- Australia, Indonesia drive gains on firm Asian demand

- Higher bunker costs, geopolitical risks weigh on Atlantic flows

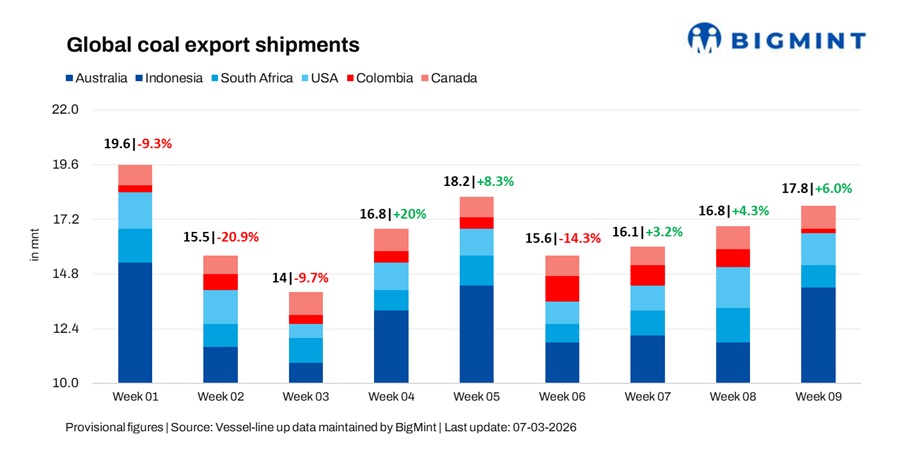

Global seaborne coal export shipments increased 6% w-o-w to a four-week high of 17.8 mnt in the week ended 27 February 2026, supported mainly by stronger exports from Pacific origins such as Australia and Indonesia, while Atlantic suppliers recorded mixed trends amid softer demand and logistical constraints.

Pacific flows strengthen on firm Asian demand

In the Pacific, Australia shipments rose to 6.8 mnt, led by Newcastle (2.4 mnt), Gladstone (1.6 mnt) and DBCT (1.2 mnt). BHP shipped 1.0 mnt, while Japan (2.2 mnt) and China (0.9 mnt) remained the key destinations.

Indonesian exports rose to 7.4 mnt, supported by firm Asian demand. Taboneo (1.1 mnt) and Samarinda (0.8 mnt) led loadings, while China (1.7 mnt) and India (1.3 mnt) remained the key buyers.

Atlantic flows remain subdued

The US recorded shipments of 1.4 mnt, with Norfolk leading exports at 0.7 mnt, followed by Baltimore at 0.4 mnt. India remained a key buyer, receiving around 0.3 mnt during the week.

South African exports declined to 1.0 mnt, with Richards Bay accounting for the entire volume, amid slower export momentum and rail logistics constraints.

Canadian volumes remained stable at 1.0 mnt, led by Roberts Bank at 0.5 mnt and Vancouver at 0.3 mnt, while Japan and Taiwan each received 0.2 mnt.

Meanwhile, Colombian shipments fell to 0.2 mnt, with Cesar Coal and Carbosan contributing 0.1 mnt each, shipped via Barranquilla and Puerto Nuevo, reflecting weaker export activity.

Dry bulk coal freights to India rise w-o-w

Dry bulk coal freights to India increased w-o-w, with Pacific routes reaching multi-month highs amid tightening vessel availability and rising bunker prices. Firm cargo demand and higher fuel costs supported freight levels, while Atlantic sentiment remained mixed as market participants monitored cargo flows and vessel positioning.

Outlook

Market participants expect export flows to remain mixed in the near term, with Pacific shipments likely to stay supported by steady Asian demand and active loading programmes. However, Atlantic volumes may continue to face pressure from logistical constraints, bunker price volatility, and cautious buying sentiment across key importing regions.

Leave a Reply