the largest destination at 0.15 mnt, highlighting continued reliance on selective Atlantic Basin demand.

US exports recover strongly

US coal exports nearly doubled, rising 99.2% w-o-w to 1.18 mnt from 0.59 mnt. The rebound reflected the return of large scheduled cargoes after the previous week’s lull, improving port activity across key load terminals. However, exports remained dependent on sporadic cargo programmes amid thin Atlantic Basin demand.

Shipment activity was led by Norfolk (0.47 mnt), followed by Baltimore (0.37 mnt), Mobile (0.17 mnt), and New Orleans (0.17 mnt), reflecting stronger execution of planned cargoes.

On the demand side, Brazil emerged as the largest destination at 0.27 mnt, followed by India (0.24 mnt), highlighting selective Atlantic and Asian offtake. Export momentum continues to be weighed by softer industrial demand and uneven rail movements in the US, limiting the ability to sustain consistent shipment growth.

Canadian shipments edge lower

Canada’s coal exports slipped 4.7% w-o-w to 0.97 mnt from 1.02 mnt, reflecting routine scheduling variability rather than operational weakness. Shipments stayed broadly stable with consistent west coast terminal activity.

Export activity was led by Roberts Bank (0.42 mnt), followed by Vancouver (0.41 mnt) and Prince Rupert (0.14 mnt), reflecting steady terminal throughput.On the supply side, Elk Valley Resources emerged as the leading shipper at 0.41 mnt, underscoring the schedule-driven nature of exports.

Japan remained the largest destination at 0.49 mnt, followed by South Korea (0.33 mnt), anchoring northeast Asian demand despite cautious buying sentiment. Improving trade ties with Asian markets may support Canadian coal exports over time, though current shipment momentum remains driven mainly by cargo scheduling.

Firmer freights, cautious chartering

Coal freight markets firmed during the week, supported by improving dry bulk sentiment and higher bunker prices, which strengthened owners’ rate expectations. Despite the firmer tone, fixing activity remained thin as a persistent bid-offer gap between shipowners and charterers kept negotiations cautious. Abundant vessel availability and selective cargo demand prevented a sharp escalation in rates, even as owners resisted downward pressure.

The mixed freight environment enabled exporters to execute previously scheduled cargoes but discouraged aggressive expansion of loading programmes. As a result, shipment growth remained measured and timing-driven, reinforcing a controlled recovery in global coal flows rather than signalling a broad-based demand resurgence.

Outlook

Global coal exports are expected to remain volatile in the near term, with shipment momentum continuing to depend more on cargo scheduling than a broad-based demand recovery. Indonesian and Australian volumes are likely to remain supported by operational execution, while US and Colombian flows may fluctuate with Atlantic cargo availability. South African exports could stay uneven amid cautious Indian demand.

Freight markets are expected to stay range-bound as vessel supply remains comfortable and cargo enquiries thin. Without a sustained pickup in downstream coal consumption, exporters are likely to maintain disciplined shipment programmes, keeping global trade stable but fragile in the coming weeks.

Leave a Reply