- Turkiye imported scrap up on higher finished steel demand

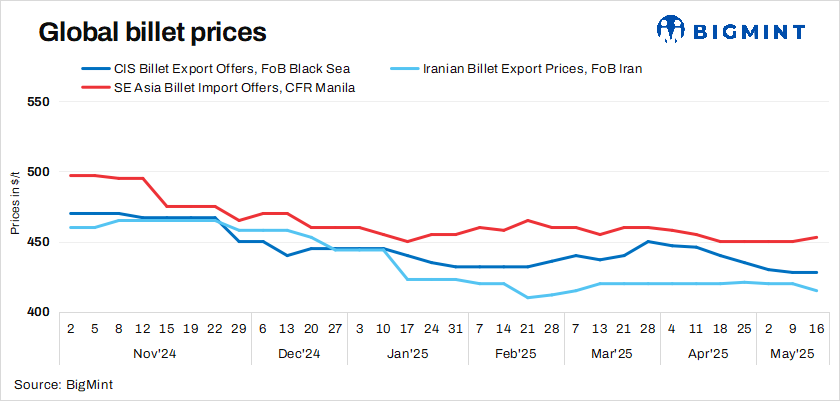

- Southeast Asia & Middle-East billets show mixed trends

Global billet prices across Southeast Asia showed mixed trends in the 20th week of 2025, mainly driven by regional activities. The steel billet market in parts of the Middle East and Southeast Asia remained sluggish, with weak demand and some regional price variations. Production cuts at certain mills added to the slow pace. In contrast, the Chinese market saw a strong boost in demand following a duty rollback, strengthening both export and domestic markets. Markets showed agility amid improved trade policies, while demand for finished steel products began to recover.

The Turkish deep-sea imported scrap market recorded a w-o-w uptick, with US-origin HMS 80:20 bulk scrap assessed at $347/t CFR Turkiye (up $11/t w-o-w) . The rise was supported by stronger domestic rebar sales and firming prices. Despite ongoing interest in June-July shipments, mills continue to resist further scrap price hikes.

The Asian billet market showed mixed trends, with weak demand in Taiwan and reduced export availability from Vietnam. China’s market rebounded, boosting both domestic and export demand. Scrap prices in Taiwan and Vietnam edged up slightly, while Japan’s steel demand remained soft.

Market highlights

- In the Vietnamese billet market, export offers from BF-route producers were heard at $435-440/t FOB. However, mills showed a stronger preference for the domestic market, where prices hovered at around $450/t ex-works – more attractive than export levels. With limited billet availability locally, most suppliers have run out of spot offers. Notably, even major producer Hoa Phat Group is now seeking to procure billets from the domestic market, reflecting tightening supply conditions amid production cuts.

- Iran’s semi-finished steel market continued being effected, and has dropped by $5/t to $415 FOB, w-o-w. Iranian mills were heard concluding billet export deals at around $415/t FOB and $410-418/t FOB, sources informed BigMint. Meanwhile, ESCO, too, concluded an export deal for 30,000 t of high manganese billets at $427/t FOB this week. Meanwhile, the domestic market is facing severe supply constraint, starting this week. The reason for this is the reduction in actual working hours due to power shortage. Buyers in the United Arab Emirates and Oman are increasingly cautious, viewing Iranian supply as risky due to potential non-compliance with ECAS certification – required for rebar sales in the UAE market.

- Chinese billet prices edged up RMB 40/t ($6/t) w-o-w amid macro-economic boosters. Steel billet prices in Tangshan, China, inched up by RMB 40/t ($6/t) w-o-w to RMB 2,950/t ($402/t), including 13% VAT, on 16 May as against 9 May. The market witnessed a sharp rebound in steel billet tags, regaining the momentum lost in previous weeks, driven by improved demand, particularly for downstream products, and optimism surrounding recent tariff cuts. Mid-week, prices hit RMB 2,990/t ($415/t) before easing slightly. Meanwhile, SHFE rebar futures also gained RMB 60/t ($8/t) w-o-w, reaching RMB 3,082/t ($428/t).

Leave a Reply