- Middle East exports rise, driven by Indian demand

- Intra-EU trade declines as sanctions hit recyclers

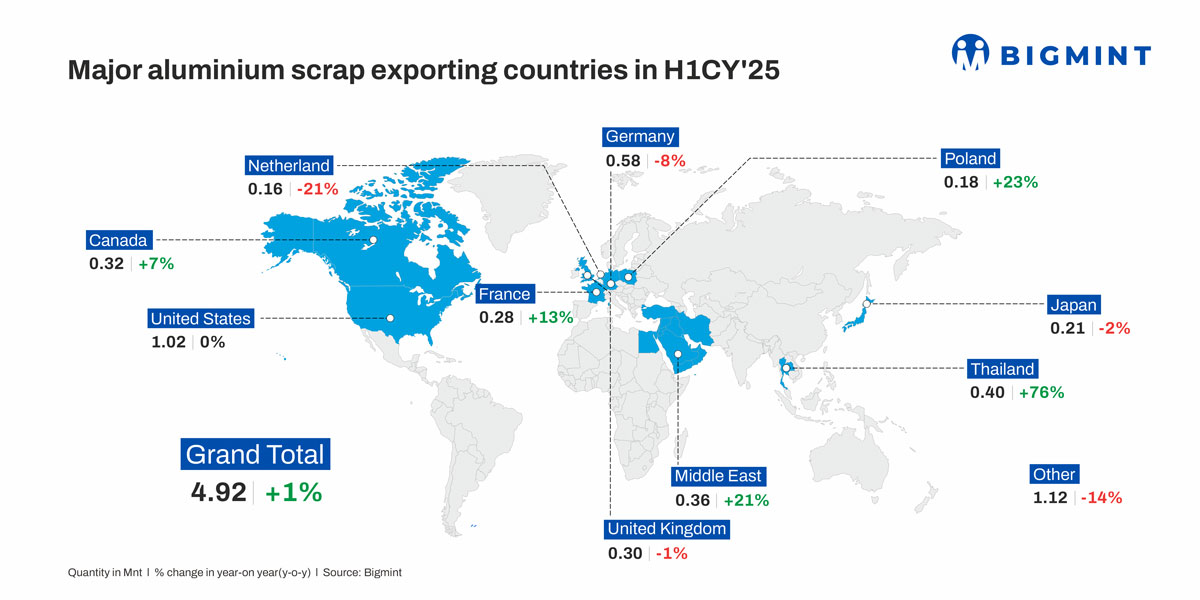

Global aluminium scrap trade volumes, including intra-European trade, stood range-bound y-o-y with a minor increase of 1% in the first half of 2025 (H1CY’25) despite various challenges impacting market activity. Total imports in H1CY’25 stood at 4.92 million tonnes (mnt) compared to almost 4.89 mnt in H1CY’24, as per provisional data available with BigMint.

Notably, the global aluminium scrap trade typically ranges between 9-10 mnt annually. In 2024, the global trade volume stood at 9.7 mnt.

Why did global aluminium scrap trade remain stagnant in H1CY’25?

Primary aluminium production remains firm: Global primary aluminium output remained stable at 36.4 mnt in H1CY’24, up a minor 1.4% y-o-y, amid macroeconomic challenges and trade frictions. Strong price support from the London Metal Exchange (LME) ($2,499-2,593/t) facilitated steady smelting operations, though rising alumina costs ($363/t) squeezed margins. China remained the leading producer, with output from other regions also gaining.

Major exporting countries in H1CY’25

The United States (US) remained the global leader in aluminium scrap exports; however, volumes stood steady y-o-y at 1.02 mnt in H1CY’25. Germany remained the second-largest exporter with 0.58 mnt in H1, witnessing a decrease of 8% y-o-y.

Other key exporters such as Thailand and the Middle East saw gains of 76% and 21% y-o-y, respectively. On the other hand, the UK and Canada witnessed modest changes, and France saw a 13% rise in exports in H1CY’25.

What happened in the top exporting nations?

US: Aluminium scrap exports from the US remained largely stable in H1CY’25, despite a decline of up to 23% in shipments to several key destinations. However, exports to countries such as Thailand and Hong Kong rose, driven by better price realisations in those markets.

Meanwhile, countries such as India, Malaysia, and South Korea recorded notable declines in aluminium scrap imports from the US — down 15%, 21%, and 23%, respectively. Specifically, US exports to India, one of its key markets, stood at 0.18 mnt in H1CY’25 against 0.21 mnt in H1CY’24.

This contraction followed the Trump administration’s imposition and subsequent doubling of tariffs on steel and aluminium imports — from 25% in March to 50% by early June — making US scrap less competitive in international markets.

The US increased its consumption of domestic scrap, driven by a 13% drop in finished aluminium imports, which fell to 0.80 mnt from 0.92 mnt in H1CY’24. Strong domestic scrap prices further discouraged exports, making US offers less viable for Indian buyers.

UK: Aluminium scrap exports remained stable at 0.3 mnt in H1CY’25, mainly to India, China, and Hong Kong. Despite strong market conditions and favourable tariff agreements, export volumes were lower than expected due to a shortage of available material. This scarcity, compounded by rising competition for supplies and environmental export restrictions, led to tighter margins and hindered trade volumes.

Middle East: Scrap exports from the Middle East remained strong at 0.36 mnt in H1CY’25, reflecting a 21% y-o-y increase from 0.3 mnt in H1CY’24. India continued to be the largest importer, accounting for nearly 40% of the region’s total exports. India imported 0.22 mnt in H1CY’25, up 13% y-o-y, largely due to its proximity. These imports helped offset the reduction in scrap exports from the US to India.

Intra-EU27 trade

Intra-EU aluminium scrap trade volumes stood at 1.67 mnt in H1CY’25, down 4% from 1.74 mnt in H1CY’24. Germany remained the largest exporter within the bloc at 0.44 mnt, followed by France (0.24 mnt) and Poland (0.18 mnt). On a global scale, Germany ranked second after the US, but its total exports — including outside EU-27 — fell 8% y-o-y to 0.58 mnt.

EU metal recyclers continue to face headwinds from weak demand, limited scrap availability, and the EU’s 16th sanctions package, which disrupted secondary aluminium flows and created major logistics bottlenecks. Rising freight costs from geopolitical tensions and stricter import regulations further pressured trade. Additionally, Germany’s stagnant economy and subdued activity in construction, automotive, and engineering sectors constrained material flows, keeping market sentiment cautious.

Leave a Reply