- Seasonal factors continue to weigh on shipments

- Freight rates fall as fixture activity slows

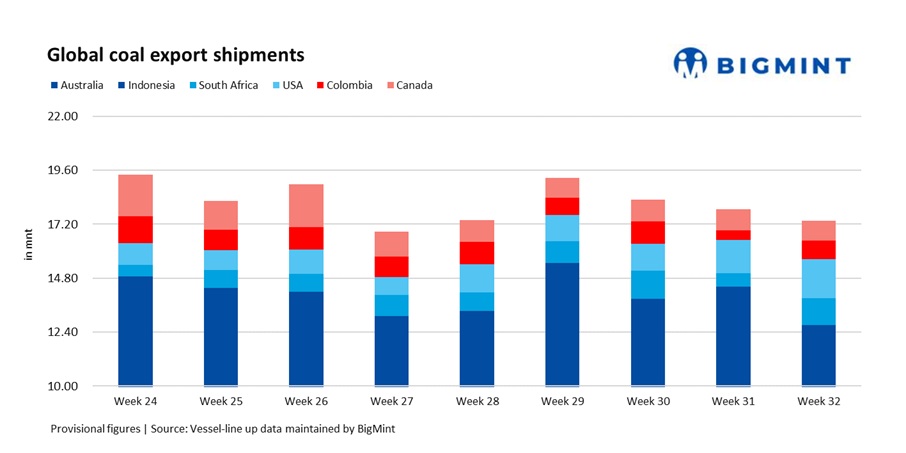

Global coal exports across the six key origins monitored by BigMint through vessel lineup fell to 17.36 million tonnes (mnt) in week 32, 2025 (2-8 August), marking a 2.8% decline w-o-w from 17.87 mnt in week 31, 2025 (26 Jul-1 Aug). The drop was driven primarily by weaker shipments from Australia and Indonesia, whose combined volumes fell by nearly 1.7 mnt w-o-w.

Adverse weather conditions, operational bottlenecks at ports, and a seasonal softening in Asian demand were the main factors weighing on volumes. South Africa and the United States, however, posted notable gains, with the latter recording its highest weekly total since past weeks.

Country wise exports

Indonesia’s coal exports fell sharply to 6.78 mnt in week 32, down 10.9% from 7.61 mnt the previous week.

This week, China remained the largest importer at 1.68 mnt, followed by India at 1.15 mnt and South Korea at 0.96 mnt. According to sources, shipments during this period were weighed down by weaker demand from major buyers China and India.

The demand slowdown is linked to higher domestic coal production in both China and India. While Indonesia’s output is expected to remain strong in the near term, gradual moderation is anticipated over time as the global energy transition gains pace.

Australia slipped to second position as the country’s coal shipments fell sharply to 5.94 mnt in Week 32, down 12.9% from 6.82 mnt the previous week. BigMint noted, movement slowed at key east coast terminals, including Newcastle (1.89 mnt) and Gladstone (1.42 mnt), with several cargoes facing deferred loading windows.

The drop was driven by a combination of operational bottlenecks, adverse weather, and subdued global steel production. Weak buying interest from Japan (1.83 mnt) and muted tender activity from China (1.56 mnt) further weighed on demand. The downturn reflects both logistical constraints at major ports and fluctuating price dynamics.

United States coal exports bucked the trend in Week 32, rising to 1.73 mnt, an 18.4% gain w-o-w from 1.46 mnt the previous week marking the highest weekly figure since past few weeks.

Key loading ports included Norfolk (0.76 mnt), Mobile (0.43 mnt), and Baltimore (0.32 mnt). Major destinations were India, importing 0.41 mnt, and the Netherlands, at 0.37 mnt.

This uptick was driven by continued demand from Atlantic-basin buyers, notably European utilities ramping up high-calorific-value thermal coal replenishment ahead of autumn restocking. Meanwhile, coking coal exports to India also strengthened, supported by steady procurement from steel mills in eastern India.

South Africa recorded the sharpest rebound in Week 32, with coal loadings nearly doubling w-o-w to 1.19 mnt from 0.60 mnt in Week 31. A temporary rail disruption over the weekend caused by a train failure and track issues briefly halted shipments, but Transnet’s operations recovered swiftly, underscoring the resilience of the coal corridor.

According to major sources, monthly shipment volumes has been improving consistently, with year-end volumes projected to increase significantly, surpassing earlier forecasts.

The week’s surge was driven by the clearance of backlogged vessels at RBCT following easing congestion, alongside stronger nominations from Indian buyers and select Atlantic-bound cargoes.

Canada’s exports dropped to 0.88 mnt from 0.95 mnt, a 7% w-o-w decrease, with steady flows to Northeast Asia but no notable spot market activity.

Key importers were South Korea with 0.34 mnt and Japan with 0.24 mnt, followed by China with 0.18 mnt. By port, shipments were led by Roberts Bank at 0.41 mnt, followed by Vancouver at 0.31 mnt and Prince Rupert at 0.17 mnt.

Colombia, in contrast, saw shipments increase to 0.84 mnt from 0.44 mnt, a 91% w-o-w increase, as European utilities sought high-CV cargoes and Middle Eastern buyers also stepped into the market.

Dry bulk coal freights fall on sluggish fixtures

Dry bulk freight rates for coal shipments to India fell across major routes this week, with the South Africa-India for Panamax segment seeing the sharpest drop. Rates from Australia, South Africa, and Indonesia all remained under pressure amid muted market activity, as buyers particularly sponge iron producers stayed cautious due to weak domestic coal prices.

Not many fixtures were reported this week as buyers continued to be taking a cautious approach, specially sponge iron players, as prices witnessed a drop in the week under review in the Indian domestic market.

Outlook

In the near term, South Africa and the US could maintain export growth on strong Atlantic demand and better logistics, while Australia and Indonesia may remain under pressure from weak Asian buying and port delays. Restocking by India and Japan may support coking coal flows, but robust domestic output in China and India could limit imports. Freight rates are expected to stay soft unless cargo demand improves.

Leave a Reply