- Australian exports fall 15%; South Africa sees 29% rise

- China’s lower import appetite continues to weigh on trade

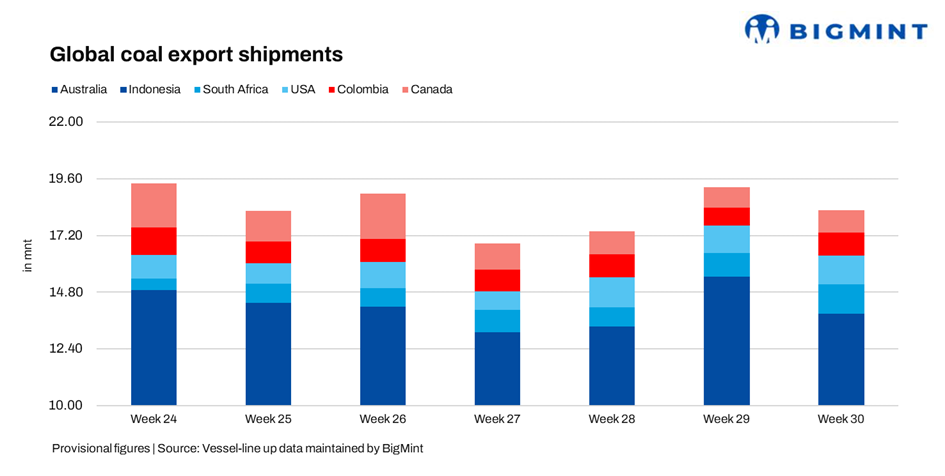

Global coal (coking, non-coking, and met coke) export shipments declined by 5% w-o-w to 18.29 million tonnes (mnt) in Week 30 (19-25 July 2025), from 19.26 mnt in Week 29 (12-18 July), according to vessel line-up data compiled by BigMint. The decline followed a pullback by major exporters such as Australia and Indonesia, after they had recorded strong shipment volumes the previous week.

Buying activity across key Asian markets remained limited, with ample stock availability at ports and power plants keeping demand subdued. Mild summer conditions in parts of East Asia, coupled with moderated power consumption and ongoing rainfall across regions of India, further weighed on thermal coal demand. Vessel bookings slowed as traders adopted a cautious approach amid volatile freights and uncertain price signals, BigMint understands.

Meanwhile, subdued demand from China and increased domestic production continued to weigh on overall coal export volumes. In H1CY’25, China’s coking coal imports dropped 8% y-o-y to 52.83 mnt, with increased domestic production reducing dependence on seaborne cargoes.

Country-wise exports

Australia takes top spot but shipments fall

Australia retained its position as the top exporter, but shipments declined 15% to 7.04 mnt in Week 30 from 8.26 mnt recorded in Week 29.

Eastern Australia, home to major coal ports such as Newcastle, Gladstone, and Hay Point, experienced heavy rainfall and rough sea conditions. These adverse weather events typically resulted in loading delays at ports, temporary closures or vessel congestion at anchorages, and disruptions to rail haulage from mines to export terminals, collectively impacting overall coal supply logistics.

Operational constraints weigh on Indonesian exports

Indonesia ranked second in Week 30, with shipments slipping by 5% w-o-w to 6.84 mnt from 7.21 mnt in Week 29.

Operational challenges, including rain-related disruptions and falling water levels at loading terminals in Kalimantan, contributed to supply chain delays. Sources noted that the logistical bottlenecks were largely driven by reduced river water levels, which hindered barge and vessel movement for miners in the region.

South Africa records steep rise amid improved logistical operations

South Africa secured the third spot in Week 30. Contrasting with the overall trend, coal exports rose 29% w-o-w to 1.26 mnt from 0.98 mnt in Week 29.

The increase was largely attributed to improved turnaround times at the Richards Bay Coal Terminal (RBCT), supported by more stable rail operations following weeks of disruption and the completion of maintenance work at the port, which had previously constrained export volumes.

US export volumes remain flat

US coal exports held steady at 1.20 mnt in Week 30, marking a modest 2% increase from 1.17 mnt in Week 29.

The marginal uptick came despite reduced shipments to China following the imposition of a 15% import tariff. While the US continues efforts to redirect supply to emerging Asian markets, high mining costs and elevated freights remain significant challenges. Broader macroeconomic concerns and geopolitical uncertainties also continued to dampen demand for US coal.

Colombia boosts exports with shift in focus to Asian markets

In Week 30, Colombia’s coal exports totalled 0.98 mnt, marking a significant 27% increase from 0.77 mnt in Week 29.

Colombia has witnessed an uptick in coal shipment volumes in recent weeks, driven by a gradual shift in export destinations from Europe to Asia-Pacific markets. This transition comes as European import demand continues to weaken, prompting Colombian miners to explore alternative markets in Asia. However, despite the growing interest in the region, Colombian coal faces stiff competition due to its longer voyage times and elevated freight costs, which make it less economically viable compared to closer and more cost-effective suppliers such as Australia.

Canada’s exports rise 10%; Glencore makes strategic expansion

Canada’s coal exports rose 10% to 0.96 mnt in Week 30 from 0.87 mnt recorded in Week 29.

The coal sector received a notable boost following Glencore’s acquisition of Elk Valley Resources — a strategic move anticipated to enhance future export potential. The acquisition is expected to drive increased production capacity and operational efficiency, positioning Glencore to better meet global demand, particularly in the metallurgical coal segment.

Outlook

Global coking coal trade is expected to stay subdued in the near term amid weak steel production and cautious buying, though a modest recovery in industrial activity across emerging Asian economies could provide limited upside. Australia faces export headwinds from soft demand and climate disruptions, while Russia and Mongolia are gaining ground as key suppliers. Trade flows remain fluid, with volatility likely to persist unless steel fundamentals improve meaningfully.

Meanwhile, the coal freight market also remains soft, with seasonal monsoon disruptions in India slowing imports and vessel bookings — especially on Indonesia-India and South Africa-India routes. Port congestion, uneven discharge, and weak spot demand from Asian buyers are further weighing on Panamax and Supramax segments.

While firm coal prices and occasional weather issues may offer brief support, a significant recovery in freight is unlikely before the post-monsoon season or a stronger rebound in regional demand.

Leave a Reply