- Australian exports stabilise as Asian utility demand stays selective

- Freight volatility and rising bunker costs temper export recovery

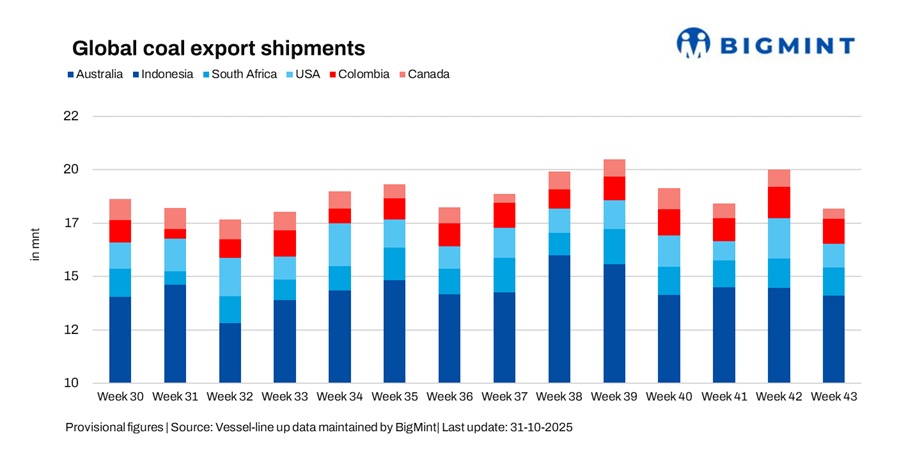

Global seaborne coal exports fell 8.9% week-on-week (w-o-w) to 17.85 million tonnes (mnt) in week 43 (18-24 October 2025) from 19.60 mnt in week 42 (11-17 October 2025), according to BigMint’s vessel line-up data. The weekly decline was driven primarily by weaker shipments from Indonesia, the US, Canada, and Colombia, while Australia’s exports stabilised, cushioning the overall drop.

Market activity remained subdued through the week as freight volatility, muted fixture activity, and soft industrial demand continued to weigh on shipments. Although Australian ports maintained steady throughput, sentiment across most origins stayed cautious amid rising voyage costs and selective procurement by Asian utilities.

Country-wise trends

Australia’s coal exports rose 2.2% w-o-w to 7.06 mnt in week 43 from 6.90 mnt in week 42, supported by steady shipment activity and improved vessel turnaround at major terminals. Loadings from Newcastle (3.43 mnt), Gladstone (1.31 mnt) and DBCT (1.01 mnt) remained consistent, backed by stable miner output from Glencore (1.04 mnt), Yancoal (0.52 mnt), and BMA (0.46 mnt).

The improvement in port efficiency and vessel scheduling helped sustain export momentum despite selective buying from key Asian utilities. Demand from Japan (2.01 mnt) and China (1.29 mnt) continued to anchor flows, while Indian purchases stayed limited amid higher freight costs at (0.23 mnt). Although overall sentiment was steady, firmer freight rates on the Australia-India route capped incremental bookings. Coking coal trade saw mild support from restocking by northeast Asian steelmakers, but broader demand remained cautious as buyers monitored price movements and freight volatility.

Indonesia’s coal exports fell 6.6% w-o-w to 6.89 mnt in week 43 from 7.38 mnt in week 42, as post-festive loading activity slowed and spot chartering declined. Loadings from key terminals such as Taboneo (1.01 mnt), Palembang (0.71 mnt), Bunati (1.15 mnt), and Samarinda (0.68 mnt) eased due to weaker vessel scheduling and reduced export nominations from mid-tier miners. The slowdown followed a brief rebound seen earlier in October, with several ports reporting delays in vessel arrivals and cargo readiness amid fluctuating weather conditions.

On the demand side, China (2.14 mnt), India (1.11 mnt), the Philippines (0.58 mnt), and Malaysia (0.58 mnt) remained the leading importers. However, muted restocking by Indian utilities and cautious procurement across Southeast Asia limited overall shipments. Softer freight rates on the Indonesia-India route provided little support, as subdued industrial coal demand and healthy stock positions across Asia continued to weigh on export momentum.

