- Offers to Turkiye up on stronger sales

- Iran prices rise amid power outages

The global steel market remained cautious with uneven demand and supply constraints seen across regions. East and Southeast Asia showed steady pricing trends and stronger exports, while South Asia and parts of Southeast Asia face tight supply and weak buying. The Middle East experienced moderate demand amid challenges. Overall, production issues and cautious sentiments are likely to keep the market range-bound as mills focus on protecting margins.

Turkish deep-sea imported scrap (HMS 80:20) prices saw an increment of $4/t w-o-w, to $347/t, CFR as sellers held firm despite limited buying interest. As a result, Turkish mills accepted higher scrap prices, supported by improved demand and stronger sales in the finished long steel segment, even though overall market activity remained relatively slow. US-origin HMS 80:20 bulk scrap stood at $347/t CFR Turkiye, stable w-o-w.

The Asian billet market remains divided, with sentiment varying across key regions. Southeast Asia continues to see weak demand and limited buying activity, while Chinese mills adopted a steady, wait-and-see approach amid cautious conditions. In contrast, Indonesia displayed a firmer outlook, weighed by recent bulk sales to regional buyers.

Market highlights

- The Vietnamese billet market is currently facing a shortage of BF-route export offers. According to sources, supply remains tight, and no fresh offers have been reported. Domestic availability is limited, and mills are unlikely to resume exports before July. This situation is primarily driven by reduced output and constrained supply due to ongoing production cuts.

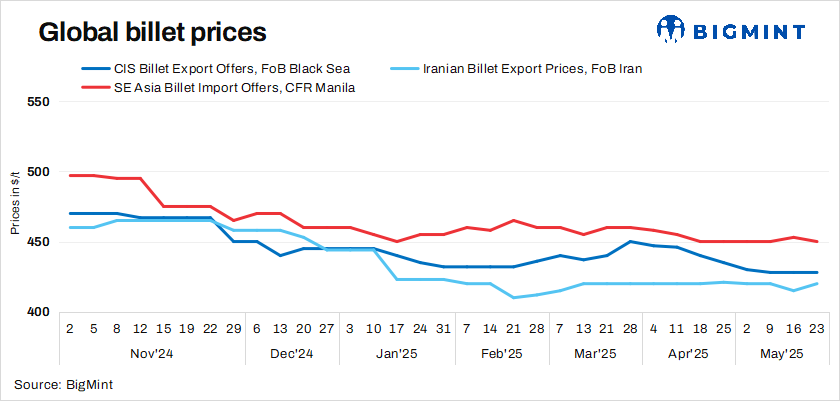

- In the Philippines market, billet offers for CFR Manila declined by $3/t w-o-w to $450/t on 23 May. However, buyers remained cautious and are targeting lower bid levels around $440–445/t amid prevailing market conditions. Meanwhile, the Russian Billet Index, FOB Black Sea, remained stable at $420/t w-o-w.

- Iran’s semi-finished steel market saw a slight price increase this week. Billet offers for 130×130 mm 3sp, FOB Bandar Imam Khomeini, rose by $5/t w-o-w to $420/t. An Iranian mill concluded a 60,000-t billet export tender. The deal included 30,000 t (150×150 mm 3SP/5SP) of billets priced at $422/t FOB, and 30,000 t of low-carbon billets at $430/t FOB. The surge in prices came as major production hubs grappled with severe power outages and liquidity challenges. Ongoing liquidity stress is hampering production recovery, while low inventories may fuel a rebound in demand.

- Chinese billet prices held steady w-o-w amid seasonally slowing demand and absence of fresh stimulus. Steel billet prices in Tangshan, China, stood at RMB 2,950/t ($409/t), including 13% VAT, on 23 May, unchanged from 16 May. The market remained range-bound this week, weakening the prior week momentum. This was largely driven by declining raw material costs, stable finished steel prices, and an imbalanced demand-supply dynamic as mills prioritised margin protection. Additionally, SHFE rebar futures dropped by RMB 36/t ($5/t) w-o-w, settling at RMB 3,046/t ($423/t).

Leave a Reply