- Global coal exports up 1.7% w-o-w

- Outlook rangebound-to-soft on weak India demand

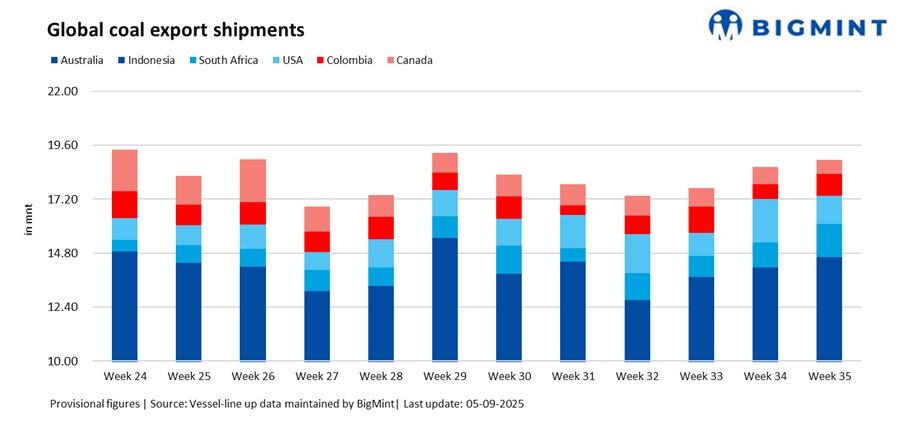

Global seaborne coal exports inched up by 1.7% w-o-w to 18.94 million tonnes (mnt) in week 35 (23-29 August 2025), compared with 18.63 mnt in week 34 (16-22 August), according to BigMint’s vessel line-up data. The rise was largely supported by stronger shipments from Australia and South Africa, which outweighed notable declines from the US and Canada. Colombian exports also staged a recovery, while Indonesian flows held broadly steady.

The improvement reflected the gradual stabilisation of supply chains following earlier weather-related disruptions in Australia and South Africa. Meanwhile, global demand remained mixed, with Chinese buyers stepping up restocking activity, while Indian utilities continued to exercise caution amid sufficient stockpiles. European demand remained selective, focused mainly on South African and Colombian cargoes, which provided additional support to overall flows.

Country-wise trends

Australia: Coal exports from Australia continued their upward momentum, rising 7.1% w-o-w to 7.55 mnt in Week 35 from 7.05 mnt in Week 34. Higher loadings from Newcastle 3.02 mnt, DBCT 1.26 mnt and Gladstone 1.16 mnt drove the increase, as vessel availability improved and weather-related delays subsided.

On the demand side, China 2.01, Japan 1.92 and South Korea 0.74 remained steady buyers of both thermal and metallurgical coal, cushioning against softer demand from India.

Market participants highlighted that, Australian exporters benefited from smoother port clearances this week, which allowed quicker vessel turnarounds and sustained shipment volumes.

Indonesia: Indonesian coal exports slipped marginally by 0.7% w-o-w to 7.07 mnt in Week 35, compared with 7.12 mnt in the prior week. Despite the slight decline, shipments held broadly stable against earlier August levels.

Loadings were constrained by softer procurement from Indian utilities, where high domestic stockpiles curbed import appetite. On the demand side, India (1.53 mnt) and China (1.50 mnt) emerged as the top buyers, while Japan and South Korea (0.71 mnt each) also contributed, helping prevent a sharper downturn in volumes.

Seasonal monsoon-related disruptions continue to weigh on flows, though market participants anticipate a firmer recovery as weather conditions improve into September.

South Africa: South African coal exports recorded the sharpest weekly increase, surging 35.6% w-o-w to 1.49 mnt in Week 35, up from 1.10 mnt in Week 34. The rebound was supported by improved railings to Richards Bay Coal Terminal (RBCT), which handled the entire 1.49 mnt despite recurring bottlenecks in recent months.

India emerged as the largest buyer at 0.62 mnt, led by demand from sponge iron and cement producers, while additional support came from European utilities.

The recovery underscores South Africa’s significant export potential; however, market participants cautioned that sustained growth hinges on consistent rail performance, as frequent logistical disruptions have historically capped volumes.

USA: Coal exports from the US fell sharply by 36% w-o-w to 1.23 mnt in Week 35, reversing the strong gains seen a week earlier. The decline was primarily due to reduced loadings at key East Coast terminals, with Norfolk handling 0.43 mnt and Baltimore 0.31 mnt, alongside weaker transatlantic flows to Europe.

Indian demand also softened to 0.25 mnt, adding further pressure on overall volumes. Market participants noted that persistent logistical challenges and limited fixture activity restricted shipments during the week.

Looking ahead, US exports are expected to stabilise at moderate levels, although weather conditions and the strength of transatlantic demand will remain decisive factors.

Colombia: Colombian coal exports staged a strong recovery in Week 35, rising 45% w-o-w to 0.96 mnt from 0.66 mnt in Week 34.

The rebound was driven by higher activity at Puerto Nuevo (0.45 mnt) and Puerto Bolivar (0.34 mnt), both of which had recorded significantly lower loadings in the previous week.

On the demand side, Brazil (0.28 mnt) and The Netherlands (0.26 mnt) emerged as the largest buyers, helping to stabilise flows. Despite the improvement, shipments remain below seasonal averages, with market participants noting that persistent logistical constraints and limited vessel availability continue to cap Colombia’s export potential.

Canada: Canadian coal exports declined by nearly 17% w-o-w to 0.64 mnt in Week 35, reversing the modest gains recorded earlier in August.

Activity slowed across key terminals, with Vancouver and Roberts Bank each handling around 0.25 mnt, while Prince Rupert contributed 0.15 mnt as fewer vessels were reported in the line-up.

On the demand side, South Korea (0.34 mnt) and China (0.17 mnt) accounted for the bulk of purchases, though Japanese buyers continued to favor Australian cargoes given their shorter voyage times and more competitive freight costs.

Looking ahead, Canadian shipments are expected to remain under pressure, with logistical bottlenecks and subdued Asian appetite limiting any scope for a meaningful rebound.

Freight trends: Dry bulk coal freights to India held firm w-o-w across major routes from Australia, South Africa, and Indonesia, supported by stronger Pacific basin sentiment and stable vessel supply.

While Panamax and Supramax rates found support from a firmer Atlantic market and rising futures, physical fixture activity remained muted.

Chinese buying ahead of the September-October peak steel production season, along with tighter coal supply signals, provided some upside to market sentiment. Still, the overall tone remained cautious, as activity in the Indian Ocean stayed muted and most operators restricted bookings to need-based procurement.

Outlook

Global coal exports are likely to remain steady to marginally higher in the near term, led by Australia and South Africa if port and rail operations hold firm. Indonesian flows may stay range-bound under seasonal weather pressure, while US and Canadian shipments remain volatile amid logistical and demand challenges.

On the freight side, mixed trends are expected, with Pacific basin sentiment and futures lending support but muted Asian demand, ample Indian stocks, and wide bid-offer spreads limiting upside. Overall, freights are projected to stay range-bound to slightly softer, with sentiment hinging on Chinese restocking and broader dry bulk dynamics.

Leave a Reply