South Africa’s coal shipments dropped 5.1% w-o-w to 1.27 mnt in week 43 from 1.34 mnt in week 42, weighed down by persistent logistical bottlenecks and slower vessel turnaround at RBCT, which handled the entire export volume. Congestion at loading berths and intermittent rail delays continued to restrict throughput, while limited vessel nominations reflected muted buying interest from key Asian markets. The overall decline extended the trend of subdued export performance seen in recent weeks, as operational inefficiencies and inconsistent port performance constrained loadings.

India remained the principal destination, taking around 0.63 mnt of South African coal during the week. However, elevated freight levels and cautious sentiment among charterers kept fixture activity limited, with several cargoes reportedly deferred to upcoming weeks. Despite steady miner output, weak demand and higher transportation costs curtailed any meaningful rebound in exports, leaving overall market momentum soft heading into the final week of October.

Colombia’s coal exports slumped 22.5% w-o-w to 1.10 mnt in week 43 from 1.42 mnt in week 42, pressured by slower port operations and weaker Atlantic basin demand. Loadings from Puerto Nuevo (0.67 mnt) and Puerto Bolivar (0.11 mnt) accounted for the bulk of shipments, primarily driven by Prodeco Group (0.72 mnt) and Cerrejon (0.11 mnt). Operational delays and limited vessel scheduling further constrained throughput, as exporters adjusted to reduced inquiries from European and trans-Atlantic buyers.

Despite stable miner availability, high inventories across key importing hubs and elevated freight costs discouraged fresh procurement. Weak European buying interest and compressed arbitrage margins continued to weigh on Colombian coal exports, keeping sentiment subdued. Market participants noted that without a pickup in Atlantic basin demand or easing freight pressures, shipment recovery is likely to remain constrained in the near term.

United States’ coal exports plunged 41% w-o-w to 1.06 mnt in week 43 from 1.80 mnt in week 42, as weaker vessel nominations and port delays significantly curtailed loadings. Throughput at major terminals, including Norfolk (0.56 mnt), New Orleans (0.24 mnt), Baltimore (0.15 mnt), and Mobile (0.11 mnt), dropped notably amid logistical constraints and limited vessel turnaround.

India remained a modest buyer at 0.42 mnt, but elevated bunker costs and subdued Atlantic basin demand weighed heavily on overall sentiment. Market sources noted minimal fixture activity along the US East Coast, reflecting a persistent disconnect between available supply and tepid buyer appetite, particularly from Europe and Asia.

Canada’s coal exports fell 37.8% w-o-w to 0.47 mnt in week 43 from 0.76 mnt in week 42, as slower loadings and logistical bottlenecks weighed on shipments. Activity at key terminals – Roberts Bank (0.23 mnt), Vancouver (0.21 mnt), and Prince Rupert (0.03 mnt) remained subdued due to tight rail capacity and intermittent congestion that disrupted coal movement to ports.

South Korea (0.17 mnt) and Japan (0.10 mnt) remained the principal buyers, though elevated freight costs and weak arbitrage margins continued to erode trade competitiveness in the Pacific market.

Dry bulk freights exhibit mixed momentum

Dry bulk coal freights exhibited mixed trends during week 43. The Australia-India route strengthened amid active spot buying by Indian steelmakers and tighter vessel availability, while the Indonesia-India route softened due to subdued cargo inquiries and oversupply of tonnage. The South Africa-India route remained steady on balanced but quiet trading conditions.

Freight volatility and higher voyage costs weighed on overall export sentiment, particularly from Indonesian and Atlantic origins, where soft fundamentals failed to offset rising bunker prices. Although the Pacific market saw isolated strength, overall chartering activity remained conservative as traders monitored short-term demand fluctuations and cost pressures.

Outlook

Global coal export momentum is likely to remain subdued in the near term, with freight volatility and soft Atlantic basin demand continuing to cap upside potential. Australian shipments are expected to stay firm on steady northeast Asian demand, while Indonesian exports may stabilise once vessel scheduling normalises.

However, US, Canadian, and Colombian flows are likely to remain under pressure amid logistical constraints and weak European procurement. Overall sentiment stays cautious, with selective chartering and rising voyage expenses expected to influence near-term coal trade dynamics.

Leave a Reply